US Payroll vs. PEO: What Every Early-Stage Founder Gets Wrong

Choosing between running US payroll directly and onboarding your team onto a Professional Employer Organisation (PEO) is one of the most consequential operational decisions you'll make in your first year of US hiring. It's also one of the most quietly mishandled.

Founders typically arrive at this question after they've already opened a Gusto account, registered with the state EDD, and committed to a process - only to discover six months later that they're on the wrong path. The migration is messy, benefits-disruptive, and entirely avoidable.

Here's what you need to know before you open a single payroll account.

The spectrum explained

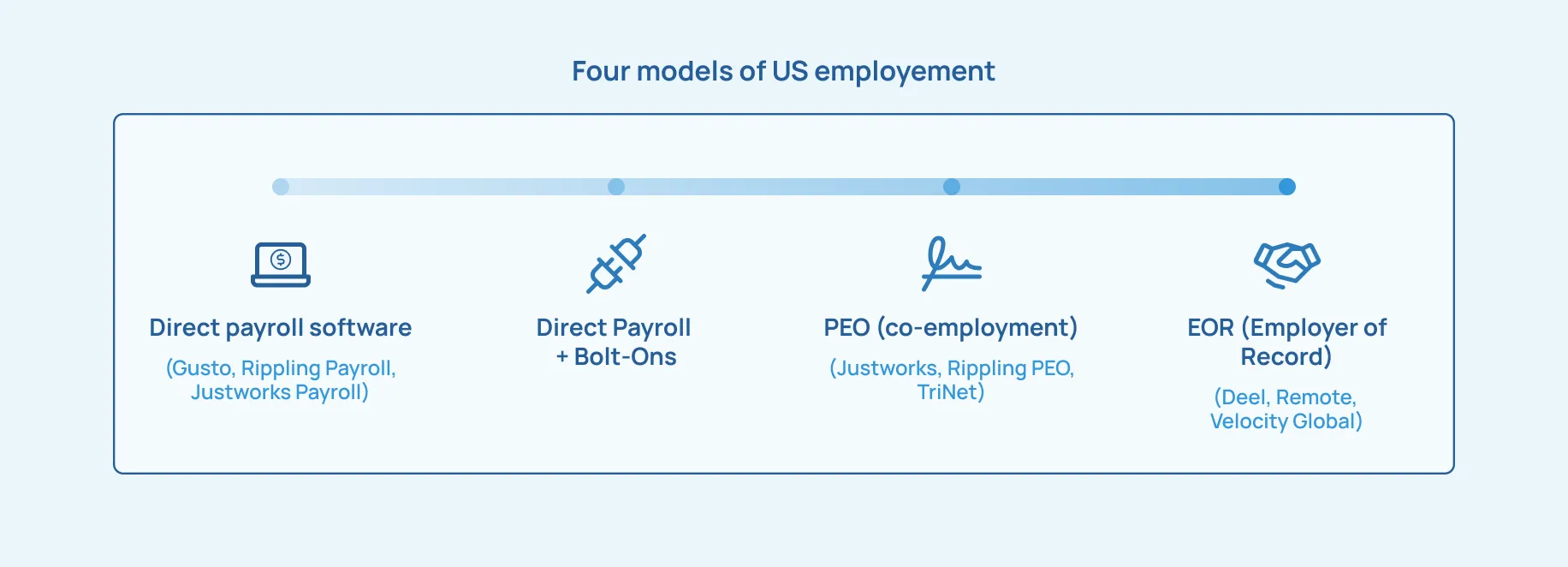

There are four distinct models for US employment, and they're not interchangeable.

Direct Payroll Software (Gusto, Rippling Payroll, Justworks Payroll) is a piece of software, not a service organisation. It runs the payroll cycle, withholds taxes, and remits to the relevant authorities. Everything else - state registrations, workers' comp, health insurance, labor-law compliance - remains your responsibility.

Direct Payroll + Bolt-Ons adds third-party modules for retirement, state compliance tracking, and similar. Several payroll vendors have acquired bolt-on companies in recent years. The integration is workable but not seamless; gaps in labor-law notices and multi-state registration tend to surface eventually.

PEO (co-employment) - Justworks, Rippling PEO, TriNet - makes the PEO a co-employer for tax and benefits purposes, while you retain full management authority. The PEO handles payroll, benefits, workers' comp, state-by-state labor law, and HR administration. This is the default for any Delaware C-Corp with two or more US employees.

EOR (Employer of Record) - Deel, Remote, Velocity Global - is for hiring in countries where you have no entity. This is not the same as a US-domestic PEO. If you're a Delaware C-Corp hiring US employees, you want a PEO, not an EOR.

What payroll software actually doesn't do

This is where most founders get caught out, especially those coming from an Indian or UK employment context where statutory employment is centralised.

Payroll software handles: pay-cycle execution, federal and state tax withholding and remittance, quarterly and annual returns (941, W-2), direct deposit, and new-hire reporting.

It does not handle:

- State employer registration. Before your first payroll runs in a new state, you must register for withholding, unemployment, and (in many states) paid family leave. The software cannot do this for you.

