S-Corp vs C-Corp Election: What changes when you switch and can you switch back?

Most startup founders make their S-Corp or C-Corp decision once, at formation, and assume it is settled. It is not. The election can be changed in either direction, and there are situations where changing it is not just beneficial but necessary.

The most common trigger is a fundraiser. S-Corps cannot have more than 100 shareholders, cannot have foreign shareholders, and cannot have more than one class of stock. The moment a VC fund wants to invest in preferred shares, or the moment a non-US investor appears on the cap table, S-Corp status is gone. Either you voluntarily revoke the election before the term sheet closes, or the S-Corp status terminates involuntarily the moment an ineligible shareholder receives stock.

The less common but equally real trigger runs in the opposite direction. A C-Corp that has been operating as a profitable small business with no plans to raise institutional capital might look at the 21% corporate tax rate, the double taxation on distributions, and the self-employment tax savings available under S-Corp treatment and decide that S-Corp status makes more financial sense.

Both directions are legally available. Both directions have tax consequences that can follow the company for years. And once you revoke an S-Corp election, there is a five-year waiting period before you can elect it again without IRS consent.

S-Corp vs C-Corp: The core differences before you switch

Understanding what you are giving up or gaining when you switch requires knowing exactly what each election means.

S-Corp treatment passes all income, losses, deductions, and credits through to shareholders' personal tax returns. The corporation itself pays no federal income tax. Shareholders report their pro-rata share of income on their personal return and pay tax at their individual rates. The major benefit for small business owners is that only the portion of income classified as wages is subject to payroll taxes (Social Security and Medicare). Distributions above the reasonable compensation threshold are not subject to self-employment tax.

S-Corp status comes with strict eligibility requirements. The corporation must be a domestic entity. It cannot have more than 100 shareholders. All shareholders must be US citizens or resident aliens. No shareholder can be a corporation, partnership, or most types of trusts. There can only be one class of stock. Violating any of these requirements, even unintentionally, terminates S-Corp status immediately and involuntarily.

C-Corp treatment means the corporation is a separate taxable entity. It pays corporate income tax at the flat 21% rate on its own income. Shareholders pay tax again when they receive dividends. This is the "double taxation" that S-Corps are often said to avoid.

But C-Corp treatment enables what S-Corp treatment cannot: multiple classes of stock (common and preferred), an unlimited number of shareholders, foreign shareholders, and the ability to issue stock that qualifies for the QSBS exclusion under Section 1202. These are the features that institutional investors and venture capital funds require, and they are not available under S-Corp status.

Direction 1: S-Corp to C-Corp (Revoking the S-Corp Election)

This is by far the more common conversion for venture-backed startups. You have an S-Corp election in place, a term sheet arrives, and you need C-Corp status before the round closes.

How to revoke an S-Corp Election

Revoking an S-Corp election does not require a specific IRS form. You submit a written statement of revocation to the IRS service center where you file your annual return. The statement must include the corporation's name, EIN, a clear statement that the S-Corp election is being revoked, the effective date of the revocation, and signatures from shareholders who collectively hold more than 50% of the total issued and outstanding shares, including both voting and non-voting shares.

There is no IRS approval required. No user fee. The revocation takes effect based on when it is filed.

There is one important distinction that changes the consequences entirely. If the S-Corp election was made effective for a given tax year but the due date of the first return for that year has not yet passed, the election can be withdrawn rather than revoked. A withdrawal is treated as if the election was never made. The five-year re-election restriction does not apply to a withdrawal. The corporation can elect S-Corp status again the following year with no waiting period. This withdrawal window closes the moment the first return due date passes, at which point only revocation is available, and the five-year bar applies. For startups that realize shortly after formation that S-Corp status was a mistake, acting before that first return due date preserves significantly more flexibility.

Timing and effective date rules:

If revoking effective the first day of the tax year, the revocation is due by the 15th day of the third month of the tax year. If revoking effective any day other than the first day of the tax year, the revocation must be received by the IRS by the requested effective date. For example, if the S corporation is on a December 31 tax year ending and requests a revocation effective January 1, the revocation is due March 15.

