What is Form BE-10 and who is required to file it?

If you're a US business owner with operations or investments outside the United States, you might receive a notice from the Bureau of Economic Analysis (BEA) asking you to file Form BE-10. You might ignore it. You might wonder if it actually applies to you. You might hope it goes away. It won't.

Form BE-10 is one of the most important yet misunderstood filing requirements for US companies with foreign operations. Failure to file can result in civil penalties up to $25,000, and willful failure can trigger criminal prosecution, fines, and imprisonment.

This guide explains what Form BE-10 is, who must file it, what information you need, and what happens if you don't.

What is Form BE-10?

Form BE-10 is the Benchmark Survey of U.S. Direct Investment Abroad, administered by the Bureau of Economic Analysis (BEA), which is part of the U.S. Department of Commerce.

The form collects comprehensive financial and operating data on US multinational enterprises and their foreign subsidiaries. The data is used to measure US foreign direct investment, track the global operations of American companies, and inform US economic policy and trade negotiations.

The survey is mandatory. It is conducted every five years and covers fiscal years ending in that benchmark year. The most recent survey covered fiscal year 2024 and was due May 30 or June 30, 2025, depending on the number of foreign affiliates being reported.

The form is authorized under the International Investment and Trade in Services Survey Act (22 U.S.C. 3101-3108), which means participation is required by federal law.

Who must file Form BE-10?

You must file Form BE-10 if you meet one simple criterion: you are a US person who owns or controls 10 percent or more of a foreign business enterprise at any time during your fiscal year.

Let's unpack what this means.

US Person

A "US person" includes:

- US citizens

- US corporations

- US partnerships

- US trusts

- US estates

- Any other business entity organized in the United States or formed under US law

It also includes foreign trusts or estates with a US beneficiary (though these have specific rules about who files on their behalf).

Non-US citizens residing in the United States on a visa do not automatically qualify as US persons for this purpose. The BEA uses specific legal tests to determine residency status for filing purposes.

Foreign affiliate

A "foreign affiliate" is a foreign business enterprise in which a US person owns or controls 10 percent or more of the voting stock (if incorporated) or an equivalent interest (if unincorporated).

This includes corporations, partnerships, branches, and limited liability companies organized outside the United States.

It also includes ownership of foreign real estate in certain circumstances. If you own rental property abroad, farm land, or any other real estate held as a business operation (not purely for personal use), it may be reportable as a foreign affiliate.

The 10% threshold

The 10 percent threshold applies to direct or indirect ownership. This means:

- Direct ownership: You own 10 percent or more of the foreign company directly

- Indirect ownership: You own shares through another US company, and your combined ownership stake reaches 10 percent or more

Example: You own a US company that owns 6 percent of a French manufacturing firm. Your spouse also owns 5 percent of the same French firm directly. Your combined indirect ownership is 11 percent, which meets the reporting threshold.

Who doesn't have to file?

Certain entities are exempt or have modified requirements:

Private funds that do not own an operating company may be exempt. A private fund is defined as an investment entity (like a venture capital fund or hedge fund) that was not a US corporation or partnership at the time of formation.

Ownership of foreign residential real estate held exclusively for personal use and not for profit-making purposes is not reportable. This applies only to your vacation home, primary residence, or other personal property. Any commercial or income-producing use of the property triggers the reporting requirement.

Certain branches of US persons conducting foreign operations as an unincorporated enterprise may have modified requirements.

Which form should you file?

