What happens if a contractor refuses to submit a W-9?

You're ready to pay your first contractor. You send over the W-9 form with a polite email explaining it's a compliance requirement. Days go by. The contractor responds with something like "I don't think I need that" or "Can't you just pay me without it?" or simply doesn't respond at all.

Now you're stuck. You have work delivered, you want to pay the person, but you don't have the tax documentation the IRS requires. What do you actually do? Can you just pay them anyway and figure it out at tax time? What are the consequences if you don't get that form? Does the contractor have any legitimate reason to refuse?

Most founders don't know the answers to these questions, which is why this situation creates more anxiety than it should. The good news is that there are clear rules about what happens next and what your options actually are. The bad news is that some of those options are more painful than others.

Why do contractors sometimes refuse W-9?

Before diving into consequences, it's worth understanding why contractors push back on W-9 requests in the first place. Sometimes it's legitimate confusion. Many contractors have never filed a tax return or dealt with US tax obligations before. They might think a W-9 is a SSN application or that it exposes them to audit risk. Neither is true, but the fear is real.

Other contractors refuse because they're trying to hide unreported income or they're working multiple jobs and want to avoid paper trails. Some are undocumented workers who can't provide a real SSN. Some just don't understand what the form is and assume it's bad for them. A small percentage are genuinely trying to avoid proper tax reporting.

The legitimate reasons are usually just confusion. The illegitimate reasons are your real problem. If a contractor is legitimately refusing to provide a W-9 because they can't provide a real tax ID, then you have a deeper compliance issue and shouldn't be working with them. If they're refusing because of confusion, that's fixable with a quick conversation.