- Workers' compensation insurance. Required in 49 of 50 states. You must procure your own policy from a carrier. Failure to carry workers' comp creates significant employer liability.

- Health insurance. The software routes you to a broker, where you'll be rated as a one- or two-life group - the most expensive tier in the market.

- Labor-law posters and notices. California alone requires nine separate posters for any employer with a single California-based employee. For remote workers, you still have to distribute these electronically and obtain attestation. This obligation applies whether or not you know about it.

- Termination compliance. California requires same-day final pay for involuntary terminations. New York, Massachusetts, Washington, and Colorado all have their own rules. The software computes the final check; it doesn't tell you what else you're legally required to do.

- Multi-state nexus. An employee working remotely from a state where you haven't registered creates nexus in that state - for payroll tax, sometimes for income tax, sometimes for sales tax. The software doesn't warn you.

The first time most of this becomes visible is when a state agency sends a notice or a former employee files a claim. The cure is always more expensive than the prevention.

The two things a PEO actually buys you

PEO marketing lists a dozen features. In practice, two of them are genuinely decision-changing. The rest are pleasant but not the reason to switch.

1. Cheaper health insurance

A PEO purchases health insurance from major carriers - UnitedHealthcare, Aetna, Anthem, Cigna - on behalf of its entire client base. That pool is often 500,000+ covered lives. Carriers price that pool as one very large employer, which produces materially lower premiums per life than a one- or two-life group would ever see.

For a single employee, age 30, in San Francisco, on a mid-tier PPO, the rough comparison looks like this:

The PEO premium typically comes in 15–30% below what the same employee would be quoted through a payroll software's marketplace. For families and older employees, the gap widens.

There's also a tax dimension: employer contributions to group health insurance are pre-tax for both employer and employee. Individual marketplace premiums paid from after-tax salary don't have the same treatment.

2. Absorbed state-by-state administration

The second benefit is less visible at the start and more material over time.

Consider what a single California employee requires in year one: an EDD employer account, nine separate labor-law posters (distributed electronically with attestation for remote workers), IWC Wage Order compliance, Healthy Workplaces Healthy Families Act sick-leave configuration, annual harassment-prevention training, CFRA, and PDL compliance - and updates when the California legislature amends any of it (which happens nearly every session).

A PEO absorbs this work. It provides the posters, configures the sick-leave accruals, schedules the training, tracks the legislative changes, and updates your handbook. For a small company, the leverage of having this work simply done - rather than discovered, scoped, and executed in-house - is significant. It grows with every hire and every new state.

