How to record a SAFE Note in your books?

You just signed a SAFE agreement. An investor wired $150,000 to your company bank account. You open your accounting software, create a new transaction, and then pause. Where does this go?

It is not revenue. It is not a loan. The investor is not a shareholder yet. The SAFE note does not have an interest rate, a repayment schedule, or a maturity date. Nothing about it fits the standard categories your chart of accounts was built around.

This confusion is not a sign that you missed something obvious. A Simple Agreement for Future Equity is one of the most common early-stage funding instruments in the startup world, and it is also one of the least understood from a bookkeeping perspective. FASB has not issued a dedicated accounting standard specifically for SAFEs, so practice varies, and even experienced accountants sometimes get it wrong.

This guide explains exactly how to classify a SAFE note on your balance sheet, what journal entries to make at issuance and at conversion, how the accounting changes based on whether your SAFE has a valuation cap or a discount, and why this matters so much when Series A due diligence begins.

What is a SAFE Note and why is it hard to account for?

A Simple Agreement for Future Equity (SAFE) was created by Y Combinator in 2013 as a simpler alternative to convertible notes for early-stage startup funding. The investor gives the company money today and receives the right to convert that investment into equity at a future priced round, typically at a discount or capped valuation.

A standard SAFE has no maturity date. It has no interest rate. There is no obligation to repay the principal in cash. The company is not required to issue shares unless and until a triggering event occurs, typically a qualified financing round, a change of control, or a dissolution.

These characteristics are exactly what make a SAFE hard to categorize under standard accounting rules.

It is not a loan under ASC 470 because there is no maturity date, no interest, and no unconditional obligation to repay cash.

It is not common stock or preferred stock because shares have not been issued. The investor holds no equity in the company at the time of the SAFE.

It does not fit neatly into the "equity" bucket because the SAFE may require the company to issue a variable number of shares depending on the outcome of a future financing round.

FASB has not issued a dedicated accounting standard specifically for SAFEs, so there is still some diversity in practice under US GAAP. Accounting firms often analyze SAFEs under ASC 480 and ASC 815-40, and depending on the legal terms, some SAFEs may need to be classified as liabilities instead of equity.

This is the core tension that makes SAFE accounting more nuanced than it appears from the outside.

The two accounting standards that govern SAFE classification

Before you can record a SAFE correctly, you need to understand the two accounting standards that govern how SAFE notes are analyzed.

ASC 480: Distinguishing liabilities from equity

ASC 480 is the starting point for any instrument that could be classified as either a liability or equity. Under ASC 480, an instrument must be classified as a liability if it embodies an obligation that requires the issuer to transfer assets or settle by issuing a variable number of shares where the monetary value is based on a fixed amount, something other than the fair value of the company's shares, or inversely related to changes in the fair value of the shares.

As the SAFE notes are accounted for under ASC 480, they will be recorded initially at fair value. Fair value is generally assumed to be the transaction price at issuance. For instance, if a $50,000 SAFE note is issued, the fair value on the issuance date is assumed to be $50,000. Under ASC 480, SAFE notes would be subsequently measured at fair value at the end of each reporting period with gains or losses recorded in earnings.

ASC 815-40: Contracts in an Entity's own equity

If a SAFE is not required to be classified as a liability under ASC 480, the analysis moves to ASC 815-40. This standard determines whether a contract involving a company's own equity should be classified as equity or as an asset or liability. For equity classification to apply, the SAFE must be indexed to the company's own stock and must satisfy the equity classification criteria in ASC 815-40-25.

The SAFE is not indexed to the company's own stock per ASC 815-40-15-5 through 15-8a. Thus, equity classification is precluded. There may be an exercise contingency included in the SAFE. The rights of a SAFE holder will generally be higher than that of the common shareholder underlying the contract, meaning there are preferential rights. The number of shares that could be required to be delivered upon net share settlement is essentially indeterminate.

The result of this two-standard analysis is that SAFE classification depends heavily on the specific terms of the agreement.

The 3 possible balance sheet positions for a SAFE

Based on the analysis under ASC 480 and ASC 815-40, a SAFE note lands in one of three places on your balance sheet.

Position 1: Liability (Most common for GAAP-compliant startups)

In practice, it is common for an issuer to classify a SAFE as a liability and subsequently measure it at fair value as a result of applying the guidance outlined above.

When a SAFE is classified as a liability, it is initially recorded at fair value (generally the transaction price) and then remeasured at fair value at each reporting period end. Any change in fair value between reporting periods is recorded as a gain or loss in the income statement. This treatment is more conservative and more technically defensible under GAAP, and it is the approach that most audit firms require for startups approaching Series A or B.