The legal requirement: What the IRS actually mandates

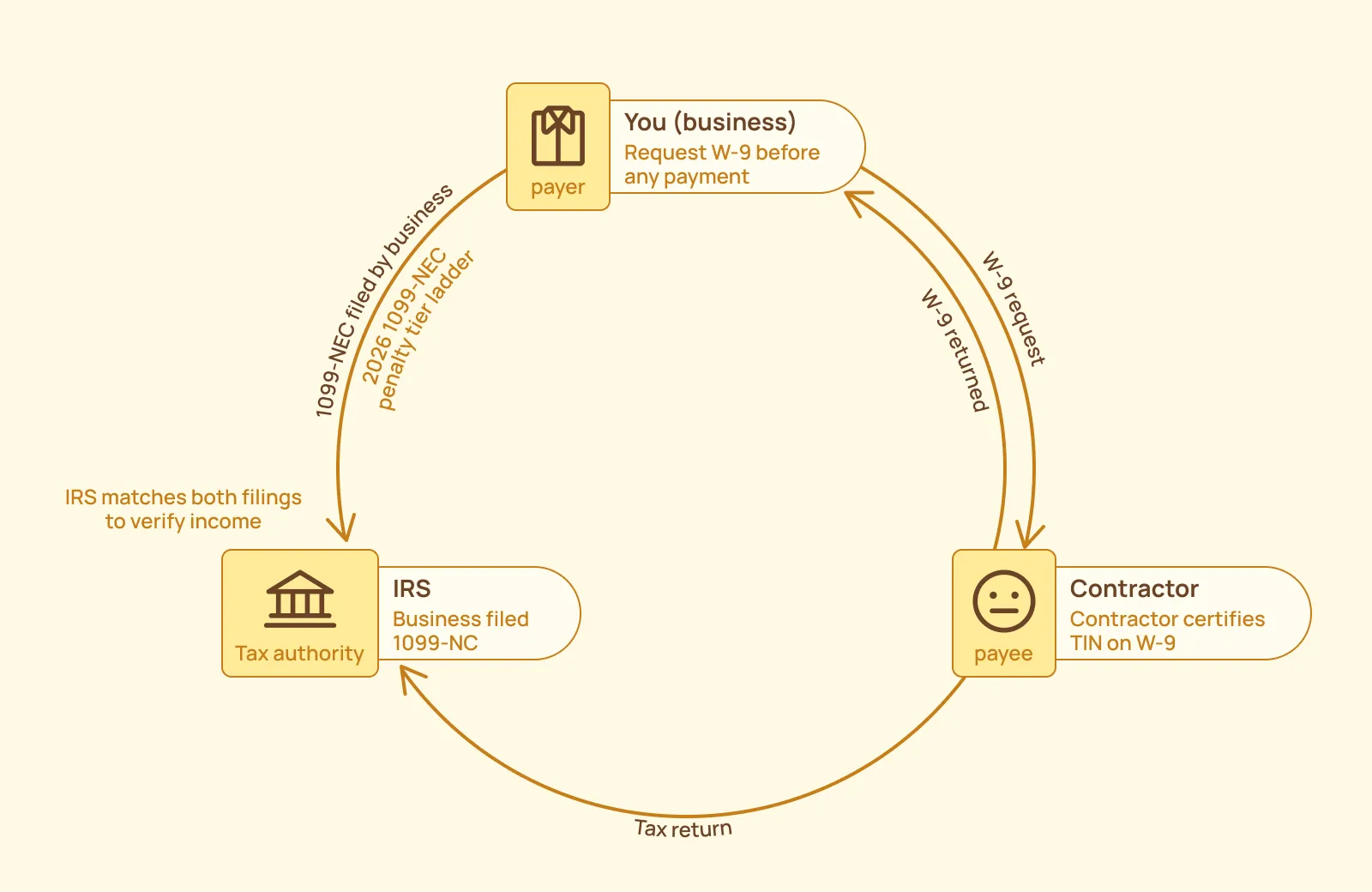

The IRS requirement is clear. If you pay a contractor $600 or more in a calendar year (now $2,000 in 2026 after the threshold increase), you must file Form 1099-NEC reporting that payment. One important exception: if backup withholding applies to any payment, you must file a 1099-NEC for that contractor regardless of the total amount paid during the year, even if it's well below $2,000.

To file 1099-NEC correctly, you need the contractor's legal name, address, and tax identification number (either SSN or EIN). The contractor provides this information on the W-9 form.

The W-9 is not optional. It's not a suggestion. It's a legal requirement that both you and the contractor are expected to comply with. The contractor is required to provide accurate information. You are required to request it and verify it.

What's less clear to most founders is that the lack of a W-9 doesn't prevent you from filing a 1099-NEC. You can file based on whatever information you have. But filing with incomplete or inaccurate information triggers IRS notices, rejected filings, and potential audits. The W-9 protects both of you by creating a documented record that you requested the information and the contractor certified its accuracy.

Scenario one: Pay them without a W-9 and deal with it later

This is what most founders do. They need the work completed. They like the contractor. They don't want conflict. So they pay the contractor and assume they'll figure out the W-9 situation later or at tax time.

Here's what actually happens. When you file your tax return in April 2026, your accountant asks for a list of contractors you paid. You tell them about this contractor but don't have a W-9. Your accountant either files a 1099-NEC with whatever information you have, or they skip it entirely and assume the payment was under the threshold.

If they file with incomplete information, the IRS matches it against the contractor's tax return. If the contractor filed their return without reporting this income (because they're trying to hide it), you now have a mismatch. The IRS might reach out to you asking for documentation that you requested a W-9. If you have an email trail showing you asked for the form, that helps establish that you made a good-faith effort. But documentation alone doesn't protect you from your actual exposure here.

If you made a reportable payment without obtaining a TIN and failed to apply backup withholding, you become directly liable to the IRS for the uncollected withholding tax — 24% of the gross payment. That's your liability, not a share of the contractor's tax bill. The IRS treats the failure to withhold as your compliance failure, separate from whatever the contractor did or didn't report.