If you want the revocation to take effect on January 1 of the current year for a calendar-year corporation, you must file the revocation by March 15 of that year. Filing after March 15 means the earliest the revocation can take effect is January 1 of the following year, unless you specify a prospective date that has not yet passed.

If a revocation effective date is specified and that date is in the current tax year, the corporation must file two short-period returns for that year: one Form 1120-S for the S-Corp period and one Form 1120 for the C-Corp period.

What changes when you switch from S-Corp to C-Corp

Tax filing: You stop filing Form 1120-S and start filing Form 1120. Income is no longer passed through to shareholders' personal returns.

Corporate tax: The corporation now pays the 21% flat corporate income tax rate on its own income. Shareholders no longer receive K-1s reflecting the company's income on their personal returns.

Retained earnings: Profits that remain in the C-Corp are taxed at the corporate level only, not again until distributed. This can be advantageous for founders who plan to reinvest profits into growth rather than take distributions.

QSBS clock starts over. This is the most significant tax implication and the one most founders do not understand clearly. S-Corp status disqualifies stock from QSBS eligibility under Section 1202. Any time the corporation spent as an S-Corp does not count toward the QSBS five-year holding period. The QSBS clock starts fresh at the date of conversion to C-Corp status. Stock issued after conversion can qualify for QSBS, but the holding period begins at conversion, not when the S-Corp was originally formed.

Under the OBBBA enacted July 4, 2025, QSBS stock issued after that date is eligible for a tiered exclusion: 50% for stock held at least three years, 75% for at least four years, and 100% for at least five years. The per-issuer exclusion cap was raised from $10 million to $15 million. Converting from S-Corp to C-Corp and then issuing stock qualifies for these enhanced benefits, but only for stock issued after conversion. The practical implication is that converting earlier rather than later gives all shareholders more time to accumulate the holding period required for the maximum exclusion.

No built-in gains tax in this direction. When you revoke an S-Corp election and convert to C-Corp, there is no built-in gains tax triggered by the conversion itself. The appreciated assets simply become C-Corp assets. The C-Corp can sell those assets and recognize gain at the standard 21% corporate rate. This is one reason the S-Corp-to-C-Corp direction is generally cleaner from a tax standpoint than the reverse.

The Five-Year Re-Election Restriction

This is the rule that permanently changes how you think about revoking an S-Corp election.

Under IRC Section 1362(g), once S-Corp status is revoked or terminated, the corporation, and any successor corporation, cannot make a new S election for five tax years without IRS consent. The clock starts on the first day of the first tax year in which the termination was effective.

This means if you revoke effective January 1, 2026, the earliest you can re-elect S-Corp status without IRS consent is January 1, 2031. This applies regardless of how the election ended: voluntary revocation, involuntary termination from an ineligible shareholder, and passive income termination all trigger the same five-year bar.

Getting IRS consent for early re-election is possible but not guaranteed. The IRS looks favorably at cases where more than 50% of the stock has changed hands since the termination, the disqualifying event has been corrected, and the re-election is not being used to manipulate tax years. A private letter ruling carrying a user fee starting at $3,000 for smaller businesses is required to seek early re-election consent.

Direction 2: C-Corp to S-Corp (Filing the S-Corp Election)

This direction makes sense for a C-Corp that has been operating profitably with no plans for institutional funding, wants to avoid double taxation, and can satisfy the S-Corp eligibility requirements. It can also be a deliberate strategy when founders want to take distributions from a profitable business without the payroll tax burden that applies to all compensation under C-Corp pass-through arrangements.

How to make the S-Corp Election

A C-Corp that wants to become an S-Corp files Form 2553, Election by a Small Business Corporation, signed by all shareholders. The election must be filed no more than two months and 15 days after the beginning of the tax year the election is to take effect, or at any time during the preceding tax year.

