SS-4, Form 8832, and Form 2553: Which one actually sets your business tax classification?

When you apply for an EIN, Form SS-4 asks you to describe the type of entity you are. When you want to change how your LLC is taxed, someone mentions Form 8832. When a startup wants S-Corp status, their accountant tells them to file Form 2553. Three forms, all related to how the IRS classifies your business. All three come up in the same conversation. And for most founders, the question is the same: which one actually matters?

The answer is that all three serve a different function in a specific sequence, and only two of them create a legally binding tax classification. Understanding which one does what, and in what order, prevents a category of expensive mistakes that accountants spend considerable time cleaning up.

Before going into detail, here is the one-line function of each form:

- Form SS-4 applies for your Employer Identification Number. It asks you to indicate your entity type, but checking a box on SS-4 does not legally set your federal tax classification. It is an administrative registration, not a tax election.

- Form 8832 is the legally binding entity classification election. It tells the IRS how your eligible entity should be taxed: as a C-Corp, as a partnership, or as a disregarded entity. It cannot elect S-Corp status.

- Form 2553 is the S-Corp election. It tells the IRS your corporation or LLC wants to be taxed under Subchapter S. It handles the underlying entity classification change automatically, without needing Form 8832 first in most cases.

The most important thing to internalize is that SS-4 is not a tax election. The boxes on SS-4 that ask about entity type are for administrative identification purposes. If you want to change how your entity is taxed, you need Form 8832 or Form 2553, not SS-4.

Form SS-4: The EIN Application

Form SS-4, Application for Employer Identification Number, is the IRS form used to obtain an EIN. Every business that needs to file tax returns, hire employees, open a US bank account, or appear on government forms needs an EIN, and Form SS-4 is how you get one.

SS-4 asks about entity type in question 8 and asks about the reason for applying. These fields exist to help the IRS route your EIN to the right account type in its system. They are not a check-the-box classification election. Indicating on SS-4 that your entity is a corporation does not make it taxable as a corporation. Indicating that it is an LLC does not trigger any specific tax treatment. The IRS assigns default classifications based on how the entity was formed under state law, regardless of how the responsible party described it on SS-4.

One practical rule that flows directly from this: you must have an EIN before you can file Form 8832 or Form 2553. The IRS will not accept either election form without a valid EIN already issued. A pending SS-4 application does not satisfy the requirement. The IRS will return Form 8832 if submitted with no EIN or with "Applied For" written in the EIN field.

The sequence is always: SS-4 first, EIN issued, then Form 8832 or Form 2553 if a classification election is needed.

For Indian founders and other non-resident applicants who cannot use the IRS online EIN tool, the SS-4 must be submitted by fax or mail with "Foreign" entered on line 7b in place of an SSN or ITIN. Our full EIN guide covers this process.

What happens if you never file Form 8832 or Form 2553?

Before explaining what each election form does, it helps to understand what the IRS does automatically when no election is filed.

The IRS assigns every new business entity a default federal tax classification under Treasury Regulation Section 301.7701-3. The default depends entirely on how the entity is legally formed under state law.

A single-member LLC is automatically classified as a disregarded entity. This means the LLC is ignored for federal tax purposes and the owner reports all income and expenses directly on their personal return, typically on Schedule C. The LLC pays no separate federal income tax.

A multi-member LLC is automatically classified as a partnership. It files Form 1065, issues Schedule K-1 forms to members, and income passes through to members' personal returns.

A corporation formed under state corporate law (a C-Corp or S-Corp in legal form) is automatically classified as a C-Corp for federal tax purposes. It files Form 1120 and pays corporate income tax at the 21% flat rate.

These defaults apply without any action on your part. The important consequence is that most startups do not need to file either Form 8832 or Form 2553. The default classification fits their situation and no election is required. You only need Form 8832 when you want something different from the default. You only need Form 2553 when you want S-Corp treatment.