The liability classification does not mean the SAFE is treated like a loan or that investors can demand repayment. It reflects the accounting treatment, not the legal nature of the instrument.

For startups that are pre-Series A and not yet subject to audit, many founders present SAFEs in temporary equity to match investor expectations, with the understanding that the formal GAAP analysis will be conducted and the classification reviewed when an audit firm is engaged ahead of an institutional round.

Position 2: Temporary equity (Mezzanine section)

Some SAFEs, particularly those with standard Y Combinator terms and without unusual conversion features, are classified in the temporary equity or mezzanine section of the balance sheet. This is the section between liabilities and permanent equity in a GAAP balance sheet. Temporary equity treatment applies when an instrument could require settlement in cash or other assets under certain circumstances that are outside the company's control.

Mezzanine classification is common in investor-reporting contexts. Venture capital investors generally expect to see SAFEs presented as equity, and for most VC-backed seed-stage startups the standard early-stage SAFEs are usually shown as equity for investor reporting purposes.

Position 3: Permanent equity

Permanent equity classification is available only when the SAFE meets all of the conditions of ASC 815-40-25, meaning it is indexed to the company's own stock and satisfies all equity classification criteria. This is the least common treatment because standard SAFEs with valuation caps and discounts generally fail the indexation test in ASC 815-40-15. Permanent equity classification is more often seen with very simple SAFEs that have only a fixed discount and no valuation cap, where the settlement amount is determinable at issuance.

The classification decision tree: Which position applies to your SAFE?

The correct classification depends on the specific terms of your SAFE agreement. Here is a practical framework:

Does your SAFE have only a discount, no valuation cap?

If the SAFE has only a discount upon conversion, the settlement amount is approximately known at issuance. ASC 480-10-25-14(a) may apply because the SAFE settles for a fixed monetary amount in equity shares. This is the scenario most likely to result in liability classification under ASC 480.

Does your SAFE have only a valuation cap, no discount?

If the SAFE has only a valuation cap, the settlement amount is not known at issuance because it depends on the future priced round valuation. The analysis moves primarily to ASC 815-40. In most cases, the valuation cap causes the SAFE to fail the fixed-for-fixed criterion, resulting in liability classification.

Does your SAFE have both a discount and a valuation cap?

If the SAFE note includes both a discount and a valuation cap, a predominance assessment should be performed. The predominance assessment would evaluate the likelihood of conversion of the SAFE notes via a discount or via the valuation cap. The outcome of the predominance test determines which standard governs the classification.

At conversion, the investor receives whichever mechanism produces the lower price per share, meaning the more favorable outcome to the investor. If the round prices below the valuation cap, the discount applies. If the round prices above the cap, the cap applies. The predominance assessment in the accounting analysis evaluates which mechanism is statistically more likely to govern the conversion.

Is your SAFE the standard Y Combinator SAFE?

The standard YC SAFE, post-2018 version, has a valuation cap and optional discount. For investor reporting and most practical early-stage startup purposes, it is commonly presented in temporary equity or as an equity-like instrument. For audit-ready GAAP financials, the liability analysis under ASC 480 and ASC 815-40 is typically required.

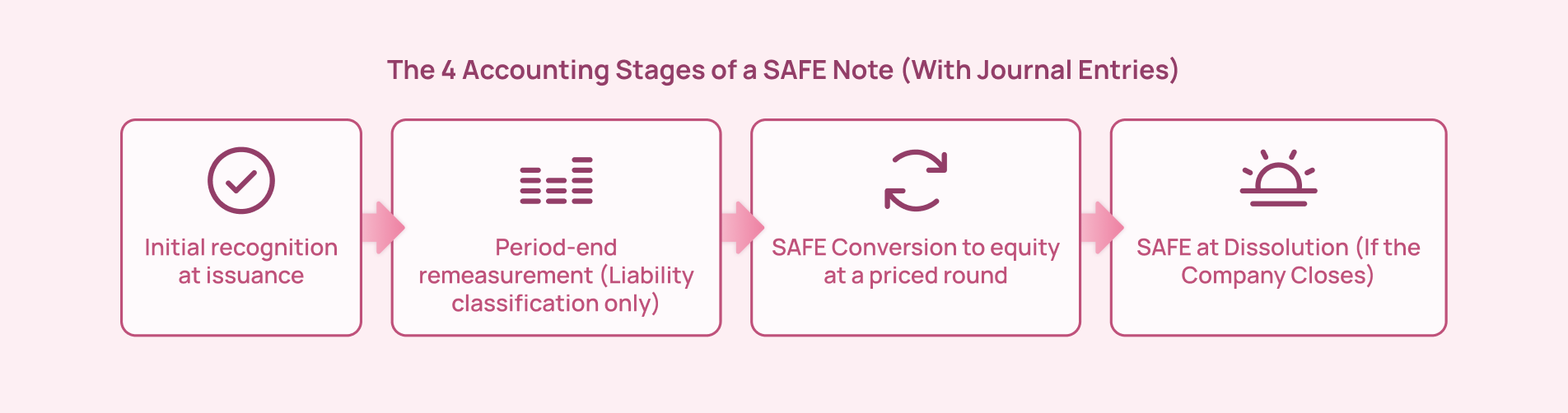

The Journal Entries: From issuance to conversion

This is the section most founders are actually looking for. Here are the specific journal entries for each stage of a SAFE note's life.

