What is California Franchise Tax for Delaware C-Corps?

.webp)

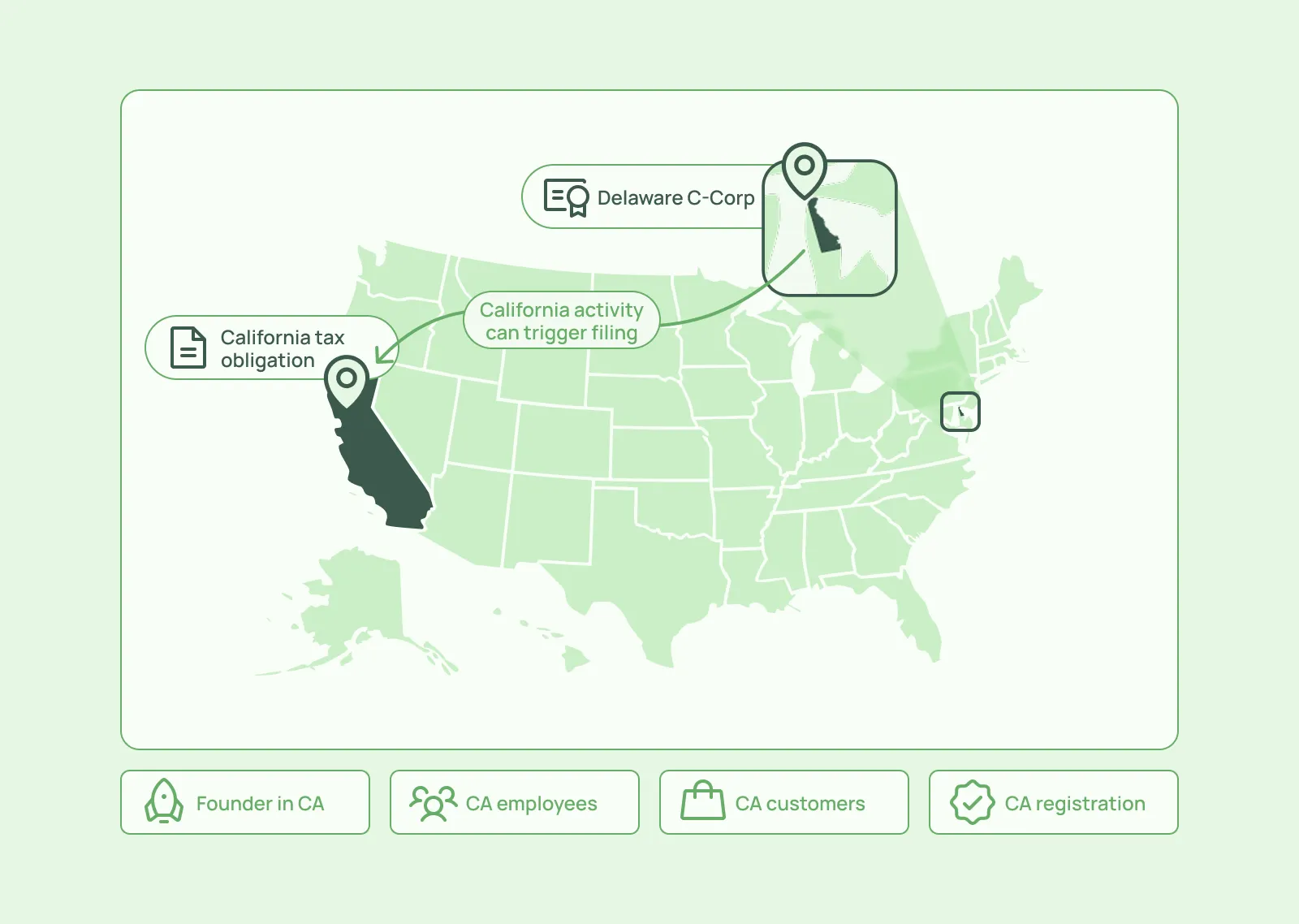

Startups choose a Delaware C-Corp because it is familiar to investors, common for venture-backed companies, and easier to standardize during fundraising. But Delaware incorporation does not mean the company only has Delaware tax obligations. If the startup operates, hires, sells, or has founders in California, it may also need to deal with the California Franchise Tax Board.

