Section 1202 QSBS Explained for Founders

Imagine selling your company for $20 million and paying zero federal capital gains tax on the gain. No $4 million federal tax bill. No 3.8% net investment income tax. Just the full $20 million to keep (assuming other conditions are met).

This is not fantasy. This is Section 1202 of the Internal Revenue Code, and it is one of the most powerful tax incentives Congress has created for startup founders and early investors.

For years, Section 1202 was a well-kept secret among sophisticated entrepreneurs. It required holding stock for five years to get the full benefit, and the cap was just $10 million in gains. Most founders never thought they would need it because they assumed their company would never be worth that much.

Everything changed on July 4, 2025, when President Trump signed the One Big Beautiful Bill Act (OBBBA). The law significantly expanded Section 1202, raising the gain exclusion cap to $15 million, allowing partial exclusions for stock held just three years, and raising from $50 million to $75 million.

If you founded a company, you have options, or you soon will. Before you plan your exit, before you accept an acquisition offer, before you negotiate a purchase price, you need to understand Section 1202 QSBS and whether your stock qualifies.

What is section 1202 QSBS?

Section 1202 is a federal tax law that allows individuals to exclude up to 100 percent of the capital gain from the sale of qualified small business stock (QSBS) under specific conditions.

In plain English: If you own stock in a company that qualifies under Section 1202, and you hold it long enough, and you sell it, you do not pay federal capital gains tax on your gain.

The law was enacted in 1993 as part of the Omnibus Budget Reconciliation Act to encourage investment in small businesses. Congress believed that if investors knew they could exclude capital gains, they would be more likely to take risks on startups, invest in early-stage companies, and help small businesses grow.

It worked. Over the past 30 years, Section 1202 has saved billions in taxes for founders and early investors.

The tax savings math:

To understand why Section 1202 matters, consider the tax burden on selling appreciated stock normally.

