How Should C-Corps Use Form 100-ES for California Estimated Tax Payments?

Delaware C-Corps that are registered, qualified, or doing business in California may need to pay California corporate taxes before the annual Form 100 deadline. These payments are called California estimated tax payments, and they help the company pay tax during the year instead of waiting until the return is filed.

This can surprise startup founders because California does not follow the simple federal-style 25% per quarter payment pattern. For corporations, California generally uses a 30-40-0-30 installment schedule. That means a large share of estimated tax can be due in the first half of the year, even when founders are still focused on product, hiring, fundraising, or customer growth.

For example, a Delaware C-Corp operating in California may owe the $800 minimum franchise tax even if it is pre-revenue or operating at a loss. If the company has California taxable income, it may also need to make estimated tax payments during the year using Form 100-ES. Missing or underpaying these amounts can lead to penalties, interest, FTB notices, and cleanup work before fundraising or diligence.

What Are California Estimated Tax Payments for C-Corps?

California estimated tax payments are advance payments toward a corporation’s California franchise or income tax liability. A C-corp generally should not wait until the annual Form 100 filing deadline to pay everything if estimated tax payments are required during the year.

For Delaware C-Corps with California obligations, these payments can matter even when the company is still early-stage. The estimated tax process can cover the minimum franchise tax, tax on California-apportioned income, and any expected balance that would otherwise become due when Form 100 is filed.

California estimated tax payments can cover:

- The $800 minimum franchise tax.

- California corporate income tax.

- Tax on California-apportioned income.

- Balances that would otherwise be due with Form 100.