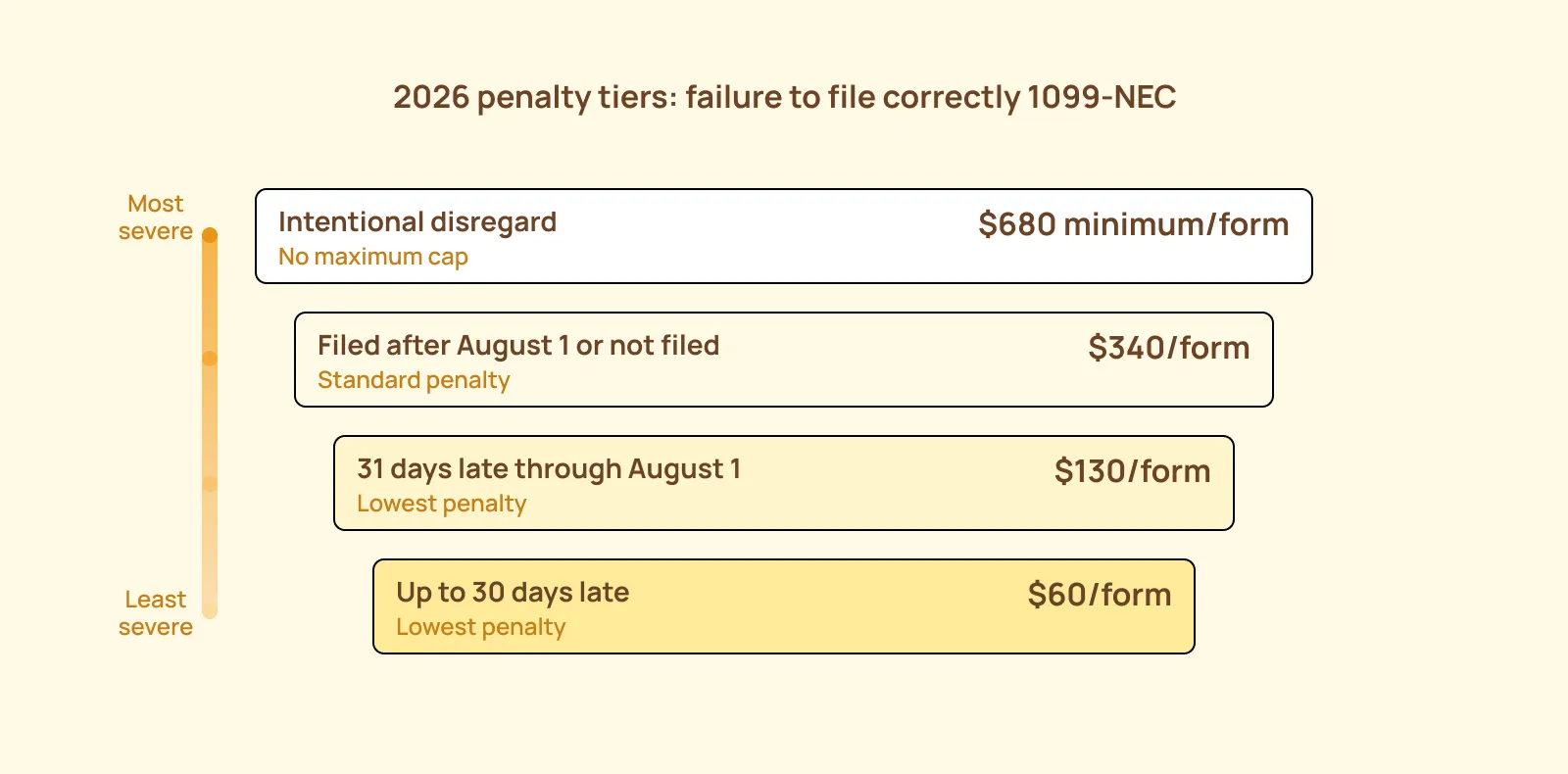

If your accountant skips the 1099 altogether, you're underreporting. If the IRS later discovers you paid this contractor $8,000 and didn't file a 1099, you face a penalty. The penalties for not filing a correct 1099-NEC follow a tiered structure based on how late you are. For 2026, the penalty is $60 per form if you file within 30 days of the deadline, $130 per form if you file between 31 days late and August 1, and $340 per form if you file after August 1 or don't file at all. If the IRS determines the failure was intentional disregard, the minimum penalty jumps to $680 per form with no cap.

The biggest risk isn't the penalty though. It's the audit. If the IRS is auditing your business for any reason and they discover unreported contractor payments, that creates a line of questioning about your bookkeeping and compliance practices. One missing W-9 can cascade into a much larger audit than you bargained for.

Scenario two: Don't pay them until they submit a W-9

This is the legally sound approach but the one most founders hate because it feels awkward. You tell the contractor that you cannot legally process payment without a valid W-9 on file. You ask them to complete the form and return it before you can initiate the wire transfer.

Contractors often push back hard on this. They might claim they're in a hurry. They might say they don't have time to fill out forms. They might threaten to find another client. But if they're truly unwilling to provide a W-9, that tells you something important about whether you should be working with them at all.

The legal and financial protection here is absolute. If you don't pay without a W-9, you have zero exposure to 1099-NEC filing issues because you genuinely don't have a contractor payment to report. You collected the form before payment, which is exactly what the IRS expects.

