GILTI Tax Explained: What Every India-US Startup Founder Needs to Know

Most Indian founders who incorporated a Delaware C-Corp with an Indian subsidiary figured out pretty quickly that they have to file Form 5471 every year. They know about transfer pricing. They know about FEMA reporting on the Indian side.

What catches most of them off guard is GILTI.

GILTI stands for Global Intangible Low-Taxed Income. It is a US tax on the foreign earnings of a US-owned company, imposed annually on the US parent, even if the Indian subsidiary never distributes a single rupee to the parent company. If your Delaware C-Corp owns more than 50% of your Indian subsidiary, the profits your Indian entity earns are partially taxable in the US in the same year they are earned.

This is not a future obligation. It is not triggered by distributions. It applies every year your Indian entity is profitable, regardless of what you do with the money.

Here is what every India-US founder needs to understand about GILTI, how it is calculated, what the One Big Beautiful Bill Act changed for 2026, and how India's corporate tax rate affects whether you actually owe anything to the IRS.

What is GILTI and why does it exist?

GILTI was introduced by the Tax Cuts and Jobs Act of 2017 under Section 951A of the Internal Revenue Code. Congress created it to prevent a specific tax avoidance strategy: large US multinationals were parking their intellectual property in low-tax or zero-tax foreign jurisdictions, allowing income from those assets to accumulate offshore without paying US tax. GILTI was designed to close that loophole by imposing a minimum tax on the foreign earnings of US-owned foreign corporations, regardless of where those earnings are kept.

The name reflects the original intent. Income from intangible assets like software, brand value, and technology was earning very little foreign tax. GILTI put a floor under it.

In practice, GILTI ended up applying far more broadly than just to IP-heavy multinationals. Any US person who owns 10% or more of a controlled foreign corporation is subject to GILTI on that CFC's profits. This includes a Delaware C-Corp owning an Indian software development subsidiary, a services company, or a consulting operation.

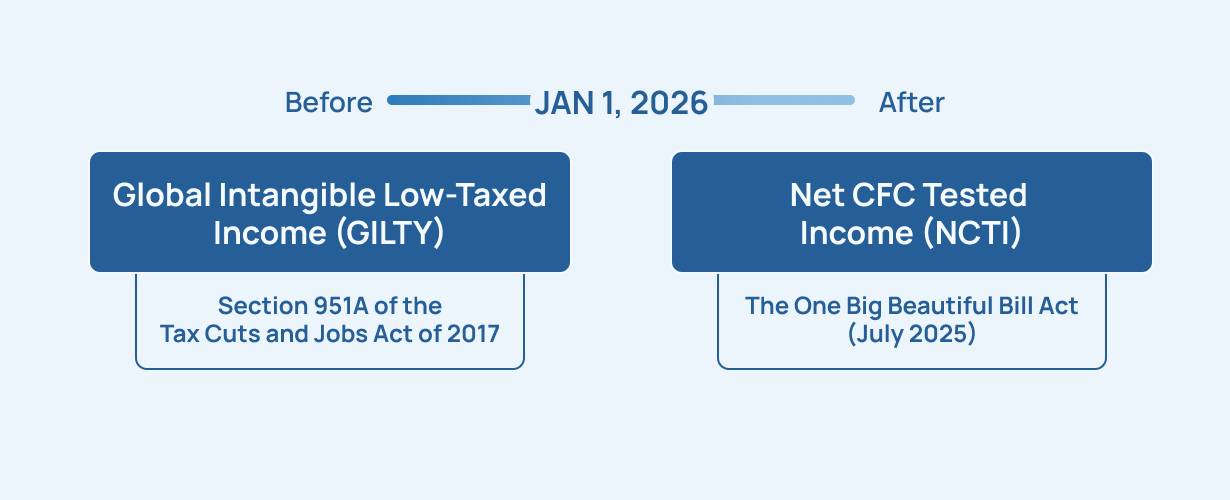

Starting January 1, 2026, GILTI was officially renamed Net CFC Tested Income (NCTI) under the OBBBA, and several of its mechanics changed. This guide covers both the 2025 rules and the 2026 rules, since most founders reading this will be dealing with one or the other depending on their tax year.