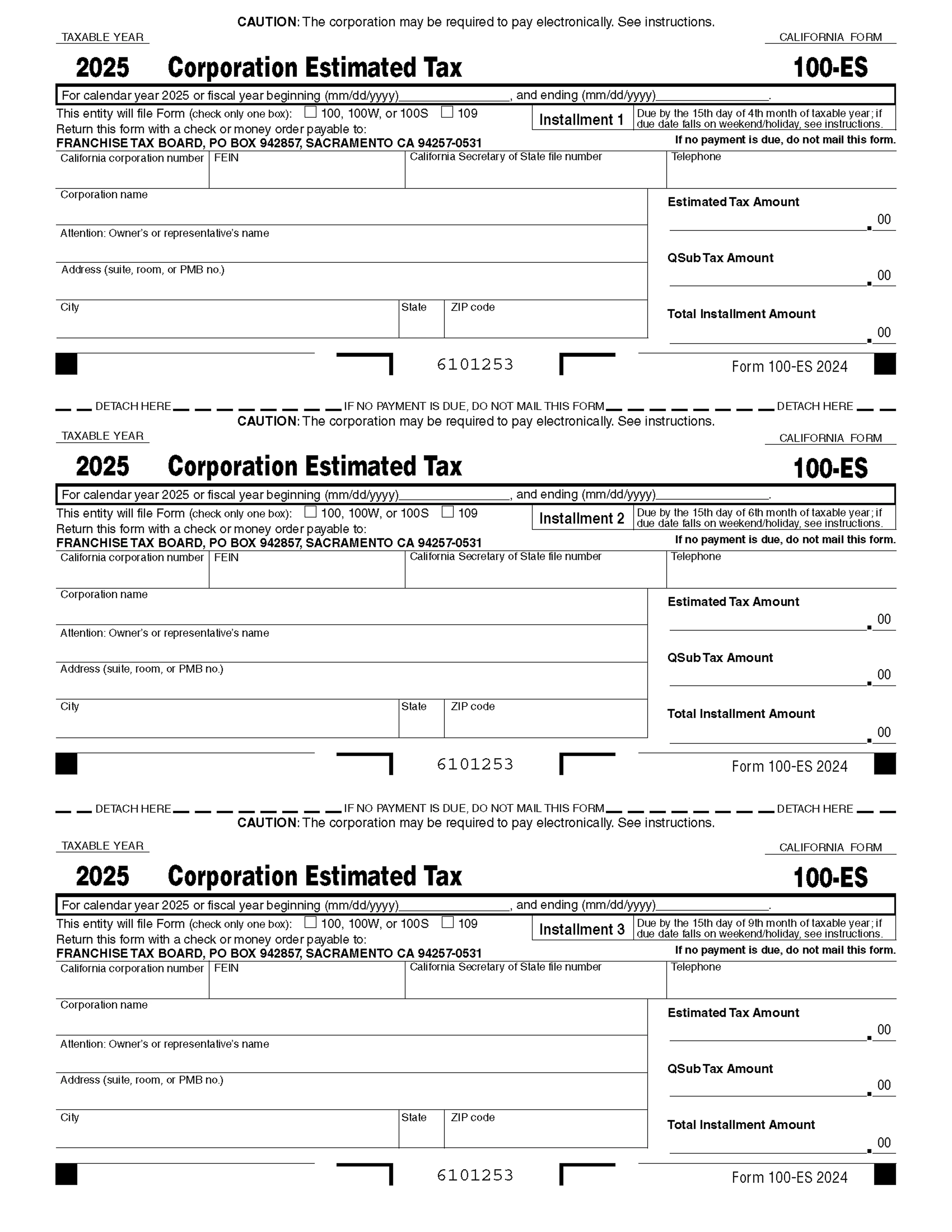

What Is Form 100-ES?

Form 100-ES is the California corporation estimated tax form. The California Franchise Tax Board says corporations use Form 100-ES to figure and pay estimated tax for the taxable year. For startups, this form is mainly relevant when a C-corp has California filing obligations and needs to pay tax before filing its annual Form 100.