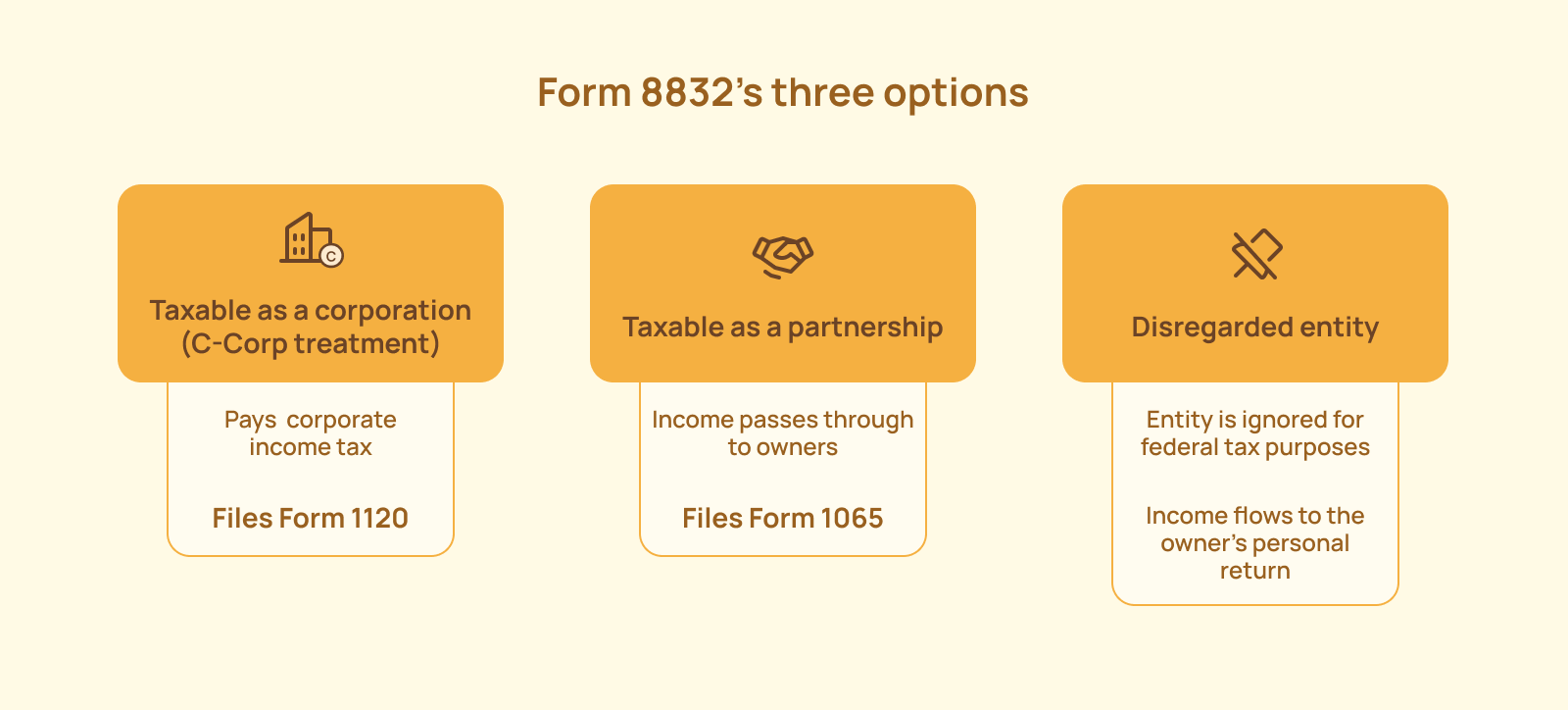

Form 8832: The check-the-box election (C-Corp, Partnership, or Disregarded Entity)

Form 8832, Entity Classification Election, is the IRS form that eligible entities use to override their default classification and elect a different federal tax treatment. It is commonly called the check-the-box election because the form literally presents checkboxes for the available classifications.

S-Corp status is not available on Form 8832. If you check the wrong box on Form 8832 hoping to elect S-Corp treatment, you will receive the C-Corp election you checked, not the S-Corp status you wanted.

Who actually needs to file Form 8832:

A single-member LLC that wants C-Corp treatment instead of the default disregarded entity classification. This is relevant for founders who want to retain earnings at the corporate level, issue QSBS-eligible stock, or position the entity for VC investment.

A multi-member LLC that wants C-Corp treatment instead of the default partnership classification.

A foreign entity that needs to establish its US tax classification because foreign entity defaults are different from domestic ones and often need to be specified explicitly.

A business that previously made a classification election and wants to change it after the 60-month restriction period has passed.

The 60-month restriction rule:

Once an eligible entity has filed Form 8832 to change its classification, it cannot make another classification change by election for 60 months from the effective date of the election. This is not a filing deadline. It is a restriction on how frequently you can change. There are exceptions: if more than 50% of ownership interests changed hands since the prior election, a new election can be made earlier.

The effective date window:

A Form 8832 election can be effective up to 75 days before the filing date or up to 12 months after the filing date. This gives you meaningful flexibility in timing but the window is firm. If you want an election that is retroactive by more than 75 days, you need late election relief under Rev. Proc. 2009-41, which requires filing within 3 years and 75 days of the requested effective date and having filed tax returns consistent with the requested classification.

What Form 8832 does not do:

It does not elect S-Corp status. It does not affect state tax classification automatically in every state. It does not change your legal entity type under state law. It does not replace the need to file the appropriate tax return for the classification you elected.

Form 2553: The S-Corp Election

Form 2553, Election by a Small Business Corporation, is the IRS form used to elect S-Corp tax treatment. It is filed by eligible corporations and LLCs that want income to pass through to shareholders' personal returns rather than being taxed at the corporate level.