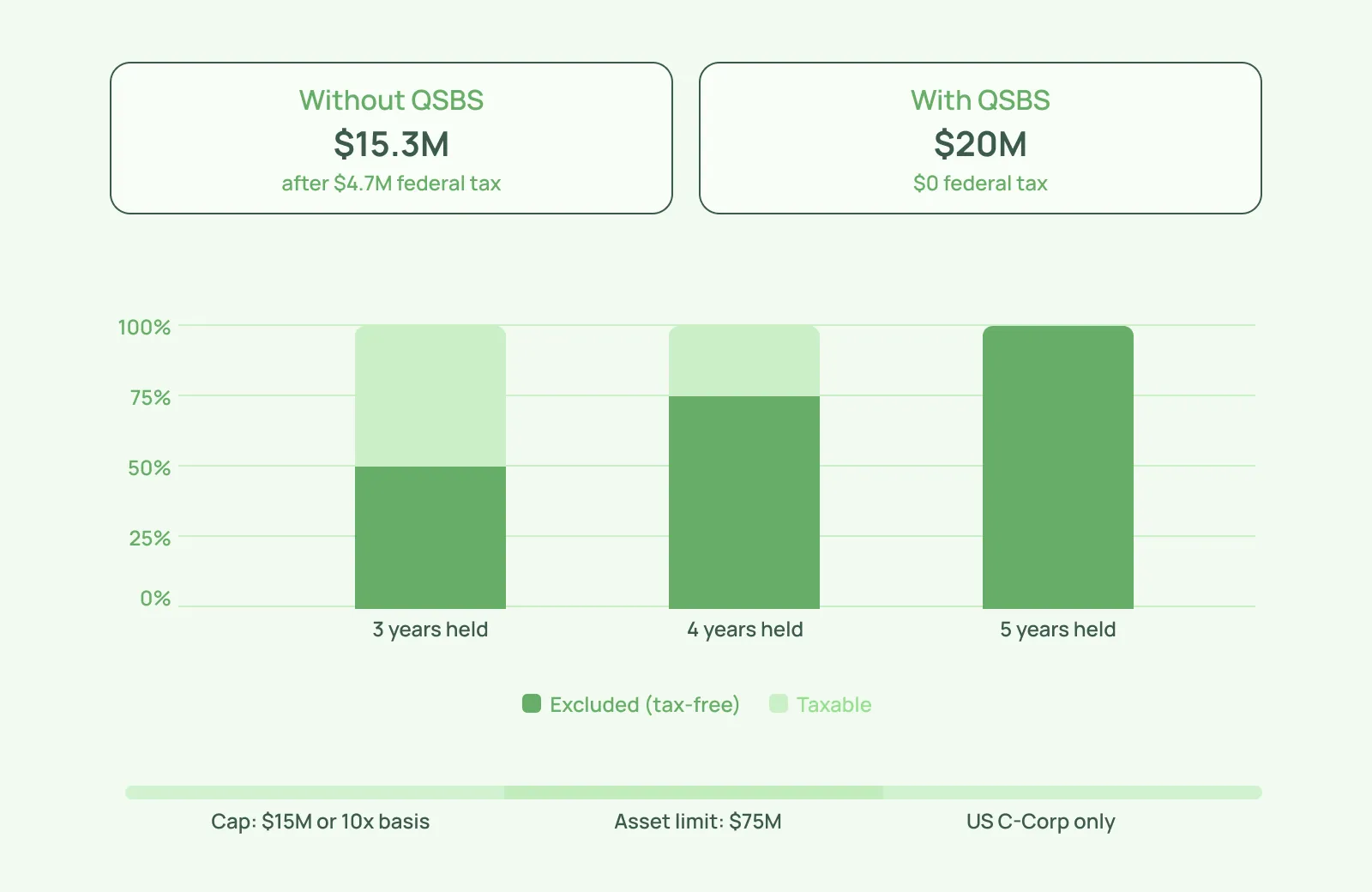

If you sell stock for $20 million and your basis (original investment cost) is $100,000, your capital gain is $19,900,000.

Under normal tax rules for long-term capital gains (held over one year), your federal tax would be:

- 20% federal long-term capital gains tax: $3,980,000

- 3.8% net investment income tax (NIIT): $756,200

- Total federal tax: $4,736,200

Your net proceeds: $15,263,800

With Section 1202 (assuming you qualify for the full 100% exclusion):

- Federal tax on excluded gain: $0

- Federal tax: $0

- Your net proceeds: $20,000,000

The difference: $4,736,200 in federal taxes saved.

Many states also follow federal treatment, so you may save additional state income taxes (potentially another 5 to 13 percent depending on your state). In California, the total tax savings could exceed $7 million.

This is why Section 1202 planning is critical for any founder with a valuable company.

How much gain can you exclude?

The amount of gain you can exclude depends on when your stock was issued and how long you have held it.

For stock issued after July 4, 2025 (OBBBA Rules)

If your stock was issued after July 4, 2025, you can exclude the following percentage of your gain:

50 percent exclusion for stock held at least 3 years 75 percent exclusion for stock held at least 4 years 100 percent exclusion for stock held at least 5 years

The exclusion is capped at the greater of:

- $15 million in gain, or

- 10 times your original investment (basis)

Example: You invested $500,000 in a startup in 2022, and the company sold in 2027 (5 years later). The sale price is $20 million, and your basis is $500,000. Your gain is $19,500,000.

Your exclusion limit is the greater of:

- $15 million, or

- 10 times $500,000 = $5,000,000

The greater amount is $15 million, so your maximum exclusion is $15 million.

You would exclude $15 million of the $19,500,000 gain, leaving $4,500,000 subject to tax.

Federal tax on $4,500,000 at 23.8% (including NIIT): $1,071,000

Savings: $4,631,000 in federal taxes

For stock issued on or before July 4, 2025 (Pre-OBBBA Rules)

If your stock was issued before July 4, 2025, the old rules apply:

50 percent exclusion for stock issued between September 28, 2010, and July 4, 2025, if held more than 5 years 100 percent exclusion for stock issued after September 28, 2010, but before July 4, 2025, if held more than 5 years

The exclusion is capped at the greater of:

- $10 million in gain, or

- 10 times your basis

You cannot upgrade to the new OBBBA rules by selling and reissuing stock. Once stock is issued, it retains the rules that existed at the time of issuance.