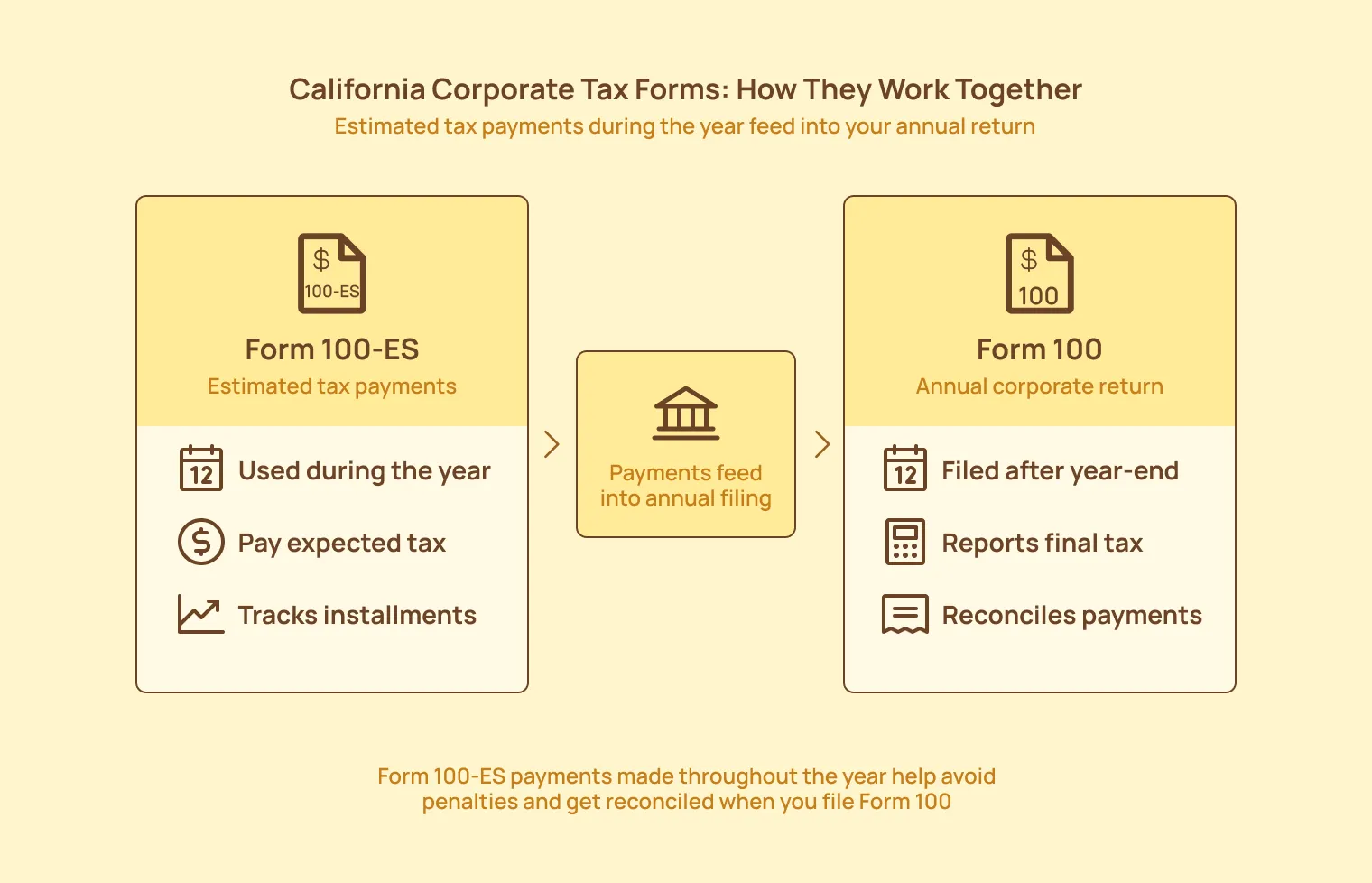

How Is Form 100-ES Different From Form 100?

Form 100 and Form 100-ES are connected, but they are not the same. Form 100 is the annual California corporation return. Form 100-ES is used during the year to make estimated tax payments toward that annual liability.

Delaware C-Corps should not use individual estimated tax forms like Form 540-ES or LLC payment forms like Form 3522 unless a tax advisor confirms a different entity classification.

Which C-Corps Must Make California Estimated Tax Payments?

A corporation may need to make California estimated tax payments if it is incorporated, registered, qualified, or doing business in California and expects to owe California tax. For Delaware C-Corps, this usually becomes relevant when the company has California founders, employees, payroll, operations, customers, or California-apportioned income.

The key point is that Delaware incorporation does not remove California tax duties. If a Delaware C-Corp has enough connection with California, it may need to pay the $800 minimum franchise tax and, in some cases, estimated tax on California taxable income. The California Franchise Tax Board generally expects corporations incorporated, registered, or doing business in California to pay the $800 minimum franchise tax, subject to exceptions.

A Delaware C-Corp should review Form 100-ES requirements if it:

- Is qualified as a foreign corporation in California.

- Has California founders, employees, payroll, or offices.

- Has California-source revenue.

- Has California-apportioned income.

- Expects to owe more than the $800 minimum franchise tax.

- Received an FTB notice or prior-year California tax bill.

Do Pre-Revenue Startups Need to Make Estimated Tax Payments?

A pre-revenue startup may still need to pay the $800 minimum franchise tax if it is subject to California franchise tax. This can apply even when the company has no revenue, operates at a loss, or has limited activity. However, founders should still check whether the first-year minimum franchise tax exemption or the 15-day rule applies before making or skipping a payment.

Does the First-Year Minimum Franchise Tax Exemption Apply?

Newly incorporated or newly qualified corporations may not be subject to the $800 minimum franchise tax for their first taxable year. But this exemption does not remove every California tax issue. If the corporation has California taxable income in the first year, tax may still apply based on income. Founders should review incorporation date, California qualification date, and business activity dates before relying on the exemption.