A company can be incorporated in Delaware and still owe California franchise tax if it is registered or doing business in California. For example, a Delaware C-Corp with a founder working from San Francisco, California payroll, or California customers may create a California filing obligation even though the company was formed in Delaware.

California franchise tax matters because it can apply even before the startup is profitable. The company may need to file Form 100, pay the $800 minimum franchise tax after the first taxable year, make estimated tax payments, and keep records that may be checked during fundraising or diligence.

This article breaks down when the tax applies, how the $800 minimum works, what the first-year exemption means, and how Delaware C-Corps can stay compliant without last-minute cleanup.

What Is California Franchise Tax?

California franchise tax is a tax charged for the right to do business in California. It can apply to corporations that are incorporated in California, registered in California, qualified to do business in California, or actually doing business in the state.

For Delaware C-Corps, this matters because the legal state of formation is only one part of the picture. A Delaware company can still fall under California tax rules if its business activity is connected to California. The California Franchise Tax Board generally expects corporations incorporated, registered, or doing business in California to pay at least the $800 minimum franchise tax, unless an exception applies.

California franchise tax can be tied to:

- California incorporation.

- California registration or qualification.

- Doing business in California.

- California-source income or operations.

Why Delaware C-Corps Need to Care About California Franchise Tax

Delaware may be the state where the company is formed, but California can still tax the company if it operates there. This is common for startups because founders, employees, customers, and operations are often spread across states.

A Delaware C-corp may create a California tax obligation when:

- A founder works from California.

- The company hires California employees or contractors.

- The company uses a California office or coworking space.

- The company sells to California customers.

- The company registers as a foreign corporation in California.

What Doing Business in California Means for Startups

For startups, “doing business” in California can mean more than having an office there. It may include operating from California, hiring in California, managing the company from California, holding inventory in the state, or earning income from California customers. The exact answer depends on facts such as revenue, payroll, property, founder location, employee location, and registration status. Founders should review their California nexus position with a CPA before assuming they are outside the state’s filing rules.

What Is the California $800 Minimum Franchise Tax?

The California $800 minimum franchise tax is the baseline amount many corporations owe for the right to do business in California. It can apply even when the company has low revenue, no profit, or limited activity in the state.

For Delaware C-Corps, this means California tax exposure is not only about profit. A startup may be loss-making and still have a California filing and payment obligation if it is qualified, registered, or doing business in California. Inkle’s California tax memo also notes that Form 100 must be filed every year once the corporation has a California filing obligation, even in loss years or zero-revenue years.

Which Delaware C-Corps Must Pay the $800 Minimum Tax?

A Delaware C-Corp may need to pay the $800 minimum franchise tax if California treats it as registered, qualified, or doing business in the state. This often applies once the company has a legal or operational connection to California.

This can include:

- Delaware C-Corps qualified to do business in California.

- Delaware C-Corps actually doing business in California.

- Startups with California operations or payroll.

- Startups registered with the California Secretary of State.

Do Inactive or Dormant Startups Still Owe California Franchise Tax?

Being inactive does not always remove the California filing or payment obligation. If the corporation remains registered or subject to California tax rules, it may still need to file and pay unless an exception applies. In many cases, a company must formally withdraw, dissolve, or cancel its California status to stop future obligations.

Does the First-Year Franchise Tax Exemption Apply to Delaware C-Corps?

California provides a first-year minimum franchise tax exemption for newly incorporated or newly qualified corporations. This means a newly qualified Delaware C-Corp may not have to pay the $800 minimum franchise tax in its first California taxable year. However, this does not always mean the company has no California filing responsibility or no California tax exposure at all.

The exemption mainly applies to the $800 minimum franchise tax. If the Delaware C-Corp has California-source income, it may still owe measured tax based on income apportioned to California. Inkle’s California memo also notes that newly incorporated or qualified corporations are not subject to the $800 minimum franchise tax in their first California taxable year, but they may still owe tax on California-source net income.

How the First-Year Exemption Works for a Newly Qualified Delaware C-Corp

A Delaware C-Corp that newly qualifies to do business in California may be exempt from the $800 minimum franchise tax for its first taxable year. But the company may still need to file California Form 100. It may also owe California tax if it has taxable income connected to California. For example, if the company qualifies in California in 2026 and operates at a loss, the $800 minimum may not apply for that first year. If it has California-apportioned net income, measured tax may still apply.