Does GILTI apply to your India-US startup?

GILTI applies when three conditions are met simultaneously.

Your US entity is a US shareholder. A US shareholder is any US person, including a US corporation, that owns 10% or more of the total combined voting power or value of a foreign corporation. Your Delaware C-Corp, as the 100% owner of your Indian subsidiary, is a US shareholder. This condition is met.

The foreign entity is a Controlled Foreign Corporation. A CFC is a foreign corporation in which US shareholders together own more than 50% of the total vote or value. If your Delaware C-Corp owns the Indian entity, US shareholders own 100%. The Indian subsidiary is a CFC. This condition is met.

The CFC has tested income. Tested income is the CFC's gross income less allowable deductions, after removing certain excluded categories. Excluded categories include income already taxed under Subpart F, income effectively connected with a US trade or business, and income covered by the high-tax exception, explained later in this guide. If your Indian subsidiary is a profitable software or services business, it almost certainly has tested income.

All three conditions apply to a standard India-US startup structure. GILTI applies to you.

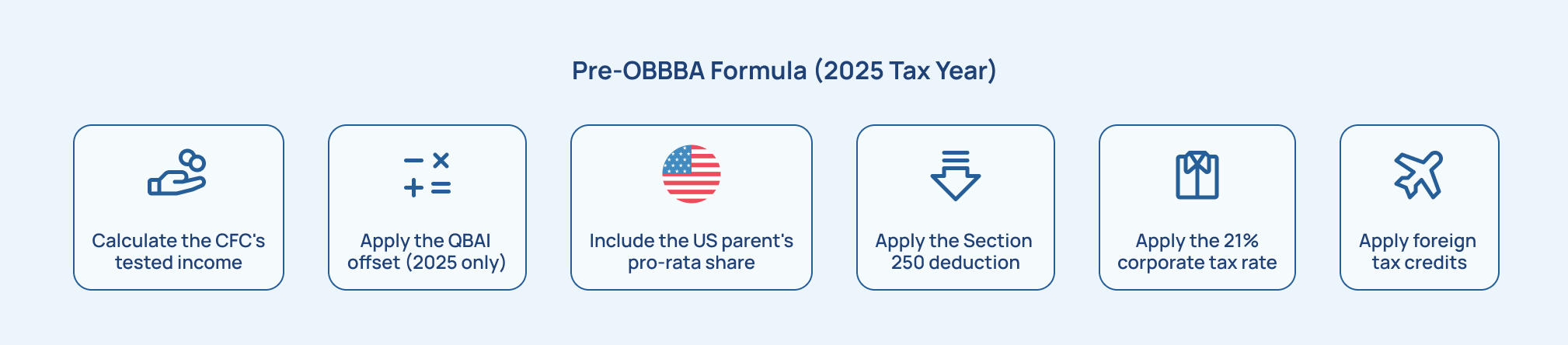

How GILTI is calculated: 2025 Rules

For the 2025 tax year, the pre-OBBBA formula applies.

Calculate the CFC's tested income. Start with the Indian entity's gross income. Remove Subpart F income, income effectively connected with a US trade or business, and income covered by the high-tax exception. What remains is gross tested income. Subtract allowable deductions to get net tested income.

Apply the QBAI offset (2025 only). Under the 2025 rules, the US parent can subtract 10% of the CFC's Qualified Business Asset Investment (QBAI), which is the net book value of tangible depreciable assets used in the business. For a software or services company with few physical assets, QBAI is typically small, meaning almost all tested income remains in the GILTI base.

The 2025 GILTI formula is: GILTI = Net CFC tested income minus (10% multiplied by QBAI minus interest expense)

For a services-focused Indian entity with $500,000 in profit and $50,000 in tangible assets, the QBAI offset is $5,000. GILTI is approximately $495,000.

Include the US parent's pro-rata share. The Delaware C-Corp includes its proportional share of the GILTI in gross income on Form 1120. As the 100% owner, it includes 100%.

Apply the Section 250 deduction. A US C-Corp can deduct 50% of the GILTI inclusion for the 2025 tax year. On $495,000 of GILTI, the deduction is $247,500. The taxable GILTI is $247,500.