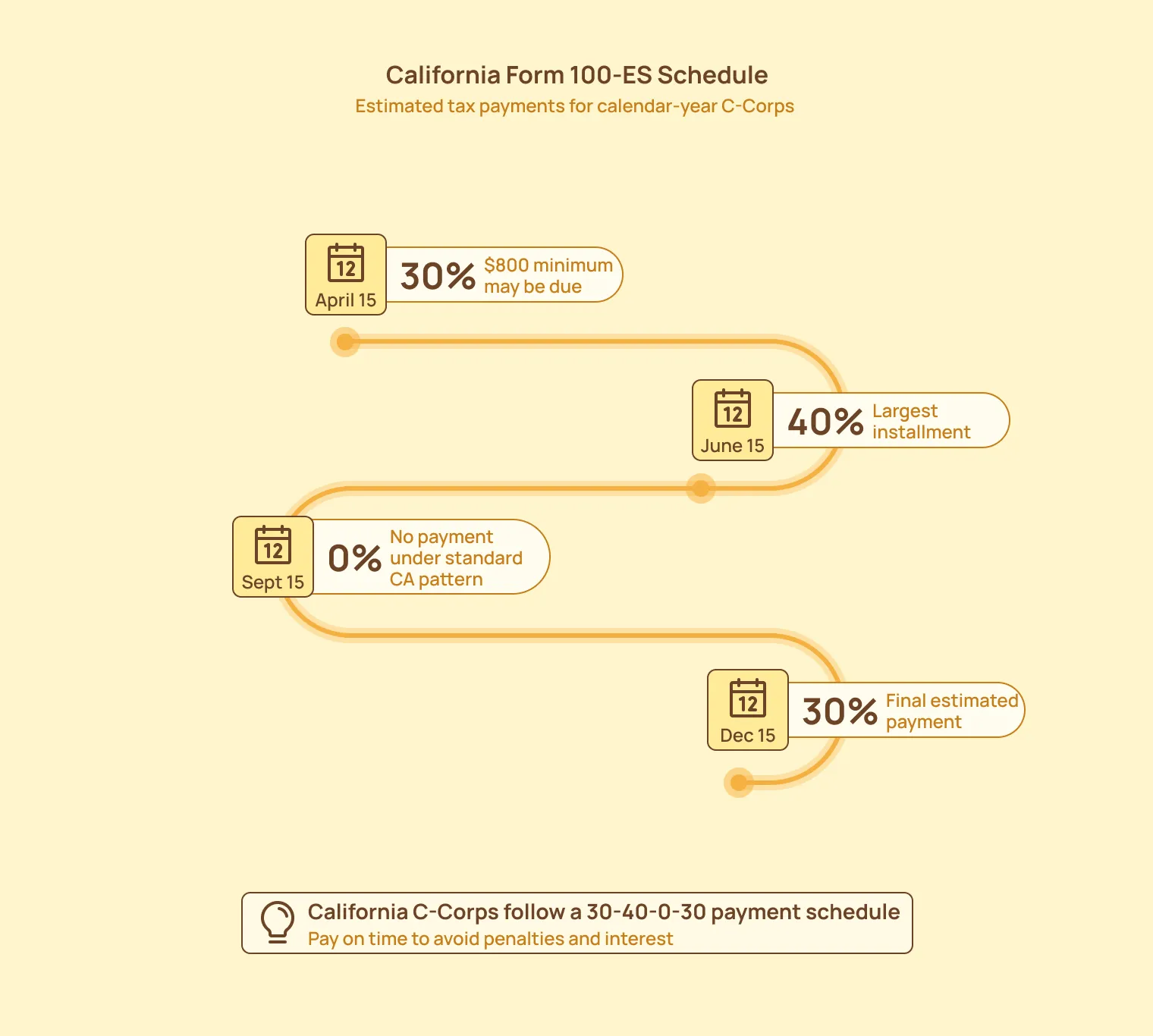

How Does California’s 30-40-0-30 Estimated Tax Schedule Work?

California’s corporate estimated tax schedule is different from the equal quarterly pattern many founders expect. Instead of paying 25% each quarter, corporations generally follow a 30-40-0-30 payment schedule for California estimated tax payments.

This matters because California front-loads most of the estimated tax into the first half of the year. The first installment is generally 30%, the second is 40%, the third is 0%, and the fourth is 30%. So, by June 15, a calendar-year C-Corp may already need to have paid 70% of its estimated California tax liability.