For a calendar-year corporation wanting S-Corp status effective January 1, 2027, Form 2553 must be filed by March 15, 2027, or at any time during 2026. Filing Form 2553 after the deadline means the S election takes effect in the following tax year. Late election relief is available under Rev. Proc. 2013-30 if there is reasonable cause for missing the deadline.

Before filing Form 2553, the corporation must confirm it meets every S-Corp eligibility requirement: it must be a domestic corporation, have no more than 100 shareholders, have only one class of stock, and have only eligible shareholders (individuals, estates, or certain trusts, all of whom must be US citizens or resident aliens). If any of these requirements are not met, the Form 2553 will be rejected.

The built-in gains Tax: The major risk in this direction

This is where the C-Corp-to-S-Corp conversion becomes significantly more complex.

The BIG tax recognition period is five years from the effective date of the S election. Gains recognized after five years are not subject to BIG tax, even if the appreciation occurred during C-Corp years.

Here is how it works. When a C-Corp converts to S-Corp status, the IRS takes a snapshot of the fair market value of all the corporation's assets on the conversion date. Any difference between the fair market value and the adjusted tax basis of each asset at conversion becomes a "built-in gain." If the corporation sells any of those assets within the five-year recognition period, the built-in gain portion of the sale proceeds is taxed at the 21% corporate rate, even though the corporation is now an S-Corp.

This means the S-Corp does not fully escape corporate-level tax until five years after conversion. Any sale of appreciated assets before that anniversary potentially triggers a corporate tax bill that passes through to shareholders on top of the income they already report.

The built-in gains tax is particularly relevant for C-Corps that have developed valuable intellectual property, built significant customer relationships with intangible value, or own real estate that has appreciated during the C-Corp years. The BIG tax applies to all of this appreciation at conversion if those assets are sold within five years.

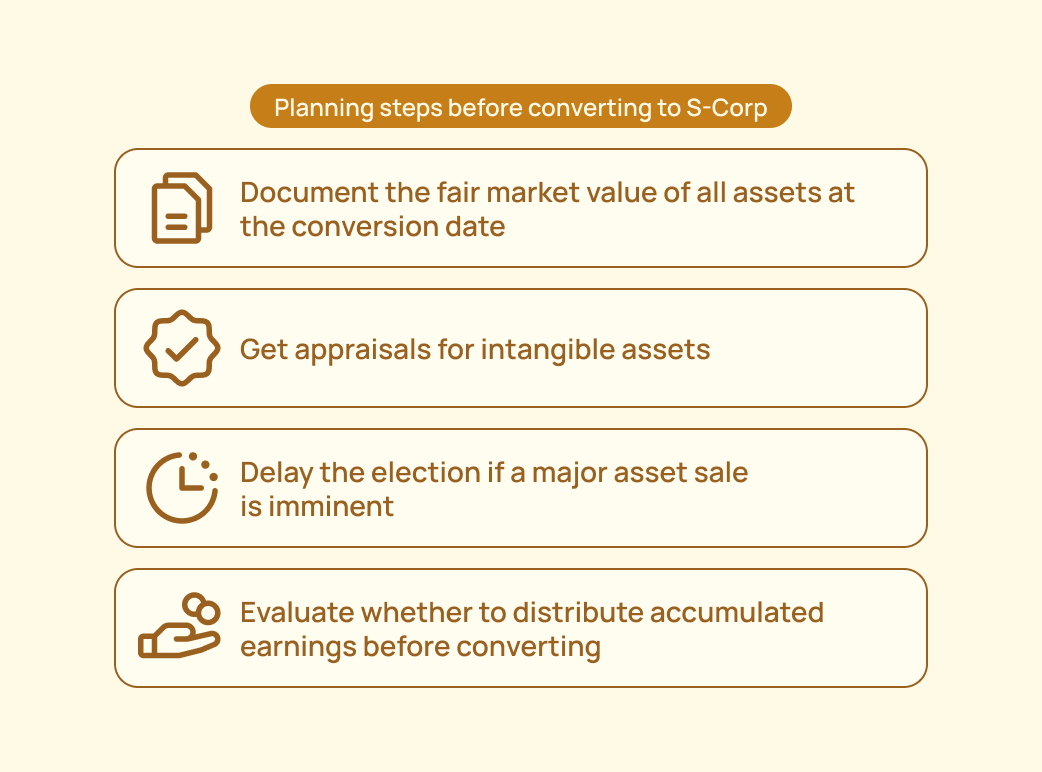

Practical planning steps before converting to S-Corp:

What changes when you switch from C-Corp to S-Corp?

Tax filing: You stop filing Form 1120 and start filing Form 1120-S. Income passes through to shareholders on Schedule K-1.

Corporate tax: The corporation stops paying corporate income tax (subject to the built-in gains tax on assets that appreciated before conversion). Income flows to shareholders and is taxed at their individual rates.

Payroll tax treatment: The S-Corp must pay shareholder-employees a reasonable salary, which is subject to payroll taxes. Distributions above the salary threshold are not subject to self-employment tax. This is the primary ongoing tax benefit of S-Corp status.

Shareholder restrictions activate immediately: After the election, every stock transfer must be reviewed for eligibility. Adding a new investor who is a foreign national or a corporate entity automatically terminates S-Corp status, possibly with retroactive effect.

QSBS eligibility ends. S-Corps cannot issue QSBS. All stock issued after the S election is in effect is disqualified from the Section 1202 exclusion. Any stock that was QSBS-eligible as C-Corp stock remains eligible for shares already issued, but no new QSBS stock can be issued while S-Corp status is in effect.

The QSBS dimension in 2026: Why this matters more than ever

The OBBBA, enacted July 4, 2025, made QSBS significantly more valuable and materially changed the conversion calculus for startup founders.

Under post-OBBBA rules, C-Corp stock issued after July 4, 2025 is eligible for:

A 50% federal capital gains exclusion after a three-year holding period. A 75% exclusion after four years. A 100% exclusion after five years. The per-issuer cap was raised from $10 million to $15 million and is indexed for inflation starting in 2027. The gross asset threshold for the issuing corporation was raised from $50 million to $75 million.

S-Corp stock cannot qualify for any of these exclusions. An S-Corp can never issue QSBS.

Only a C corporation can issue QSBS. If your company is currently an LLC or an S corporation, it must convert to a C Corp before issuing the stock for it to be eligible.

For a startup founder who is holding S-Corp stock and considering a future exit, the math has changed under the OBBBA. Converting from S-Corp to C-Corp now starts the QSBS clock on stock that can qualify for up to $15 million in tax-free gains. Every year spent as an S-Corp is a year the QSBS holding period is not accruing.

Converting early, while the company still has relatively low asset values and limited appreciation, is generally better than converting later when the built-in gains position is larger and the QSBS exclusion would take longer to mature relative to the exit timeline.

Can you switch back? The 5 year rule in practice

Once you have revoked an S-Corp election, you cannot re-elect S-Corp status for five tax years without IRS consent. This restriction under IRC Section 1362(g) applies regardless of the reason for termination.

Here are the practical implications for founders:

If you revoke your S-Corp election to accommodate a VC investment and then later want to return to S-Corp status (perhaps because the company sold a division and the remaining business is smaller), you need to wait five full tax years from the effective date of the revocation.

If the S-Corp election was involuntarily terminated (because an ineligible shareholder received stock accidentally), the same five-year bar applies.

The only way to re-elect within the five-year window is to obtain IRS consent through a private letter ruling. The IRS will consider granting consent when more than 50% of the issued and outstanding shares have changed hands since the termination, and the original circumstances that led to the termination have been corrected.

For most startups that revoke S-Corp status to raise institutional capital, re-election within five years is effectively impossible. Once a VC fund holds preferred shares, the company can never be an S-Corp again regardless of whether the five-year restriction applies, because preferred stock means two classes of stock, which is a permanent S-Corp disqualifier.