Apply the 21% corporate tax rate. At 21%, the tax on $247,500 is $51,975. This is the tentative GILTI tax before foreign tax credits.

Apply foreign tax credits. The Delaware C-Corp can credit 80% of the Indian taxes paid on the tested income. India's corporate tax rate of 22% (concessional) or approximately 25.17% (all-in with surcharge and cess) exceeds the 2025 crossover rate of 13.125%, meaning the Indian tax credit is generally sufficient to eliminate the residual US GILTI tax for founders whose Indian entity pays standard Indian corporate tax.

This means most Indian startups with a standard Indian corporate tax rate do not end up paying additional US tax on GILTI in 2025. But this is a calculation that needs to be done every year, and the numbers change in 2026.

GILTI in 2026

The One Big Beautiful Bill Act, signed on July 4, 2025, made the most significant changes to GILTI since its 2017 introduction. For tax years beginning after December 31, 2025, three core mechanics changed.

The QBAI exclusion is eliminated. Under the 2025 rules, a 10% return on tangible assets was excluded from the GILTI base. Starting in 2026, this exclusion no longer exists. All of a CFC's net tested income is included in the NCTI base regardless of tangible asset investment. For service-heavy Indian subsidiaries with little QBAI, the practical impact is minimal. For Indian entities with significant physical assets, the taxable base increases.

The Section 250 deduction drops from 50% to 40%. For 2025, the C-Corp could deduct 50% of GILTI, producing an effective rate of 10.5%. For 2026, the deduction is permanently set at 40%, raising the effective rate to 12.6% (21% multiplied by 60%). The OBBBA made this rate permanent with no further phase-downs, which provides planning certainty compared to the scheduled deterioration under the original TCJA schedule.

The foreign tax credit cap increases from 80% to 90%. Under the 2025 rules, only 80% of foreign taxes paid were creditable against GILTI. Under the 2026 rules, 90% are creditable, partially offsetting the impact of the reduced Section 250 deduction.

The crossover rate changes from 13.125% to approximately 14%. The crossover rate is the foreign effective tax rate at which no residual US tax is owed after applying the Section 250 deduction and available foreign tax credits. India's corporate rates of approximately 22% to 25.17% exceed the new 14% crossover rate. Indian startups operating under standard Indian corporate tax continue to see their Indian tax credits largely offset US NCTI tax, but this must be verified each year.

India's corporate tax rate and the high-tax exception

India's domestic corporate tax structure matters directly for GILTI and NCTI planning.

Indian companies that opted for the concessional tax regime under Section 115BAA of the Income Tax Act pay 22% base corporate tax. With a 10% surcharge and 4% health and education cess, the effective all-in rate is approximately 25.17%. Companies that did not exercise the concessional option pay 30% base rate with applicable surcharge and cess. The Finance Act 2026 reduced the Minimum Alternate Tax rate from 15% to 14% for companies under the existing tax regime.

Under the GILTI and NCTI rules, if a CFC's income is subject to a foreign effective tax rate of at least 18.9% (which is 90% of the US corporate rate of 21%), that income can be excluded from the GILTI or NCTI calculation entirely under the high-tax exception. This election must be made annually.

An Indian subsidiary paying the concessional rate of approximately 25.17% effective exceeds the 18.9% threshold. This means that for many India-US startups, the high-tax exception election can eliminate the NCTI inclusion entirely, rather than relying on the foreign tax credit mechanism to offset it.

The high-tax exception and the foreign tax credit approach are alternative strategies with different trade-offs. The high-tax exception completely removes the income from the US tax calculation but means the associated foreign tax credits are not usable against other income. The foreign tax credit approach includes the income in the NCTI base but offsets the US tax with credits. The right choice depends on the specific numbers, the founder's individual tax situation, and whether the Indian entity has years with lower effective rates due to tax holidays or deductions available under Indian law.

Individual founders vs. C-Corp shareholders

The analysis above applies to Delaware C-Corps with Indian subsidiaries. If you personally own shares in the Indian entity rather than through a US corporation, the tax treatment is significantly worse without planning.