S-Corp status requires meeting all eligibility criteria at the time of the election: the entity must be a domestic corporation or a domestic LLC, it cannot have more than 100 shareholders, all shareholders must be US citizens or resident aliens, there can be only one class of stock, and no shareholder can be a corporation, partnership, or most types of trusts.

The critical distinction from Form 8832:

An LLC that files Form 2553 does not need to file Form 8832 first. An LLC that files Form 2553 without previously filing Form 8832 is treated as simultaneously electing corporate classification and S-Corp status. The IRS accepts this dual election on a single Form 2553. Form 2553 Part IV handles the underlying classification change automatically.

This is one of the most practically useful things to understand about these three forms. The default assumption is that you need to file Form 8832 to elect C-Corp treatment first, and then file Form 2553 to elect S-Corp treatment second. That sequence is only necessary in specific circumstances. In most cases, filing Form 2553 alone is sufficient.

The exception where Form 8832 is filed before Form 2553: if an LLC previously filed Form 8832 to elect C-Corp treatment, and that election has been in effect for some time, the LLC then files Form 2553 to convert from C-Corp to S-Corp treatment. In this scenario, both forms are in the picture, but at different points in time.

Filing deadline:

Form 2553 must be filed no later than two months and 15 days after the beginning of the tax year the election is to take effect, or at any time during the preceding tax year. For a calendar-year entity wanting S-Corp status effective January 1, 2027, Form 2553 must be filed by March 15, 2027, or any time during 2026.

Missing this deadline means the S-Corp election takes effect the following year. Late election relief is available under Rev. Proc. 2013-30 if there is reasonable cause.

What Form 2553 does not do:

It cannot elect C-Corp treatment. It cannot elect disregarded entity or partnership treatment. It does not apply to entities that are already ineligible for S-Corp status, such as those with foreign shareholders or more than one class of stock.

How the 3 forms work together?

Now that each form is defined clearly, here is how they interact in every common startup scenario.

Scenario 1: Single-member LLC, wants default treatment (no elections needed)

File SS-4, get EIN. The LLC defaults to disregarded entity. File Schedule C on your personal Form 1040 each year. Form 8832 and Form 2553 are not needed and should not be filed.

Scenario 2: Single-member LLC, wants C-Corp treatment for QSBS or VC investment

File SS-4, get EIN. File Form 8832 to elect C-Corp (association) treatment. The LLC is now taxed as a C-Corp and files Form 1120. Form 2553 is not needed unless you later want to convert to S-Corp.

Scenario 3: Single-member LLC, wants S-Corp treatment to reduce self-employment tax

File SS-4, get EIN. File Form 2553 directly. You do not need Form 8832 first. Form 2553 handles the underlying corporate classification and the S-Corp election in a single filing.

Scenario 4: Delaware C-Corp (legally incorporated as a corporation)

File SS-4, get EIN. The C-Corp defaults to C-Corp tax treatment automatically. No Form 8832 needed. If you want S-Corp treatment, file Form 2553 by the deadline.

Scenario 5: LLC previously filed Form 8832 for C-Corp, now wants S-Corp

The LLC has been taxed as a C-Corp under the Form 8832 election. File Form 2553 by the deadline to convert to S-Corp treatment. This is the one scenario where both Form 8832 and Form 2553 appear sequentially.

Scenario 6: Multi-member LLC, wants C-Corp treatment

File SS-4, get EIN. File Form 8832 to elect C-Corp treatment. The LLC is now taxed as a C-Corp. File Form 1120 each year.

Scenario 7: Multi-member LLC, wants S-Corp treatment

File SS-4, get EIN. Confirm all S-Corp eligibility requirements are met. File Form 2553 directly. Form 8832 is not required first.

The most common mistakes

Mistake 1: Believing SS-4 sets your tax classification.

The entity type field on SS-4 is descriptive, not prescriptive. Indicating that your LLC is an LLC on SS-4 does not trigger any tax election. The IRS applies default classification rules regardless of what SS-4 says about entity type.

Mistake 2: Filing Form 8832 to elect S-Corp status.

Form 8832 does not have an S-Corp option. If you file Form 8832 selecting corporation treatment, you get C-Corp tax treatment. S-Corp status requires Form 2553.

Mistake 3: Filing Form 8832 before Form 2553 when it is not required.

Many founders and even some advisors believe you must always file Form 8832 to establish corporate status before filing Form 2553 for S-Corp treatment. This is not true. An LLC that files a timely Form 2553 is treated as having simultaneously elected corporate classification. Form 8832 is not a prerequisite.

Mistake 4: Filing Form 8832 without an EIN.

The IRS will not accept Form 8832 if the EIN field is blank or if it contains "Applied For." The EIN must be fully issued before Form 8832 is submitted. The same applies to Form 2553.