Why There Is No Third California Estimated Tax Payment for C-Corps

California’s standard corporate installment schedule pushes the required third installment to 0%. That does not mean founders can ignore tax planning in September. If revenue grows, California income changes, or earlier estimates were too low, the company should still update its forecast before the fourth installment.

How California Estimated Tax Payments Differ From Federal Payments

Federal and California estimated tax schedules should be tracked separately. A founder who assumes both calendars work the same way can easily miss California’s larger June payment or treat the September 0% installment incorrectly.

Key differences include the following:

- Federal corporate estimated taxes generally use a different installment pattern.

- California uses the 30-40-0-30 schedule for corporations.

- Startups should track federal and California payment calendars separately.

When are California Form 100-ES payments due?

California Form 100-ES payments are generally due in four installments during the corporation’s taxable year. For a calendar-year C-Corp, the standard due dates are April 15, June 15, September 15, and December 15. However, under California’s 30-40-0-30 schedule, the third installment is usually 0%.

This timing matters because the first two payments carry most of the estimated tax burden. If the corporation’s estimated tax does not exceed the minimum franchise tax, the $800 minimum franchise tax is generally due by the 15th day of the fourth month of the taxable year. For calendar-year corporations, that usually means April 15.

What Happens If a Due Date Falls on a Weekend or Holiday?

If a California estimated tax due date falls on a weekend or legal holiday, the deadline generally moves to the next business day. Founders should still confirm the exact dates for the tax year being covered before publishing a calendar or scheduling payments.

Is the Form 100-ES Deadline the Same as the Form 100 Filing Deadline?

No. Form 100-ES payments are made during the tax year. Form 100 is the annual corporation return filed after the tax year ends. For a calendar-year C-corp, Form 100 is generally due on April 15 after year-end, while Form 100-ES payments are made during the year to cover expected California tax.

How Should C-Corps Calculate California Estimated Tax Payments?

C-Corps should calculate California estimated tax payments using expected taxable income, California adjustments, apportionment, credits, prior payments, and the $800 minimum franchise tax, where applicable. For most C-corps, California’s corporate income tax rate is generally 8.84%, excluding banks and financial corporations.

For startups, the estimate should not be treated as a one-time calculation. Revenue, payroll, customer location, and California activity can change quickly during the year. A Delaware C-corp that hires in California, grows California revenue, or expands operations should update its estimates before the next installment date.

Follow this step-by-step process to calculate california Form 100-ES payments:

Step 1: Confirm whether your corporation is subject to California tax

Start by checking whether your company has a California tax obligation. This determines whether Form 100-ES estimated tax payments may apply.

Step 2: Check whether the first-year minimum tax exemption applies

Next, confirm whether your corporation qualifies for the first-year minimum franchise tax exemption. A newly qualified corporation may not owe the $800 minimum franchise tax in its first California tax year.

Step 3: Estimate federal taxable income

Use your expected federal taxable income as the starting point. California corporate tax calculations generally begin with federal income before state-specific adjustments.

Step 4: Adjust for California tax differences

Review whether California treats any income, deductions, or credits differently from federal tax rules. These adjustments can change the amount of income taxable in California.

Step 5: Calculate California-apportioned income

If your startup operates in multiple states, calculate the California share of income. This helps ensure you pay tax only on the portion assigned to California.

Step 6: Apply the California corporate income tax rate

If the company expects taxable income, apply the California corporate income tax rate. Most C-corps use the 8.84% rate.

Step 7: Compare the result with the $800 minimum franchise tax

Compare the calculated tax with the $800 minimum franchise tax, if applicable. The company may need to pay the greater applicable amount.

Step 8: Apply the 30-40-0-30 installment schedule

Break the estimated tax into California’s installment schedule. For calendar-year corporations, this usually means 30% due in the first installment, 40% in the second, 0% in the third, and 30% in the fourth.

Step 9: Subtract prior payments or overpayment credits

Reduce the amount due by any prior estimated payments or overpayment credits from earlier periods. This helps avoid double payment and keeps the calculation accurate.