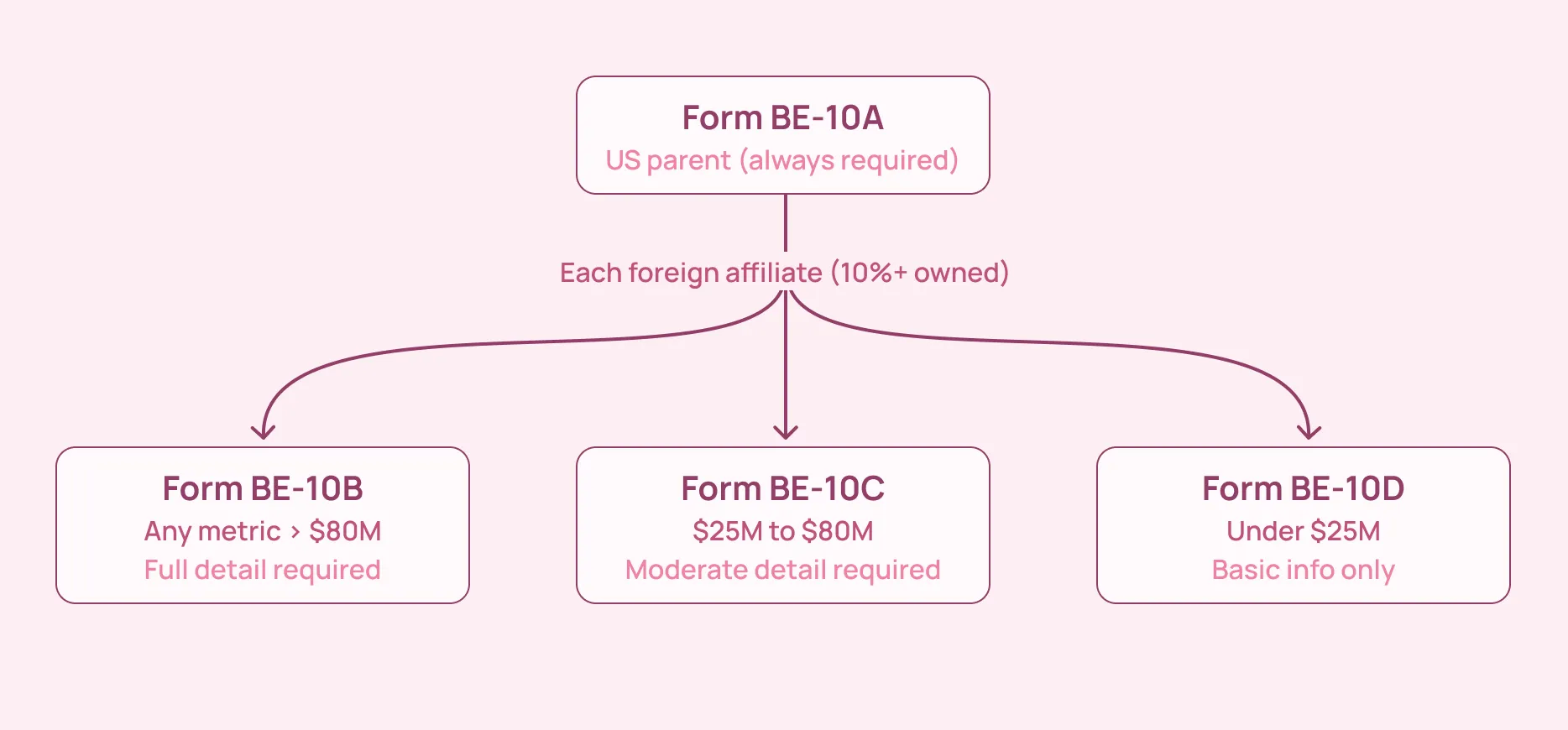

Form BE-10 is not a single form. It is a suite of forms, each with different levels of detail based on the size of the foreign affiliate.

Every US reporter must file a Form BE-10A, which reports data on the fully consolidated US domestic business enterprise.

In addition, you must file one or more supplemental forms for each foreign affiliate:

Form BE-10B

File Form BE-10B for majority-owned foreign affiliates (more than 50 percent ownership) whose total assets, annual sales, or net income exceed $80 million.

This form requires detailed financial and operating information, including balance sheet data, income statement data, employment information, R&D activities, and capital expenditures.

Form BE-10C

File Form BE-10C for majority-owned foreign affiliates whose total assets, annual sales, or net income exceed $25 million but none of these items exceed $80 million.

Form BE-10C requires less detail than BE-10B but still captures key financial information.

File Form BE-10C also for minority-owned foreign affiliates (10 percent to 50 percent ownership) whose total assets, annual sales, or net income exceed $25 million.

Form BE-10D

File Form BE-10D for all foreign affiliates whose total assets, annual sales, and net income do not exceed $25 million.

This is the simplest form, requiring basic financial data and ownership information.

Determining which form to file

The form you file depends on the size of each foreign affiliate. You measure size using total assets, total sales (gross operating revenue, excluding sales taxes), or net income after foreign taxes. If any of these three metrics exceeds the threshold, you file the corresponding form.

Example: Your foreign subsidiary has total assets of $60 million, annual sales of $150 million, and net income of $12 million. Because one metric (annual sales) exceeds the $80 million threshold, you file Form BE-10B for that affiliate, even though the other metrics are lower.

You may consolidate multiple foreign affiliates into a single form if they are in the same detailed industry classification or are integral parts of the same business operation. Otherwise, each foreign affiliate requires a separate form.

When is form BE-10 due?

The 2024 benchmark survey is due on the following dates:

May 30, 2025 for US reporters required to file fewer than 50 Forms BE-10B, BE-10C, and/or BE-10D.

June 30, 2025 for US reporters required to file 50 or more Forms BE-10B, BE-10C, and/or BE-10D.

The BEA determines the deadline based on how many affiliate forms you need to file, not on whether you received a notice.

You may request an extension, but the request must be filed by the original due date. Extensions are typically granted for 60 to 90 days if reasonable cause is shown.

What information must you report?

The information required varies by form, but generally includes:

Form BE-10A (US Domestic Business Enterprise)

- Corporate structure and ownership information

- Total assets, sales, and net income

- Employment data

- Capital expenditures

- Breakdown of US operations by state

Forms BE-10B, BE-10C, and BE-10D (Foreign Affiliates)

- Ownership structure (direct ownership percentages and names of owners)

- Balance sheet data (assets, liabilities, equity)

- Income statement data (sales, operating income, net income)

- Employment information

- Compensation and benefits paid to employees

- R&D activities and funding

- Capital expenditures

- Industry classification

- Country or region of operations

The level of detail increases with the size of the affiliate. BE-10B requires the most comprehensive data, while BE-10D requires only basic financial information.