Stage 1: Initial recognition at issuance

When you receive the cash from the investor, you record the SAFE at fair value. For a standard SAFE, fair value at issuance is the amount the investor paid.

Example: Investor signs a $150,000 SAFE with a $3 million valuation cap and 20% discount.

If classifying as a liability (most GAAP-compliant approach):

Debit: Cash $150,000 Credit: SAFE Note Liability $150,000

The SAFE Note Liability appears on the balance sheet in the liabilities section, typically as a separate line item labeled "SAFE Note Liability" or "Simple Agreements for Future Equity." It should not be combined with accounts payable, accrued expenses, or other operating liabilities.

If classifying in temporary equity (mezzanine):

Debit: Cash $150,000 Credit: SAFE Notes (Mezzanine/Temporary Equity) $150,000

The SAFE appears in the mezzanine section between total liabilities and stockholders' equity. Many startups present this as "SAFE Notes" as a separate line item between the liabilities and equity sections.

Stage 2: Period-end remeasurement (Liability classification only)

If your SAFE is classified as a liability, you must remeasure it at fair value at each balance sheet date. This requires either a management estimate of fair value or a formal valuation. The change in fair value is recorded in the income statement.

Example: At December 31, the SAFE note's fair value has increased to $165,000 due to increased company valuation.

Debit: Change in Fair Value of SAFE Liability (Income Statement) $15,000 Credit: SAFE Note Liability $15,000

Alternatively, if fair value decreased:

Debit: SAFE Note Liability $X Credit: Gain on Fair Value of SAFE Liability (Income Statement) $X

Period-end remeasurement is one of the most commonly skipped steps for startups doing their own bookkeeping. Skipping it means your liabilities are misstated at every balance sheet date, which creates restatement work during a fundraise.

For temporary equity classification, remeasurement at each period end is not required in the same way. The instrument stays on the balance sheet at the original issuance amount until a triggering event occurs.

Stage 3: SAFE Conversion to equity at a priced round

The most significant accounting event in a SAFE's life is when it converts into preferred stock at a qualifying financing round. This removes the SAFE from the balance sheet and adds the converted amount to the equity section.

Example: The company closes a Series A at $1.00 per share. The SAFE investor, because of the 20% discount, converts at $0.80 per share. The $150,000 SAFE converts into 187,500 shares of Series A Preferred Stock. The par value of the preferred stock is $0.0001 per share.

Step 1: Remove the SAFE from the balance sheet

Debit: SAFE Note Liability $150,000 (or current fair value if remeasured) (If there is a fair value adjustment at conversion date, record that first)

Step 2: Record the shares issued

Credit: Series A Preferred Stock (par value) $18.75 (187,500 shares x $0.0001) Credit: Additional Paid-In Capital (APIC) $149,981.25 (remaining amount after par value)

The total credit to preferred stock and APIC equals the carrying value of the SAFE being extinguished. The detailed journal entries will also allocate amounts between the preferred stock par value and additional paid-in capital based on the number of shares issued, and your accounting team and counsel will work together to make sure the cap table and accounting entries are reconciled.

If the SAFE was classified in temporary equity (not liability), the conversion entry is simpler:

Debit: SAFE Notes (Mezzanine) $150,000 Credit: Series A Preferred Stock (par value) $18.75 Credit: Additional Paid-In Capital $149,981.25

Stage 4: SAFE at dissolution (If the company closes)

If the company dissolves without ever completing a qualifying financing round, the treatment of the SAFE depends on its terms. Most standard SAFEs provide that investors receive either a pro-rata share of the dissolution proceeds or their original investment amount, whichever is greater, ahead of common stockholders. This is treated as a distribution of assets upon liquidation, not as debt repayment.

How SAFE accounting compares to convertible notes

Founders frequently ask how SAFE accounting differs from convertible note accounting. The distinction matters because the two instruments look similar but have meaningfully different accounting treatments.

Convertible Notes are typically classified as debt. They accrue interest and have a maturity date. SAFEs are generally treated as equity-like instruments, though classification depends on the specific terms and legal interpretation. The accounting treatment prior to conversion differs, and so does the process of recognizing the conversion.