Comparison summary: Key differences at a glance

What this means for India-US Founders

If you are an Indian founder who incorporated a Delaware C-Corp, S-Corp status is almost certainly not available to you and not relevant to your situation.

The reason is straightforward. S-Corp eligibility requires that all shareholders be US citizens or resident aliens. A non-resident Indian founder living in India who owns shares in the Delaware C-Corp is a non-resident alien, which is a prohibited shareholder type for S-Corps. The moment any non-resident alien holds stock, S-Corp status is impossible.

For Indian founders who have relocated to the United States and hold green cards or have met the substantial presence test for US tax residency, S-Corp status is technically possible, but it is rarely appropriate because it prevents VC funding, QSBS eligibility for future investors, and multi-class stock structures. Almost every founder on this path is better served by staying with C-Corp status.

The more relevant issue for India-US founders is the QSBS implication of entity status changes. If your Delaware C-Corp has an Indian subsidiary and the parent entity converts or changes its tax classification at any point, the QSBS eligibility and holding period implications for the US entity need to be analyzed carefully, particularly given the OBBBA's enhanced exclusion thresholds.

Frequently Asked Questions

Can a VC-backed startup be an S-Corp?

No. Venture capital funds are structured as partnerships or LLCs, which are ineligible S-Corp shareholders. Additionally, VCs typically require preferred stock with different economic and voting rights from common stock. S-Corps are restricted to a single class of stock. The moment a VC fund invests in preferred shares, both disqualifiers apply simultaneously. A startup that has an S-Corp election in place when a term sheet arrives must revoke the election before the investment closes. If the ineligible shareholder receives stock before the revocation takes effect, S-Corp status terminates involuntarily on the date of that stock transfer, potentially requiring two short-period returns for the year of termination.

What is the built-in gains tax and how do I avoid it?

The built-in gains tax applies when a C-Corp converts to S-Corp status and then sells appreciated assets within five years of the conversion date. The appreciation that existed at the time of conversion is taxed at the 21% corporate rate even though the corporation is now an S-Corp. Assets sold after the five-year recognition period are fully free of the BIG tax regardless of when the appreciation occurred. To minimize exposure, document the fair market value of all assets at the conversion date so you can accurately calculate what portion of any future sale proceeds is subject to BIG tax. Avoid selling appreciated assets within the five-year window if possible. If an asset sale is unavoidable, coordinate the timing with your tax advisor to maximize the use of any built-in losses that can offset built-in gains in the same period.

What happens to QSBS when you switch from S-Corp to C-Corp?

Time spent as an S-Corp does not count toward the QSBS five-year holding period. The QSBS clock starts fresh on the date the S-Corp election is revoked and the corporation returns to C-Corp status. Stock issued after conversion can qualify for QSBS under Section 1202, but the holding period begins at conversion, not at original formation. Under the OBBBA enacted July 4, 2025, stock issued after that date qualifies for a tiered exclusion: 50% after three years, 75% after four years, and 100% after five years, with a per-issuer cap of $15 million. The practical implication for founders is that converting from S-Corp to C-Corp earlier, while the company has lower asset values and more time before a potential exit, maximizes the value of the QSBS benefit.

Can you switch back to S-Corp after revoking the election?

Yes, but not for five years without IRS consent. Under IRC Section 1362(g), once an S-Corp election is voluntarily revoked or involuntarily terminated, the corporation cannot re-elect S-Corp status for five tax years from the effective date of the termination without the IRS granting early consent through a private letter ruling. The IRS considers early consent when more than 50% of outstanding shares have changed hands since the termination and the disqualifying circumstances have been resolved. For most startups that revoke to accommodate VC investment, re-election within five years is practically impossible regardless of the five-year rule, because the preferred stock structure required by institutional investors permanently disqualifies the company from S-Corp status.

In this article

.jpg)

_%20A%20Survival%20Guide%20for%20First-Time%20C-Corp%20Founders.png)