An individual US person who owns 10% or more of a CFC includes GILTI in gross income at ordinary income tax rates, which can reach 37%. An individual cannot claim the Section 250 deduction and cannot use indirect foreign tax credits to offset GILTI. The result is potential double taxation on the same profits: once in India and again in the US at full individual rates.

The Section 962 election addresses this. Under Section 962, an individual US shareholder can elect to be taxed on GILTI as if they were a US C-Corp. This allows the individual to access the 40% Section 250 deduction and claim 90% of foreign taxes as an indirect credit under the 2026 rules. Making the Section 962 election can significantly reduce or eliminate the individual's US tax on GILTI from an Indian subsidiary.

The trade-off is that future distributions from the Indian entity may be taxed again when received, and the interaction between Section 962 and future dividend distributions requires careful modeling. The election is made annually on the individual's federal tax return and must include a written statement identifying the CFC and the income being covered.

For most India-US founders who hold equity personally rather than through a Delaware C-Corp, the Section 962 election is worth evaluating every year.

What forms do you need to file for GILTI?

GILTI compliance requires several forms filed together with the annual tax return.

- Form 5471 is the information return for US persons with interests in foreign corporations. A Delaware C-Corp that directly owns 100% of an Indian subsidiary is typically both a Category 4 filer (US person who controlled the CFC) and a Category 5a filer (US shareholder of the CFC). Both categories require Form 5471 to be filed. When a filer qualifies as both Category 4 and Category 5a, Category 4 takes precedence on the form's checkbox, but all schedules required by both categories must be completed. This form is filed with the corporate return (Form 1120) or individual return (Form 1040). The penalty for failure to file Form 5471 is $10,000 per form per year, increasing with continued non-compliance.

- Form 8992 is the GILTI calculation form. It calculates each CFC's tested income, aggregates results, and determines the US shareholder's GILTI inclusion amount. This form is filed with the annual return.

- Form 8993 is the Section 250 deduction claim form for C-Corps and for individuals making a Section 962 election. It calculates the available deduction against the GILTI inclusion.

- Form 1118 is the foreign tax credit form for corporations. It calculates the creditable Indian taxes against the GILTI or NCTI tax liability.

All forms are due with the annual return, including any extensions. Missing Form 5471 generates penalties regardless of whether any GILTI tax is ultimately owed.

A practical example: India-US startup with a profitable Indian subsidiary (2026 Rules)

Assume an India-US startup has a Delaware C-Corp parent that owns 100% of an Indian private limited company. The Indian entity had net profit of $500,000 for the 2026 calendar year. It paid Indian corporate tax at an effective rate of approximately 25%.

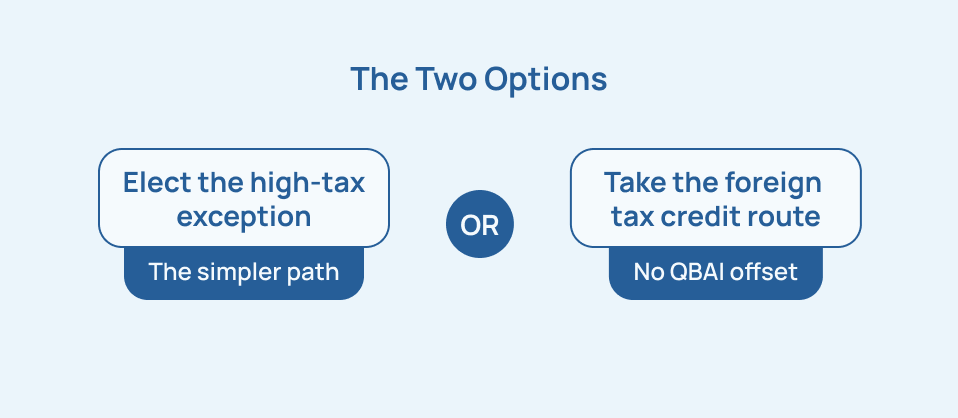

Because the Indian entity's effective tax rate (25%) exceeds the 18.9% high-tax exception threshold, the founders have two options.

Option 1: Elect the high-tax exception. The $500,000 is excluded from NCTI entirely. The Delaware C-Corp has no US NCTI inclusion for this year. No NCTI tax is owed. This is the simpler path.