What Should You Check Before Claiming the First-Year Exemption

Founders should confirm the company’s facts before assuming the exemption applies. The key question is not only when the company was formed, but when and how it became connected to California.

Check:

- The date of Delaware incorporation.

- The date of California qualification.

- Whether the company did business in California before registering.

- Whether the company has California-source income.

- Whether the company has a short taxable year or regular taxable year.

What is the California 15-Day Rule?

The California 15-day rule is a narrow rule that can help some businesses avoid a short-year filing and minimum tax obligation. It may apply when a business has a taxable year of 15 days or fewer and does no business in California during that short period. Both conditions matter. The period must be 15 days or fewer, and the company must have no California business activity during that time.

For Delaware C-Corps, this usually comes up when a company qualifies or registers in California near year-end. The rule can be helpful, but founders should not assume it applies automatically. If the company starts operating, signs customers, pays employees, earns California income, or otherwise does business in California during that short period, the rule may not apply.

For example, assume a calendar-year Delaware C-Corp qualifies in California on December 20 and does no California business before December 31. That short period may fall under the 15-day rule. But if the company signs California customers, pays California employees, or starts operating in California during that period, the company may need to file and review whether tax is due.

Why the 15-Day Rule Matters for Year-End Incorporations

The 15-day rule matters because many founders incorporate, qualify, or register entities near the end of the year without thinking about short-period tax filings. In limited cases, the rule may prevent an unnecessary California filing for that short tax year. But it only works when the company has no California business activity during that period, so founders should confirm the facts before relying on it.

When Is California Franchise Tax Due for Delaware C-Corps?