The 10X basis cap

The 10X basis cap is important because it allows high-growth founders to exclude significantly more than $15 million or $10 million if their investment basis is large enough.

Example: You invested $2 million in a company in 2021. Ten years later, the company sells for $250 million. Your gain is $248 million.

For stock issued before July 4, 2025, the exclusion cap is the greater of $10 million or 10 times your basis.

10X your basis: 10 times $2,000,000 = $20 million

The greater amount is $20 million, so you can exclude up to $20 million of your $248 million gain.

Excluded gain: $20 million Taxable gain: $228 million Federal tax on $228 million at 23.8%: $54,264,000

Without Section 1202, federal tax would be: $58,936,000

Savings: $4,672,000

Who can use section 1202?

Section 1202 is available only to non-corporate taxpayers. This includes:

- Individuals (you, if you own the stock personally)

- Trusts (with specific conditions)

- Estates

- Pass-through entities (partnerships, S-corporations) under certain conditions if their owners are non-corporate

Notably, corporations cannot use Section 1202. If a C-corporation owns stock in another corporation, it cannot claim the exclusion. This is why founders typically own stock personally, not through holding companies.

If you are a pass-through entity owner (i.e., you own the company through an LLC or partnership), the gain may flow through to you as a non-corporate owner, and you may still claim the exclusion. However, there are additional rules and conditions that apply. Consult a tax professional if you own stock through a pass-through entity.

What companies qualify for QSBS?

Not every stock qualifies. The company issuing the stock must meet specific criteria at the time the stock is issued.

Requirement 1: Domestic C Corporation

The company must be a domestic C-corporation. This means:

The company must be incorporated in the United States (any state, not just Delaware, though Delaware is most common for startups). The company must have elected to be treated as a C-corporation for federal tax purposes.

Pass-through entities do not qualify. If you are incorporated as an S-corporation or LLC, your stock does not qualify for Section 1202, period. This is the most common disqualifier, and it is permanent. You cannot fix this by converting to a C-corporation later. The old stock remains disqualified.

You can convert an LLC to a C-corporation and issue new stock, but only the stock issued after conversion qualifies. All the old LLC shares remain ineligible.

Requirement 2: Gross assets do not exceed the threshold

At the time your stock is issued, the company's aggregate gross assets cannot exceed:

$75 million (for stock issued after July 4, 2025) $50 million (for stock issued on or before July 4, 2025)

Gross assets include cash plus the adjusted basis of all property held by the corporation. Adjusted basis is typically the fair market value at the time property was contributed to the company.

This is where many high-growth companies lose QSBS status. If a company raises Series A funding, its assets may jump from $5 million to $80 million overnight. If the company's assets exceed the threshold at the time the Series A shares are issued, those shares do not qualify as QSBS.

The threshold is checked at the time of issuance and immediately after issuance. If the company crosses the threshold between issuance and the next day, the stock is still disqualified.

Example: A company has $49 million in assets at 11:59 pm. At midnight, it received a funding wire for $30 million, bringing assets to $79 million. Any shares issued after the funding wire was received do not qualify.

Requirement 3: Active business requirement

At least 80 percent of the company's assets must be used in the active conduct of one or more "qualified trades or businesses" during substantially all of your holding period.

This means the company cannot be primarily a holding company or investment vehicle. It must be actively operating a business.

Common violations:

- Holding excess cash (if cash exceeds 20 percent of assets, the company may fail this test)

- Holding investment securities or passive assets

- Real estate leasing or passive real estate operations

- Excess affiliate stock

Importantly, this test is not just evaluated at the time of issuance. It applies during substantially all of your holding period. If the company fails this test at any point and stays in failure for a significant time, the stock may lose QSBS status permanently.