Convertible notes appear on the balance sheet as debt under ASC 470. You record interest expense monthly, accrete any original issue discount over the life of the note, and must track the maturity date for balance sheet current vs. non-current classification. The beneficial conversion feature, if any, used to require separate accounting but was eliminated by ASU 2020-06.

SAFE notes have no interest to accrue, no maturity date to track, and no OID to amortize. The ongoing accounting burden is lower for a SAFE than for a convertible note if classified in temporary equity. If classified as a liability requiring fair value remeasurement, the SAFE carries more ongoing accounting complexity than a simple convertible note.

The Series A due diligence problem

This is why correct SAFE accounting matters beyond just good record-keeping.

When a VC conducts financial due diligence before a Series A, one of the first things they look at is how outstanding SAFEs and convertible instruments are presented on the balance sheet. If SAFEs are missing from the balance sheet entirely (a surprisingly common situation when founders do their own bookkeeping and do not know where to put them), or if they are incorrectly recorded as revenue, operating liabilities, or generic equity, the due diligence process will flag this.

The consequences range from a request to restate historical financials, which delays closing and costs accounting fees, to a VC reducing their confidence in the management team's financial controls, which is a harder problem to fix than a journal entry.

The specific issues that come up most often in practice are:

SAFE notes absent from the balance sheet because the founder treated the incoming cash as revenue or as a generic bank deposit with no corresponding liability or equity entry.

SAFE notes recorded as a single line in accounts payable or accrued liabilities without being identified as SAFEs, which makes cap table reconciliation impossible.

Fair value remeasurement not performed for SAFEs classified as liabilities, leading to understated or overstated liability balances at each period end.

Conversion journal entries that do not properly allocate between par value and APIC, leaving an unexplained discrepancy between the equity section of the balance sheet and the cap table.

What does this mean for India-US founders

If you are an Indian founder who raised early capital from Indian angel investors or family offices through a SAFE note, the bookkeeping treatment in your US entity is the same as described above. The currency in which the SAFE was originally funded does not change the accounting classification.

One India-specific point worth noting, SAFE notes received from Indian investors by a US C-Corp may have FEMA and RBI reporting implications on the Indian side, specifically if the Indian investor is a resident Indian individual or entity. The Foreign Exchange Management Act governs outbound investments from India, and investments by Indian residents into foreign startup entities through SAFE-like instruments require regulatory review. This is a compliance matter handled separately from the bookkeeping treatment in your US entity, but it is worth confirming with an advisor who understands both sides of the structure.

From a US bookkeeping standpoint, the entity that receives the SAFE proceeds is the Delaware C-Corp, and the journal entries described above apply to that entity's books regardless of where the investor is located.

Getting your SAFE notes correctly classified, recorded, and reconciled with your cap table before a fundraise is exactly the kind of bookkeeping work that Inkle handles. Book a demo with Inkle to make sure every SAFE on your balance sheet is correctly classified, every conversion is recorded cleanly, and your books are investor-ready before due diligence begins.

Frequently Asked Questions

Is a SAFE note recorded as debt or equity on the balance sheet?

Neither in most cases. A SAFE has no interest rate, no maturity date, and no obligation to repay cash, so it is not traditional debt. Shares have not been issued, so it is not permanent equity. Most SAFEs are analyzed under ASC 480 and ASC 815-40 and land in either liability or temporary equity depending on their specific terms.

What is the journal entry when a SAFE note converts to equity?

Debit the SAFE account for its carrying value and credit preferred stock par value and additional paid-in capital for the total. For example, a $150,000 SAFE converting into 187,500 Series A Preferred shares at $0.0001 par value means crediting $18.75 to preferred stock and $149,981.25 to APIC. Your cap table and balance sheet must reconcile exactly after this entry.

Do I need to remeasure a SAFE note at fair value every quarter?

Only if the SAFE is classified as a liability. Liability classification requires fair value remeasurement at each reporting date with changes recorded in the income statement. Temporary equity classification does not require periodic remeasurement and the instrument stays at its original issuance amount until conversion. Most pre-audit startups use the transaction price as fair value and update it only when a significant event occurs.

How is SAFE note accounting different from convertible note accounting?

Convertible notes are classified as debt and accrue monthly interest, while SAFEs have no interest and no maturity date. For a convertible note you track interest expense and amortize any original issue discount. For a SAFE the main ongoing burden is fair value remeasurement if it is liability-classified, or minimal maintenance if it is in temporary equity. Both instruments produce similar journal entries at conversion into preferred stock.

In this article

.jpg)

_%20A%20Survival%20Guide%20for%20First-Time%20C-Corp%20Founders.png)