Step 10: Review the calculation with a CPA before submitting payments

Before submitting payments, have a CPA or tax advisor review the estimate. This helps reduce the risk of underpayment penalties, missed credits, or filing errors.

Multistate startups may not pay California tax on all income. Apportionment determines how much income is assigned to California based on the company’s facts. This matters for Delaware C-Corps with customers, employees, payroll, property, or operations both inside and outside California.

Should Startups Use Prior-Year Tax to Estimate Current Payments?

Prior-year tax can help with planning, but it may not be enough for fast-growing startups. If revenue increases, losses shrink, California activity changes, or the company adds cross-border operations, the prior year may not reflect current tax exposure. Startups should update estimates during the year instead of relying only on last year’s numbers.

How Can C-Corps Pay California Estimated Tax?

C-Corps can pay California estimated tax through Franchise Tax Board business payment options or by mailing Form 100-ES where allowed. For many startups, online payment is easier because it creates a clear payment record and reduces the risk of mailing delays.

The Form 100-ES voucher is used when a corporation makes estimated tax payments during the year. But if the company pays online through FTB Web Pay for Business, it generally should not mail the voucher separately. Startups should keep confirmation records because these payments need to be reconciled before filing Form 100.

Before making a California estimated tax payment, C-corps should:

- Confirm the correct tax year.

- Confirm the correct installment due date.

- Use the corporation’s legal name and identification numbers.

- Select the right payment type.

- Save the payment confirmation.

- Reconcile the payment in the company’s books.

- Share payment proof with the CPA or tax preparer.

Should C-Corps Use WebPay for Business?

Web Pay for Business is often easier to manage than paper vouchers because the company can save confirmations and schedule payments in advance. This is useful for startups that want cleaner records before Form 100 filing, investor diligence, or CPA review. Founders should still confirm whether electronic payment is required based on the company’s tax amount or payment history.

When Should a Startup Mail Form 100-ES?

A startup may mail Form 100-ES when online payment is not used or not available. In that case, the company should use the correct tax year’s voucher, the correct installment, and the latest FTB mailing instructions. If no payment is due, the Form 100-ES voucher generally should not be mailed.

What Penalties Apply if a C-Corp Underpays California Estimated Tax?

A C-Corp can face penalties and interest if it misses California estimated tax deadlines, pays less than required, or forgets to account for the $800 minimum franchise tax. This often happens when founders track federal tax dates but miss California’s different 30-40-0-30 schedule.

Underpayment issues can also create cleanup work later. When the company files Form 100, the Franchise Tax Board may compare the final tax liability with payments made during the year. If payments are missing or too low, the startup may need to deal with notices, interest, penalties, and extra advisor follow-up.

Possible issues include:

- Underpayment penalties.

- Interest on unpaid tax.

- FTB notices.

- Mismatch between Form 100 and estimated payments.

- Cleanup work before fundraising, audits, or diligence.

How Startups Can Reduce Underpayment Risk

Startups can reduce underpayment risk by treating California estimated tax as part of the monthly finance process, not a once-a-year tax task. This is especially important when revenue, payroll, or California activity changes during the year.

To reduce risk:

- Maintain clean monthly books.

- Reforecast California taxable income during the year.

- Track California payroll, revenue, and operations.

- Reconcile each Form 100-ES payment.

- Ask a CPA to review estimates before due dates.

Can a C-Corp Request a Penalty Waiver?

Penalty relief may be available in limited cases, but startups should not rely on waiver requests as a planning method. It is safer to prevent the issue through accurate estimates, calendar reminders, clean books, and saved payment confirmations. A CPA can review whether penalty relief is worth requesting if the company receives an FTB notice.

What Should Delaware C-Corps Watch Out for With Form 100-ES?

Delaware C-Corps often miss California estimated tax requirements because founders assume Delaware formation controls all state tax obligations. But California can still require estimated tax payments when the company is registered, qualified, or doing business in the state. This is especially common when a startup has California founders, employees, payroll, customers, or operations.