Example: Your company has $10 million in cash (20 percent of $50 million in assets) and $40 million in operating assets. The company then raises a Series B and receives $100 million, bringing cash to $110 million (68 percent of the new $160 million total). The company is now failing the active business test because more than 20 percent of assets are passive cash.

If this condition persists, the stock may be disqualified retroactively.

Requirement 4: Qualified trade or business

The company must operate a qualified trade or business. This means it cannot primarily operate in the following excluded industries:

Banking, insurance, finance, or investment (including leasing) Hospitality (hotels, restaurants, bars) Law, accounting, consulting, or other professional services where the principal asset is the reputation or skill of employees Health, veterinary, or other services of this kind Foreign investment companies or passive foreign investment companies (PFICs) Cooperatives or mutual companies Corporations engaged in farming or mineral extraction

Many service-based companies fall into excluded categories. For example:

- A consulting firm: Excluded (professional service)

- A law firm: Excluded (professional service)

- A staffing agency: Excluded (professional service)

- A real estate brokerage: Excluded (service where reputation matters)

- A management consulting firm: Excluded (professional service)

- A software company: Generally qualifies (active business)

- A SaaS company: Qualifies (active business)

- A manufacturing company: Qualifies (active business)

- A retail business: Qualifies (active business)

- A restaurant: Excluded (hospitality)

- A hotel: Excluded (hospitality)

- A financial services firm: Excluded (finance)

If your company is primarily in an excluded industry, no amount of planning will make your stock qualify. Section 1202 is not available to you.

Requirement 5: Original issuance

You must acquire the stock directly from the company at its original issuance. You cannot buy QSBS on the secondary market.

This means:

- If you purchase stock in a company's Series A round, you qualify

- If you exercise options that were granted by the company, you qualify (the holding period begins on the date of exercise)

- If you receive restricted stock awards, you qualify if you made a timely Section 83(b) election

- If you buy stock from another shareholder, you do not qualify

For founders who receive founder stock, the holding period typically begins on the date the company issued the stock. If you received founder shares on the date of incorporation (which is standard), your holding period began on that date.

The holding period requirement

When you can claim the Section 1202 exclusion depends on how long you have held the stock.

For stock issued after July 4, 2025 (OBBBA)

3 years: 50% exclusion 4 years: 75% exclusion 5 years: 100% exclusion

For stock issued before July 4, 2025 (Pre-OBBBA)

- 5 years: 100% exclusion (for stock issued after September 28, 2010)

- 5 years: 50% exclusion (for stock issued between August 11, 1993, and September 27, 2010)

You cannot benefit from the shorter holding periods if your stock was issued before the OBBBA date. The law does not allow retroactive application.

The holding period begins on the date the stock was issued to you, not the date you paid for it or the date the company was incorporated (unless you received it on incorporation).

For stock acquired through option exercise, the holding period begins on the exercise date, not the grant date. This is important because it means your holding period clock resets each time you exercise options.

For restricted stock or stock subject to a vesting schedule, if you made a Section 83(b) election, the holding period begins on the date of issuance. If you did not make the election, it begins on the date the stock vests.

Common mistakes that disqualify QSBS

Section 1202 is powerful, but it is also fragile. Small mistakes can permanently disqualify your stock.

Mistake 1: Incorporating as an LLC or S-Corp instead of a C-Corp

This is the most common and most permanent mistake. If you incorporated as an LLC and never converted to a C-corporation, your stock will never qualify for Section 1202.

If you converted to a C-corp later, only stock issued after the conversion qualifies. All pre-conversion shares remain ineligible.

Solution: If you have not yet incorporated, incorporate as a Delaware C-Corporation from day one. If you are already incorporated as an LLC or S-Corp, convert to a C-Corporation before issuing any shares. The conversion does not trigger income tax, but it restarts your holding period clock for Section 1202.

Mistake 2: Exceeding the gross asset threshold

If your company's assets exceed $75 million at the time of share issuance, the stock issued at that time does not qualify.

High-growth companies often lose QSBS status when they raise large funding rounds. A company with $40 million in assets that raises a Series B funding round of $100 million may exceed the threshold during the funding process.