The provider landscape

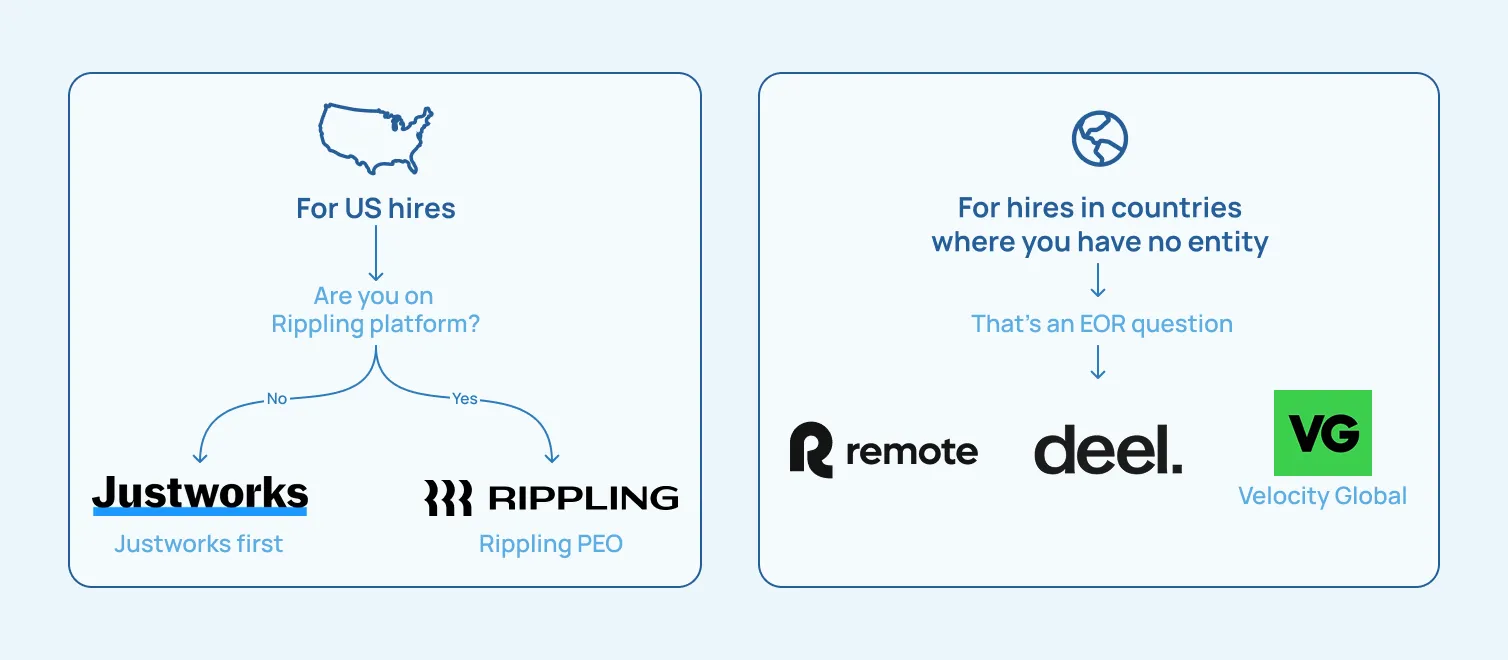

Gusto is where most founders end up first. It does the payroll-software job well: clean execution, all standard filings, usable employee portal. The 401(k) bolt-on and state-compliance tracking are workable additions. Gusto does not offer a PEO product. For one US employee with no near-term hiring plans, it's a defensible choice. For two or more, it's rarely right on its own.

Rippling offers both direct payroll and a PEO product. The principal advantage is platform integration - payroll, HRIS, IT identity, and device management running on one schema. The principal disadvantage is the switching cost: migrating off Rippling later is more involved than migrating off Gusto, because more of your operational state lives inside the platform.

Justworks is primarily a PEO, and the one most commonly used by early-stage Delaware C-Corps. The product is focused, the onboarding is straightforward, the pricing is transparent, the health plans are competitive, and the HR support is reliable. For a Delaware C-Corp with two or more US employees - or one employee with meaningful health-coverage needs - Justworks PEO is the default to explore first.

The all-in cost

Founders sometimes refuse the PEO conversation on the assumption that the $80–$150 per-employee PEO fee is an additional cost on top of direct payroll. It isn't. The PEO fee includes payroll execution, workers' compensation, HR advisory, compliance tracking, and benefits administration. Once you add health insurance, the PEO is typically cheaper all-in.

Single employee, $120K base, San Francisco, employer pays 100% of single-employee health premium:

At three employees, that gap widens to over $10,000 per year. The PEO only costs more than direct payroll when you're offering no employer-paid health insurance - which is a defensible setup for a one-person company, and rarely sustainable at five.

The four questions to answer before choosing anything

The pattern that leads to bad setups is choosing a payroll software before answering these questions. Ask them first.

1. How many US employees will you have today, and in 12 months? One today and likely one in 12 months - direct payroll is defensible. One today and two or more in 12 months - start on a PEO now. Migrating mid-year is operationally messy and benefits-disruptive.

2. Will you offer employer-sponsored health insurance? If yes at any level, the PEO's group-rate leverage is material from day one. If not, the case for PEO weakens - but the administrative absorption argument remains.

3. In how many US states will employees be located? Single state, low complexity - direct payroll can work. Multi-state from day one, or California specifically - the PEO's standing 50-state registration eliminates a meaningful and growing burden.

4. Does anyone at the company have an appetite to own US labor-law administration? If yes - direct payroll with bolt-ons can be made to work. If your time is better spent building the product - PEO is the better default. Most early-stage founders fall into the second camp.

Common mistakes and how to avoid them

Assuming payroll software is a managed service. It isn't. It's a piece of software - closer in spirit to QuickBooks than to an outsourced HR function. Everything outside the payroll cycle is yours to manage.

Conflating bolt-ons with PEO coverage. Bolt-ons help you see the compliance landscape. A PEO absorbs the work. They're not the same. The first lights up obligations; the second removes them from your plate.

Confusing PEO with EOR. PEO is for US-domestic employees of a US-incorporated client. EOR is for employees in countries where you have no entity. Don't use an EOR for US hires at a Delaware C-Corp - it creates unnecessary cost and structural awkwardness.

Underestimating the cost of leaving a PEO later. PEOs are easy to join and meaningfully harder to leave. Exiting requires registering in every state where you have employees, procuring your own workers' comp, securing your own health insurance (and losing the group-rate leverage), and setting up your own 401(k). Plan for the exit when it becomes economic - typically at 50–100 US employees - and don't rush it.

Opening a payroll account before asking why. The trigger is usually a hire arriving in the US. The reflex is to get an EIN, register with the state EDD, and open a Gusto account. None of those steps is wrong; the omission is the ten-minute conversation that should precede them - about expected headcount, benefits, state distribution, and what you're actually trying to build.

The recommendation

For the typical early-stage Delaware C-Corp - often with foreign founders, hiring the first one to ten US employees alongside a larger team in India or the UK - the recommendation is straightforward.

Direct payroll is acceptable if: you will have one US employee for the foreseeable future, they don't need employer-sponsored health insurance, the work is in a single state, and you have bandwidth to own the administrative load. Re-evaluate at each new hire.

PEO is the better default if: any of those conditions doesn't hold - two or more US employees, employer-sponsored health insurance in scope, employees across multiple states, or your time is better spent on the product than on labor-law posters.

The single most useful thing you can do before making this decision is answer the four questions above, explicitly, before opening any account. It takes ten minutes and prevents the most expensive class of avoidable rework.

In this article

.webp)