The bigger issue is that Form 100-ES mistakes usually show up later. A missed payment in April or June may become a notice, penalty, or reconciliation problem when Form 100 is filed. It can also create avoidable cleanup before fundraising, audits, or diligence.

Common mistakes include:

- Using Form 540-ES instead of Form 100-ES.

- Using LLC Form 3522 instead of corporate payment forms.

- Forgetting the $800 minimum franchise tax.

- Missing the June 15 second installment.

- Treating the third installment as a federal-style payment.

- Not reconciling estimated payments before filing Form 100.

Why Form 540-ES Is Not the Right Form for C-Corps

Form 540-ES is used for individual estimated tax payments. It is not the standard form for Delaware C-Corps paying California corporate estimated tax. A C-Corp should generally use Form 100-ES for California corporation estimated tax payments unless a CPA confirms a different entity classification or filing position.

Why Cross-Border Startups Need Extra Care

Cross-border startups need extra care because California estimates may depend on more than local revenue. A US-India startup may have intercompany expenses, India subsidiary costs, payroll in different locations, and revenue spread across multiple markets. If these records are not clean, the California estimate may be wrong.

Cross-border startups should watch for:

- US-India operations that create intercompany transactions.

- California apportionment tied to revenue and payroll location.

- India subsidiary costs that need clean classification.

- Transfer pricing support and bookkeeping records that align with tax filings.

How Can Inkle Help C-Corps Manage California Estimated Tax Payments?

California estimated tax payments are easier to manage when the company’s books, payment records, and compliance calendar are already organized. For Delaware C-Corps, this becomes more important when California tax deadlines run alongside federal filings, payroll, investor reporting, and cross-border finance work.

Inkle helps startups keep bookkeeping and compliance records ready throughout the year. That makes it easier to estimate tax, track Form 100-ES payments, reconcile those payments before Form 100 filing, and respond quickly if advisors or investors ask for records. This is especially useful for Delaware C-Corps with California and US-India operations.

With Inkle, startups can:

- Keep bookkeeping records ready for tax estimates.

- Track California compliance workflows and due dates.

- Organize Form 100-ES payment confirmations.

- Support Delaware C-Corps with US and cross-border operations.

- Stay prepared for tax filings, fundraising, and diligence.

Keep California Estimated Tax Payments on Track

Inkle helps Delaware C-Corps manage bookkeeping, tax records, and compliance workflows across states and borders.

Keep Form 100-ES payments, Form 100 filings, and payment confirmations organized before deadlines or investor review.

Book a demo with Inkle to keep California estimated tax payments and compliance records ready for review.

Frequently Asked Questions

What is California Form 100-ES?

California Form 100-ES is the corporation's estimated tax form. C-corps use it to calculate and pay estimated California franchise or income tax during the tax year, before filing the annual Form 100 return.

Does a Delaware C-corp need to make California estimated tax payments?

A Delaware C-corp may need to make California estimated tax payments if it is registered, qualified, or doing business in California and expects to owe California tax. This can include companies with California founders, payroll, customers, operations, or California-apportioned income.

What is California’s 30-40-0-30 schedule for C-corps?

California’s standard corporate estimated tax schedule generally requires 30% of estimated tax with the first installment, 40% with the second installment, 0% with the third installment, and 30% with the fourth installment. This is different from the equal quarterly payment pattern many founders expect.

When are California estimated tax payments due for a calendar-year C-corp?

For a calendar-year C-corp, California estimated tax payments are generally due on April 15, June 15, September 15, and December 15. Under California’s standard C-Corp schedule, the September installment is usually 0%.

Does a pre-revenue C-corp need to pay California estimated tax?

A pre-revenue C-corp may still owe the $800 minimum franchise tax if it is subject to California franchise tax. However, first-year and 15-day rule exceptions may apply. Founders should confirm the company’s facts before paying or skipping the payment.

Can a C-corp pay California estimated tax online?

Yes. C-Corps can generally use FTB Web Pay for Business to make California estimated tax payments. Online payment is often easier to track because the company can save confirmations and reconcile payments before Form 100 filing.

In this article