Mistake 5: Missing the Form 2553 deadline and assuming it applied retroactively.

Form 2553 has a specific filing deadline. Missing it does not invalidate the election permanently, but it means the election applies to the following tax year, not the current one. If you wanted S-Corp status effective January 1, 2026, and you missed the March 15, 2026 deadline, the earliest your election takes effect without late election relief is January 1, 2027.

Mistake 6: Not understanding the 60-month restriction on Form 8832.

After filing Form 8832, the entity cannot change its classification again for 60 months without meeting the ownership-change exception. This means a founder who files Form 8832 to elect C-Corp treatment and then decides they want to revert to disregarded entity or partnership treatment cannot do so for five years without IRS consent.

What does this mean for India-US founders?

For Indian founders who have incorporated a Delaware C-Corp with Indian ownership, the interaction between these three forms has specific implications.

First, a Delaware C-Corp is a corporation by state law and defaults to C-Corp tax classification automatically. You do not need Form 8832 to establish C-Corp status. The only reason a Delaware C-Corp would file Form 8832 is to change its tax classification, and for VC-backed startups this is essentially never appropriate.

Second, S-Corp status is not available to Indian founders who are non-resident aliens. S-Corp eligibility requires all shareholders to be US citizens or resident aliens. A non-resident Indian founder who owns shares in the Delaware C-Corp is ineligible. Filing Form 2553 in this situation would result in rejection.

Third, if an Indian founder formed a US LLC (rather than a C-Corp) and later files Form 8832 to elect C-Corp treatment for tax purposes, this creates a single-member LLC treated as a C-Corp for federal tax purposes. This entity is a foreign-owned US disregarded entity before the election and a foreign-owned domestic corporation after it. The Form 8832 election for a foreign-owned entity triggers Form 5472 filing obligations. A foreign-owned single-member LLC that elects disregarded entity status triggers a Form 5472 filing requirement. Form 5472 is an information return that reports transactions between the foreign owner and the US entity, and the penalty for failing to file it is $25,000 per form per year.

Quick Reference: Which form does what?

If you are unsure which of these forms applies to your startup or whether your current tax classification matches what you intended, book a demo with Inkle to have a cross-border tax professional review your entity structure and confirm that the right elections are in place.

Frequently Asked Questions

Does checking the entity type box on Form SS-4 set my LLC's tax classification?

No. The entity type field on Form SS-4 is for administrative identification purposes and does not create a legally binding tax election. The IRS assigns default tax classifications based on how the entity is formed under state law, regardless of what SS-4 says. A single-member LLC is a disregarded entity by default. A multi-member LLC is a partnership by default. A corporation is a C-Corp by default. If you want a classification different from the default, you must file Form 8832 (for C-Corp, partnership, or disregarded entity treatment) or Form 2553 (for S-Corp treatment). SS-4 is the prerequisite for both since you need an EIN before filing either election form, but SS-4 itself is not the election.

Do I need to file Form 8832 before Form 2553 to elect S-Corp status for my LLC?

In most cases, no. An LLC that files a timely Form 2553 is automatically treated as having elected corporate classification simultaneously. The IRS accepts Form 2553 as a dual election that handles both the underlying corporate classification and the S-Corp election in one filing. You only need to file Form 8832 before Form 2553 if your LLC previously made a Form 8832 election for C-Corp treatment and you are now converting to S-Corp, or in certain specific circumstances involving foreign entities. For a standard domestic LLC making a first-time S-Corp election, Form 2553 alone is sufficient.

What happens if I file Form 8832 to try to elect S-Corp status?

You will receive C-Corp tax treatment, not S-Corp status. Form 8832 offers three classification options: C-Corp, partnership, and disregarded entity. S-Corp is not one of them. If you check the corporation box on Form 8832, the IRS will classify you as a C-Corp. To elect S-Corp status, you must file Form 2553. This is one of the most common and costly mistakes in entity classification because the C-Corp election under Form 8832 triggers the 60-month restriction, meaning you cannot change the classification again for five years without IRS consent.

What is the correct order of filing SS-4, Form 8832, and Form 2553?

The sequence always starts with SS-4 to obtain an EIN. An EIN must be fully issued before either Form 8832 or Form 2553 can be filed. After the EIN is in hand, the order depends on what you want. If you want C-Corp treatment for your LLC, file Form 8832. If you want S-Corp treatment for your LLC, file Form 2553 directly without filing Form 8832 first. If you have a Delaware C-Corp and want S-Corp treatment, file Form 2553 directly since the corporation already defaults to C-Corp status. The only scenario where Form 8832 and Form 2553 are both required is when an LLC previously made a Form 8832 election for C-Corp treatment and now wants to convert to S-Corp.

In this article

.jpg)