All amounts are reported in US dollars, rounded to thousands.

How do you file Form BE-10?

You have three options:

- Electronic filing

Use the BEA's eFile system at www.bea.gov/efile. This is the preferred method and allows you to submit, save progress, and revise your filing before final submission. Electronic filing is available to all reporters, regardless of the number of forms you are filing.

Mail completed forms to: Bureau of Economic Analysis Direct Investment Division, BE-69(A) 4600 Silver Hill Road Washington, DC 20233

Include a cover letter identifying your company and listing the forms being submitted.

- Fax

Fax completed forms: Include a cover sheet with your company name, the forms being submitted, and contact information.

Before you file

You will need your BEA reporter ID, which is assigned when you are initially identified by the BEA as having a filing requirement. If this is your first filing, contact the BEA to request your ID.

Prepare all financial data for your US domestic business and each foreign affiliate for the entire fiscal year. If any affiliates have multiple currencies, convert all amounts to US dollars using the average exchange rate for the reporting period.

Have your federal Employer Identification Number (EIN) available.

You must certify that the information you report is true and accurate. This certification is made "under penalties of perjury," which means false or misleading information can result in criminal charges under 26 U.S.C. 7206.

Penalties for failure to file

Penalties for not filing Form BE-10 are serious and enforcement is active.

Civil penalties

Any US person who fails to file a required Form BE-10 report is subject to civil penalties of not less than $2,500 and not more than $25,000 per violation, according to 31 CFR 128.4.

A "violation" typically means one failure to file the required report within the time limit, not each form within the report.

However, if you file an incomplete or inaccurate report, each material error or omission can be treated as a separate violation.

Willful failure penalties

If the BEA determines that your failure to file was willful (meaning intentional or with reckless disregard for the filing requirement), you face criminal prosecution under 22 U.S.C. 3105.

Criminal penalties for willful failure include:

- Fines up to $10,000

- Imprisonment for up to one year

- Both fines and imprisonment may be imposed

This applies to any individual, including officers, directors, employees, or agents of any corporation, who knowingly participates in a willful violation.

Enforcement

The BEA actively enforces the filing requirement. If you fail to file:

- You will receive a notice from the BEA requesting a response

- If you do not respond or file within 30 days, you will receive a penalty notice

- The BEA may refer serious violations to the Department of Justice for criminal prosecution

The BEA has resources to pursue collection, and penalties can significantly exceed the cost of filing the form properly in the first place.

Special scenarios

Foreign affiliates in multiple countries

If you own foreign affiliates in several countries, you must file a separate form for each affiliate (or consolidate if they meet specific criteria) regardless of where they are located.

Different countries have different tax rates, financial reporting standards, and currency. The BEA wants to capture this data separately so it can analyze US investment patterns by country.

Minority ownership

If you own less than 50 percent of a foreign affiliate, you still have a reporting requirement if your ownership stake is 10 percent or more.

You typically file Form BE-10C for minority-owned affiliates with material assets, sales, or income above $25 million.

When you acquire or dispose of foreign affiliates

If you acquire a new foreign affiliate during your fiscal year, you must report it on your BE-10 for the year in which you acquired it, even if you acquired it on the last day of your fiscal year.

If you sell or dispose of a foreign affiliate during your fiscal year, you still report it on the BE-10 for that year, using financial data for the period of your ownership.

Recent changes to Form BE-10

In 2024, the BEA expanded the information collected on Form BE-10 regarding research and development activities performed by US parents for foreign affiliates under collaborative R&D agreements.

Previously, the form did not ask specifically about this. Now, reporters must identify the value of R&D performed by the US parent for each foreign affiliate under a collaborative arrangement.

This change reflects growing interest in understanding US research investment that benefits foreign operations.

What happens if you miss the deadline?

If you miss the filing deadline:

- Contact the BEA immediately to request an extension. Extensions can sometimes be granted if you demonstrate reasonable cause.

- If you cannot obtain an extension, file as soon as possible and include a brief explanation of the delay.

- If you receive a penalty notice, you can request abatement (removal or reduction) if you can demonstrate reasonable cause for the late filing. Reasonable cause typically means you exercised ordinary care and prudence but something unexpected prevented timely filing.

- Do not ignore penalty notices from the BEA. Ignoring them does not make them go away. Penalties will continue to accrue.

Next steps if you have a filing requirement

- Confirm your filing requirement by checking with a tax advisor familiar with international reporting requirements.

- Gather financial data for your US business and each foreign affiliate for your fiscal year.

- Determine which forms you must file based on the size of each foreign affiliate.

- Register for an eFile account at www.bea.gov/efile if you do not already have one.

- Complete the forms with accurate financial and ownership information.

- Submit by the deadline. If you cannot submit by the deadline, request an extension immediately.

- Keep copies of your filed forms and supporting documentation for your records.

If you have questions about your specific situation, consult a tax advisor with experience in international direct investment reporting.

In this article

.jpg)