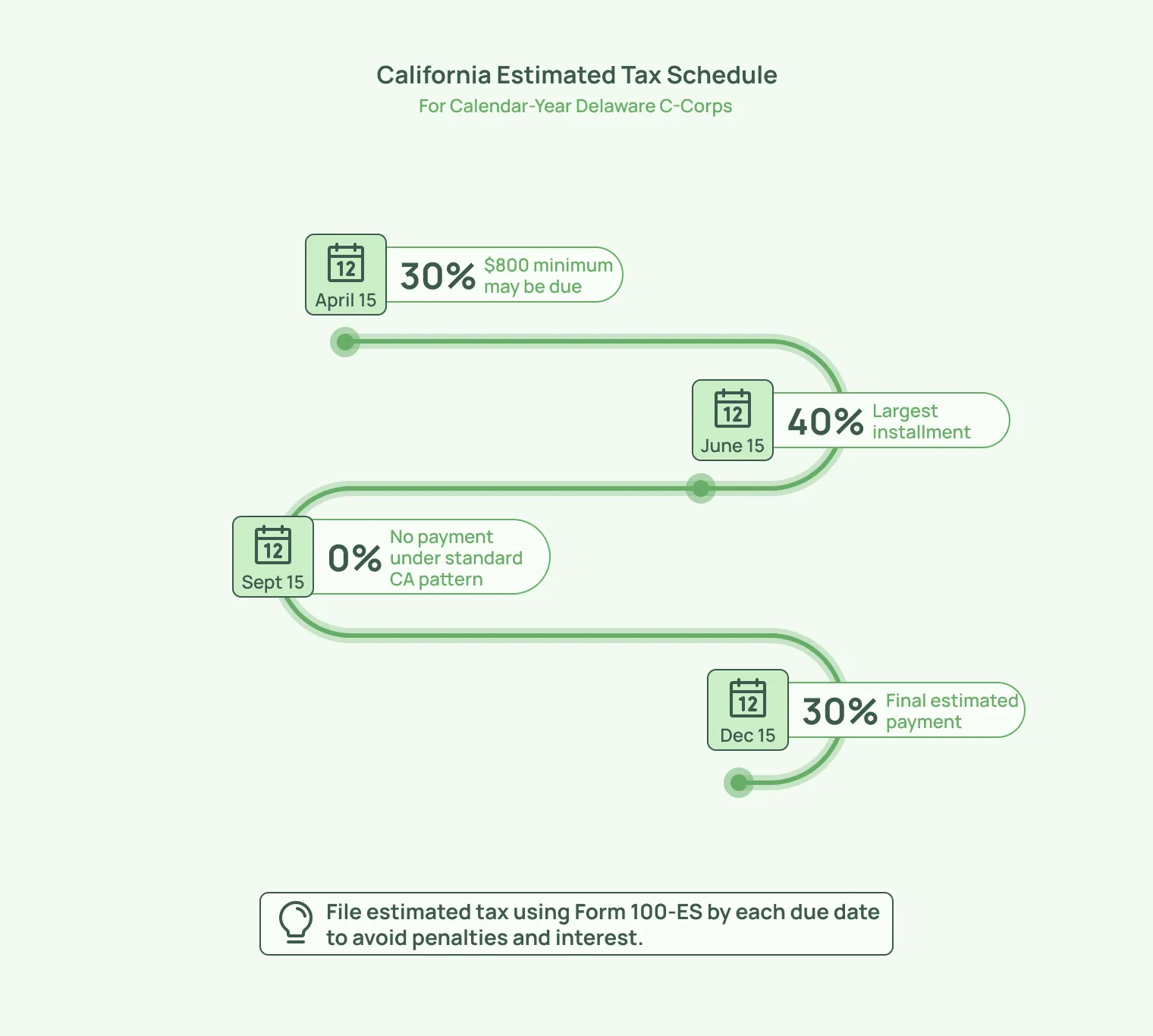

For Delaware C-corps, California due dates usually follow the corporation’s tax year. A calendar-year C-corp generally files California Form 100 by April 15, which is the 15th day of the fourth month after the tax year ends. Any total tax owed is also due by the original return due date, not the extended filing date.

Estimated tax payments follow a separate schedule during the tax year. Corporations generally need to make estimated tax payments only if they expect their income tax (after credits) to be $500 or more for the year. California corporation estimated tax installments are generally due in the fourth, sixth, ninth, and twelfth months of the taxable year. Common California installment patterns are 30%, 40%, 0%, and 30%, with the first installment due on April 15 for calendar-year corporations. It also notes that if only the $800 minimum applies, the full $800 is generally due with the first installment.

How C-Corp Due Dates Are Different From LLC Due Dates

Founders often mix up California corporation and LLC payment rules. A Delaware C-Corp should generally follow corporation filing and payment rules, not LLC rules.

- C-Corps generally file California Form 100.

- LLCs generally file Form 568 and may use Form 3522 for the $800 annual tax.

- Do not use LLC payment forms for a Delaware C-corp unless a CPA confirms that the entity’s tax structure requires it.

What Happens If a Startup Misses a California Franchise Tax Deadline?

Missing California franchise tax deadlines can create more than a late fee. The company may receive FTB notices, accrue penalties and interest, and risk falling out of good standing. This can become a problem during fundraising, legal diligence, bank reviews, or state registrations.

Possible consequences include:

- Penalties for late filing or late payment.

- Interest on unpaid tax.

- Notices from the California Franchise Tax Board.

- Loss of good standing or suspension risk.

- Avoidable issues during fundraising, diligence, or state registrations.

How Can Delaware C-Corps Pay California Franchise Tax?

Delaware C-Corps should use California corporation tax forms and payment channels when paying California franchise tax. The right method depends on what the company is paying, whether it is making an estimated tax payment, and whether it has already triggered electronic payment requirements. For most startups, the common forms are California Form 100 for the annual corporation return and Form 100-ES for estimated tax payments.

California also offers online payment options such as FTB Web Pay, which allows businesses to make payments directly from a US bank account. Inkle’s California memo notes that Web Pay is often the default method for startups, while EFT becomes mandatory once a corporation makes any single estimated tax or extension payment exceeding $20,000, or has a total tax liability exceeding $80,000. Startups should save payment confirmations because these records may be requested during tax prep, diligence, or compliance reviews.

Before paying California franchise tax, founders should:

- Confirm the company’s California filing status.

- Confirm whether the first-year minimum tax exemption applies.

- Calculate whether only the $800 minimum or a larger tax amount is due.

- Use the correct corporation payment method.

- Save payment confirmation for diligence and audit records.

Should Delaware C-Corps Use FTB Form 3522?

Usually, no. Form 3522 is an LLC Tax Voucher, so it is generally not the right form for a Delaware C-Corp. Delaware C-Corps usually use corporation forms such as Form 100 and Form 100-ES, depending on the filing or payment. LLCs follow different California filing rules, so founders should avoid using LLC forms unless their CPA confirms that the company’s structure or tax treatment requires it.