Solution: Be mindful of the asset threshold during funding rounds. Discuss QSBS implications with your investors and advisors. If possible, structure funding to keep assets under the threshold (e.g., staging the funding across multiple closes, using convertible notes instead of equity in the first round).

Mistake 3: Failing the active business test

If your company accumulates excess cash (more than 20 percent of total assets), invests in passive securities, or holds non-operating assets, it may fail the active business test.

This test is evaluated throughout your holding period, not just at issuance. If your company fails for a sustained period, your stock may be permanently disqualified.

Solution: Monitor your company's asset composition. If you accumulate significant cash, consider returning it to shareholders through dividends or buybacks, or reinvest it in operating assets.

Mistake 4: Not filing an 83(b) Election

If your stock is restricted (subject to a vesting schedule), you must file an 83(b) election with the IRS within 30 days of receiving the stock to start your holding period clock.

Without the election, your holding period does not begin until the shares vest. This could delay your eligibility by years.

Solution: File an 83(b) election for all restricted stock within 30 days of receipt. This is absolutely critical for founders and early employees.

Mistake 5: Holding stock through a C-Corporation

As a founder, if you own your company stock through a holding company or C-corporation instead of personally, you cannot claim the Section 1202 exclusion. Only individuals, trusts, and estates can claim it.

Solution: Own your stock personally, not through a corporate entity. If you already own it through a corporation, there may be a way to restructure before selling, but consult a tax professional immediately.

Section 1202 and exit planning

QSBS status should influence how you plan your exit.

Stock sale vs Asset sale

Section 1202 applies only to stock sales, not asset sales. If you sell the company's assets instead of selling the stock, Section 1202 does not apply.

In a stock sale, the buyer purchases 100 percent of the company's stock, and you receive the purchase price.

In an asset sale, the buyer purchases the company's assets (equipment, customer contracts, IP, etc.), and the company remains as an empty shell with cash. You then liquidate the company, and any remaining cash (gain) is distributed to shareholders.

Section 1202 applies to the gain on the stock sale itself, not the gain on the asset sale.

If your company qualifies for QSBS and you have a choice between a stock sale and an asset sale, the stock sale is strongly preferable from a tax perspective. The buyer may prefer an asset sale for their own reasons (to avoid inheriting liabilities, to reset asset basis, etc.), but you should negotiate a tax-gross-up or higher price to compensate for the loss of Section 1202 benefits.

A $20 million stock sale with QSBS benefits may result in $15 million in after-tax proceeds. A $20 million asset sale without QSBS benefits results in approximately $15.2 million in after-tax proceeds (after corporate-level tax and individual-level tax).

The difference is small in absolute terms, but it reflects the value of QSBS planning.

Section 1045 rollover

There is an alternative to claiming the Section 1202 exclusion called a Section 1045 rollover.

Section 1045 allows you to defer capital gains from the sale of QSBS if you reinvest the proceeds in new QSBS within 60 days.

This is useful if:

- You want to sell early (before the holding period for Section 1202 is satisfied)

- Your gain exceeds the Section 1202 cap, and you want to reinvest excess proceeds without immediate tax

- You want to diversify your holdings by selling one company and buying stock in another

If you use Section 1045, you defer tax on the reinvested amount. You do not pay tax until you eventually sell the new QSBS.

Section 1045 planning is complex and requires professional guidance.

Documentation

To claim the Section 1202 exclusion, you must prove that your stock qualifies. The IRS will not take your word for it.

Keep the following documentation:

- Articles of incorporation (showing C-corporation status)

- Bylaws

- Board resolutions authorizing stock issuance

- Stock purchase agreements or stock certificates

- Proof of payment for the stock (bank wire, check, property contribution records)

- 83(b) election filings (if applicable)

- Annual financial statements or balance sheets showing the company's asset levels

- Evidence of the company's business operations (business plan, revenue records, customer contracts)

- Evidence of when you exercise options (exercise agreements, board resolutions)

Keep these documents for at least seven years after the sale.