The practical downside is that you might lose the contractor. Some people genuinely won't work with US companies because they don't want to deal with tax documentation. Others will decide the friction isn't worth it. If the contractor is easily replaceable, this isn't a big loss. If they're a specialist you desperately need, this creates a real problem.

Scenario Three: Use backup withholding

If a contractor refuses to provide a W-9 and you choose to pay them anyway, backup withholding isn't one option among several, it's a legal requirement. When a contractor fails to provide a valid Taxpayer Identification Number for a reportable payment, IRS rules mandate that you withhold 24% of the gross payment and remit it to the IRS rather than paying it to the contractor.

Here's how it works in practice. If the contractor bills you $5,000, you withhold $1,200 and send $3,800 to the contractor. You then report the full $5,000 payment on a 1099-NEC with $1,200 shown as federal income tax withheld in Box 4. You also report and remit all backup withholding collected during the year to the IRS using Form 945, Annual Return of Withheld Federal Income Tax, which is filed separately from your business tax return.

The contractor receives the 1099-NEC and can claim a credit for the withheld amount when they file their taxes, but they only take home $3,800 unless they recover it through their return.

Backup withholding protects you by demonstrating to the IRS that you took required action when you couldn't collect a valid TIN. It also creates a strong incentive for contractors to provide a W-9 quickly, because they see the immediate financial consequence of not doing so.

The challenge is that most contractors hate it. They're expecting $5,000 and suddenly they're getting $3,800. They often blame you for the shortfall even though it's their refusal to provide a W-9 that created the situation. This frequently damages the working relationship. But it's not optional, if you're paying a contractor who won't give you a TIN, this is what compliance looks like.

One important note: if you fail to apply backup withholding when required, the IRS can hold you directly liable for the full amount that should have been withheld. That liability is yours regardless of what the contractor ultimately reports on their own return.

Scenario Four: Classify them as an employee

If a contractor consistently refuses to provide a W-9 and the work is ongoing, it's worth stepping back and asking a different question: was this person actually an independent contractor to begin with?

Worker classification is a legal determination based on the nature of the working relationship, not on whether someone is willing to fill out paperwork. The IRS uses a right-to-control test that looks at three categories: behavioral control (do you direct how and when the work gets done?), financial control (do you control the business aspects of the work, like providing tools or setting rates?), and type of relationship (is there a written contract, does the work continue indefinitely, is it central to your business?). Many states also apply a stricter ABC test, which presumes someone is an employee unless the hiring entity can prove all three conditions for independent contractor status.

A W-9 refusal doesn't reclassify anyone. It triggers backup withholding obligations. But if you examine the working relationship and realize the person has been functioning as an employee all along — taking direction from you, working set hours, using your equipment — then reclassification may be appropriate and overdue, regardless of the W-9 situation.

If you do correctly reclassify someone as an employee, they complete a W-4 instead of a W-9, and you handle withholding through payroll in the normal way. The W-9 compliance issue disappears because it no longer applies.

Misclassifying an employee as a contractor carries serious consequences — liability for unpaid payroll taxes on both sides, unemployment taxes, potential wage and hour claims, and Trust Fund Recovery Penalties that can attach personally to individuals responsible for payroll decisions. Don't use reclassification as a workaround for a missing W-9. Only do it if the facts of the relationship actually support it.

What actually happens to you

If you pay a contractor without a W-9 and get caught, the consequences vary based on the situation.

If the contractor properly reports the income on their own tax return, the IRS matches it to your payment and there's no problem. You might file the 1099-NEC late or with incomplete information, but if the numbers match what the contractor reported, the IRS generally doesn't pursue it.

If the contractor doesn't report the income and the IRS discovers the discrepancy during an audit of either party, you face questions about why you didn't collect a W-9. If you can show an email trail proving you requested one, you're mostly protected. The burden shifts to the contractor for not reporting the income.

If the contractor is intentionally hiding income and the IRS determines you should have been more diligent about collecting a W-9, you could face penalties for failing to file accurate 1099-NECs. These penalties start at $60 per form for filings up to 30 days late, increase to $130 per form between 31 days and August 1, and reach $340 per form for filings after August 1 or not filed at all. If the IRS classifies the failure as intentional disregard, the minimum penalty is $680 per form with no upper limit.