Should Startups Pay Online or by Mail?

Online payment is usually easier to track because the company can save confirmation details immediately. Mailed payments require more care because the startup must use the correct voucher, mailing address, payment memo, and proof of mailing. If a startup is close to a deadline, online payment may also reduce avoidable mailing delays.

How Is California Franchise Tax Different for C-Corps, S-Corps, and LLCs?

California tax rules differ by entity type, which is why founders should not copy forms or due dates from another company without checking the structure first. A Delaware C-Corp usually follows corporation rules, while LLCs and S-Corps follow different filing paths, payment forms, and tax calculations.

For Delaware C-Corp founders, the main point is simple: do not use LLC rules as a shortcut. C-Corps generally need to think about Form 100, the $800 minimum franchise tax, estimated tax payments, and measured tax on California-apportioned income. Inkle’s California memo notes that California charges C-Corps the greater of the $800 minimum franchise tax or 8.84% measured tax on net income apportioned to California.

Can California Franchise Tax Affect Fundraising and Good Standing?

California franchise tax compliance can come up during fundraising, due diligence, investor onboarding, bank reviews, or acquisition checks. Investors and counsel may not only review Delaware incorporation documents. They may also check whether the company is properly qualified in California, whether Form 100 has been filed, and whether payments to the California Franchise Tax Board are current.

This matters because missed filings or payments can create avoidable delays. A startup that is behind on California taxes may need to clear FTB notices, pay penalties, restore good standing, or explain gaps during diligence. Inkle’s California memo also notes that continued non-filing or non-payment can lead to FTB suspension, which can affect the corporation’s ability to use its name, defend itself in California courts, or close transactions.

California franchise tax issues can affect fundraising because:

- Investors may ask for state tax filings.

- Counsel may check California qualification status.

- Missed FTB payments can create avoidable diligence issues.

- Late filings can lead to notices, penalties, and interest.

- Clean state compliance helps avoid delays during funding rounds.

How Can Inkle Help Delaware C-Corps Stay Compliant in California?

California franchise tax compliance is easier to manage when bookkeeping, filing calendars, payment records, and state registrations are not scattered across emails, spreadsheets, and advisor threads. For Delaware C-Corps, this matters because California obligations can run in parallel with federal tax filings, Delaware compliance, payroll, and investor reporting.

Inkle helps startups keep finance and compliance work organized, especially when teams operate across the US, India, and other markets. For California, that means cleaner books, better filing records, and fewer last-minute gaps before tax deadlines, fundraising, or diligence.

With Inkle, Delaware C-Corps can:

- Track compliance workflows across federal and state requirements.

- Maintain cleaner books for California tax reporting.

- Support US and cross-border finance operations in one place.

- Organize filing records, payment confirmations, and tax documents.

- Prepare clearer reporting before fundraising, audits, and diligence.

Book a demo with Inkle to keep your California compliance and startup books ready for review.

Frequently Asked Questions

Does a Delaware C-corp have to pay California franchise tax?

A Delaware C-corp may have to pay California franchise tax if it is registered, qualified, or doing business in California. Delaware incorporation does not remove California obligations if the company has founders, employees, operations, customers, or income connected to California.

What is the California $800 minimum franchise tax?

The California $800 minimum franchise tax is the baseline tax many corporations owe for the right to do business in California. It can apply even when the company has low revenue, no profit, or limited activity, unless an exemption or exception applies.

Does California waive the $800 minimum tax for a new Delaware C-Corp?

California generally waives the $800 minimum franchise tax for newly incorporated or newly qualified corporations in their first taxable year. However, the company may still need to file and may owe tax based on California-source income or activity.

What is the California 15-day rule for startups?

The California 15-day rule may apply when a business has a taxable year of 15 days or fewer and does no business in California during that period. If both conditions are met, the business may not need to file a California return or pay the $800 minimum tax for that short period.

When is the California franchise tax due for a calendar-year C-corp?

For a calendar-year C-corp, California Form 100 and the total tax payment are generally due on April 15. Estimated tax installments usually follow California’s fourth, sixth, ninth, and twelfth month schedule.

Should a Delaware C-corp use Form 3522 to pay California franchise tax?

Usually, no. Form 3522 is an LLC tax voucher. Delaware C-Corps generally use corporation forms such as Form 100 and Form 100-ES, depending on the filing or payment.

In this article