How the OBBBA changes section 1202

The One Big Beautiful Bill Act, signed July 4, 2025, made four major changes to Section 1202:

Change 1: Increased exclusion cap from $10M to $15M

For stock issued after July 4, 2025, the per-issuer, per-shareholder exclusion cap increased from $10 million to $15 million.

This means you can exclude up to $15 million in gain instead of $10 million (assuming you meet the holding period requirement).

This change is indexed for inflation beginning in 2027.

Change 2: Partial exclusions for short holding periods

Previously, you had to hold QSBS for at least five years to claim any exclusion.

Now, for stock issued after July 4, 2025:

- Hold for 3 years: 50% exclusion

- Hold for 4 years: 75% exclusion

- Hold for 5 years: 100% exclusion

This gives founders more flexibility if they want to exit sooner.

Change 3: Increased asset threshold from $50M to $75M

The gross asset limit for qualifying businesses increased from $50 million to $75 million for stock issued after July 4, 2025.

This allows larger, more-mature companies to still issue QSBS.

Change 4: Indexed for inflation

The $15 million exclusion cap is adjusted annually for inflation beginning in 2027.

The $75 million asset threshold is also indexed for inflation.

These changes significantly expanded the value of Section 1202 for founders. The lower holding period requirement and higher exclusion cap make it attainable for more companies.

Special considerations for foreign founders

If you are a founder who is not a US citizen or resident, Section 1202 still applies to you, but there are additional considerations.

US tax residency

To claim Section 1202, you must be a US person. A US person includes US citizens, permanent residents (green card holders), and individuals subject to US tax residency rules.

If you are a non-US citizen and non-resident, you generally are not a US person, and Section 1202 does not apply to you.

However, if you hold a valid visa that makes you a US tax resident (e.g., E-2 visa, H-1B visa), you may qualify as a US person.

Consult a tax professional before assuming you do not qualify.

Treaty implications

If you are a non-US citizen, you may be subject to tax under a US-India tax treaty (or treaty with your home country) even if you are not a US resident.

Tax treaties can affect your overall tax liability, the rate of tax, and whether certain exclusions apply.

For example, many tax treaties provide that capital gains are taxed only in the country where you reside. If you reside in India and are a non-US resident, you may not owe US tax on the gain, but you will owe Indian tax.

This is beyond the scope of a US-focused blog, but the point is: if you are a foreign founder, consult a tax professional who understands both US and your home country tax law.

How Inkle can help you manage QSBS?

QSBS qualifications depend on accurate documentation and ongoing compliance. Inkle's integrated platform directly supports QSBS planning:

1. Incorporation & stock issuance records: Inkle Incorporate handles Delaware C-Corp formation and maintains articles of incorporation, bylaws, and board resolutions. These documents prove your company's C-Corp status, the first requirement for QSBS eligibility.

2. 83(b) election filing: Inkle helps prepare and file 83(b) elections for founder shares and restricted stock. Your holding period cannot begin until your election is properly filed, making this critical for QSBS timing.

3. Financial tracking: Inkle Books tracks your company's asset composition (cash, equipment, intangible assets, passive holdings). Since Section 1202 requires 80 percent of assets in active business, Inkle's reports help you identify excess cash or passive holdings before they jeopardize QSBS status.

4. Compliance & deadline tracking: Inkle's reminders help ensure you file required annual reports and maintain good standing. A company struck from state records may permanently lose QSBS status.

5. Multi-Entity tracking: If you hold equity in multiple startups, Inkle tracks all entities in one place. This is critical because Section 1202 caps the exclusion per issuer, so you need visibility into each holding.

6. Audit trail documentation: Inkle's tax filings and financial records create documentation of your basis, holding period, and asset levels at issuance. When you sell, this audit trail enables any tax professional to calculate your Section 1202 exclusion correctly.

For founders with US C-Corporations, especially international founders with cross-border structures, Inkle's integrated approach to bookkeeping, tax filing, and compliance is invaluable for QSBS planning.

In this article

.jpg)