The worst-case scenario is that you're audited for unrelated reasons, the auditor discovers contractor payments without W-9s on file, and this becomes a line item in the audit. It doesn't necessarily result in huge penalties, but it extends the audit scope and increases the chance of finding other issues.

The financial risk is usually manageable. The time risk is worse. An audit triggered partially by missing 1099 documentation takes months to resolve and diverts significant attention from your business.

What should you actually do?

The best practice is straightforward. Before any payment, send the W-9 form and explain that you cannot legally process payment without it. Use language that frames this as a legal requirement, not a personal preference.

If the contractor asks questions, answer them honestly. A W-9 is just a tax ID form. It doesn't trigger audits. It doesn't create tax liability beyond what they already have. It just tells the IRS who received the payment so they can match it to the contractor's tax return. Most confusion disappears once you explain what the form actually does.

If the contractor refuses, you have a decision to make. You can require it as a hard line, implement backup withholding, convert them to an employee if the work is ongoing, or walk away from the engagement. The choice depends on how essential the contractor is and how much friction you're willing to absorb.

The clear answer from a compliance perspective is to not pay without a W-9. The pragmatic answer depends on your specific situation, but you should never pay without understanding what the consequences might be.

Frequently Asked Questions

Can I pay a contractor under $600 and skip the W-9 entirely?

In 2026, the threshold is $2,000, so payments under that amount don't legally require 1099-NEC filing in most situations. However, there's a critical exception: if backup withholding applies to any payment, because the contractor didn't provide a valid TIN — you must file a 1099-NEC regardless of the total amount paid. Even if you paid someone $400 and withheld $96, you still have to file. Beyond that exception, skipping the W-9 for small payments is still bad practice. If you end up paying the same contractor multiple times and the total crosses $2,000, you need the form from day one.

What if the contractor says they don't have a SSN because they're a foreigner?

If they're a foreign contractor, they don't use a W-9. The form they need depends on whether they're an individual or an entity. A foreign individual uses Form W-8BEN, Certificate of Foreign Status of Beneficial Owner for Individuals. A foreign company, partnership, or other entity uses Form W-8BEN-E. Getting this distinction wrong creates its own compliance problems, so confirm what type of contractor you're dealing with before sending the form. On your end, you report the payment on Form 1042-S rather than a 1099-NEC. You'll need tax identification before you can pay them compliantly, and the rules around withholding and treaty benefits are more complex than the domestic W-9 process.

Can the contractor claim the W-9 is private information they don't want to share?

A W-9 is a tax form, not a banking form. It doesn't expose financial accounts or sensitive information. The contractor is providing their name, address, and tax ID number, which are facts already on file with the IRS. Claiming privacy concerns is usually a sign they don't understand what the form is. A quick explanation usually resolves it.

What if the contractor provides a fake SSN on the W-9?

This is fraud on the contractor's part. You're not liable for knowingly filing a fraudulent 1099, but you're also not protected by collecting a false W-9. If you suspect the SSN is fake, you can ask the contractor to verify it or decline to work with them. A real contractor should be able to provide a valid tax ID without hesitation.

If I use backup withholding, can I continue working with the contractor?

Technically yes, but the relationship is usually damaged. The contractor knows they're getting paid less because of the backup withholding, and they blame you. Most contractors either provide the W-9 immediately once they realize what backup withholding means, or they stop working with you. Either way, the situation is resolved, just not pleasantly.

What if the contractor doesn't live in the US and I'm paying them in a foreign country?

If they're a foreign person, the rules are completely different. For a foreign individual, you collect Form W-8BEN. For a foreign entity like a company or partnership, you collect Form W-8BEN-E. You report the payment on Form 1042-S, not a 1099-NEC. The default withholding rate for U.S.-source income paid to foreign persons is 30%, though this can be reduced or eliminated if the contractor's country has a tax treaty with the U.S. and they claim it on their W-8 form.

Note that Form 1042-S reporting may still be required even when withholding is reduced to zero under a treaty. Do not use 1099-NEC for payments to foreign contractors, that's a separate compliance framework entirely.

Does requesting a W-9 make the contractor think I'm auditing them?

No. A W-9 is a standard business form. Every legitimate contractor understands that it's required. If a contractor thinks a W-9 request is unusual, they probably have something to hide or they're genuinely confused about US tax requirements. Either way, a simple explanation clarifies it.

In this article

.jpg)