Option 2: Take the foreign tax credit route. Under the 2026 rules, there is no QBAI offset. The full $500,000 is tested income.

Apply the Section 250 deduction at 40%: $500,000 multiplied by 40% equals $200,000 deducted. Taxable NCTI is $300,000.

Calculate tentative US tax at 21%: $300,000 multiplied by 21% equals $63,000.

Apply foreign tax credits at 90% of eligible Indian taxes: Indian tax paid at 25% on $500,000 is $125,000. Creditable amount is 90%, which is $112,500. This exceeds the $63,000 US tentative tax entirely, eliminating the residual US NCTI tax.

In both scenarios, no residual US NCTI tax is owed in this example. But the high-tax exception election must be formally made on the return. The foreign tax credit route requires Form 8992, Form 8993, and Form 1118 to be completed and filed.

For Indian entities paying lower effective rates due to tax holidays, R&D deductions, or startup exemptions under Indian law, the 18.9% threshold may not be met and the high-tax exception would not be available. In those cases, the NCTI inclusion must be calculated and foreign tax credits evaluated carefully.

Common GILTI mistakes India-US founders make

- Not filing Form 8992 at all is the most common error. Some founders and accountants treat Form 5471 as the full extent of CFC reporting and do not calculate or report GILTI separately. GILTI is a distinct annual obligation requiring its own form even when no US tax is ultimately owed.

- Assuming no GILTI tax means no filing requirement is the second most common mistake. Even when India's corporate tax rate is sufficient to eliminate any US GILTI liability, the forms must still be filed. Failure to file Form 8992 is a compliance violation regardless of the tax outcome.

- Not making the Section 962 election when founders hold shares individually is a structuring issue. Indian founders who personally own shares in the Indian entity without a US corporate intermediary face the full individual ordinary income rate on GILTI without the Section 250 deduction. This should be identified before the return is prepared, not during it.

- Not checking whether the high-tax exception applies every year is another missed opportunity. The high-tax exception must be elected annually. Founders whose Indian entity qualifies often do not make the election because they did not know it existed.

- Applying 2025 rates to 2026 filings produces incorrect calculations. The OBBBA changed the QBAI mechanics, the Section 250 deduction rate, and the FTC cap. These are not interchangeable across tax years.

If your Delaware C-Corp has an Indian subsidiary and you are not sure whether GILTI is being calculated and reported correctly on your annual return, book a demo with Inkle.

Frequently Asked Questions

Does GILTI apply to every Indian subsidiary owned by a Delaware C-Corp?

It applies whenever the Delaware C-Corp is a US shareholder (10% or more ownership) of a CFC (a foreign corporation where US shareholders own more than 50%), and the CFC has tested income. For a typical India-US startup where the Delaware C-Corp is the 100% parent of the Indian entity, all three conditions are met. Whether any US tax is actually owed depends on the Indian entity's effective tax rate and whether the high-tax exception applies or foreign tax credits are sufficient to offset the inclusion. The filing obligation exists regardless.

My Indian subsidiary pays about 25% corporate tax. Does that mean I do not owe GILTI in 2026?

Most likely correct, but it requires a formal annual calculation. Under the 2026 NCTI rules, the high-tax exception allows you to exclude income taxed above 18.9% from the NCTI calculation entirely. India's standard and concessional corporate tax rates both exceed 18.9%, so the high-tax exception election is generally available. Alternatively, India's 25% effective rate exceeds the 2026 crossover rate of approximately 14%, meaning creditable Indian taxes would likely eliminate any US residual tax through the foreign tax credit route. The election must be formally made on the return and the calculation must be filed. Not filing because you assume the liability is zero is a compliance failure.

What changed about GILTI in 2026 under the OBBBA?

Three things changed for tax years beginning after December 31, 2025. First, GILTI was renamed Net CFC Tested Income (NCTI), though the underlying IRC Section 951A still governs it. Second, the 10% QBAI exclusion was eliminated, meaning all CFC tested income is included without any deduction for returns on tangible assets. Third, the Section 250 deduction was permanently reduced from 50% to 40%, raising the effective corporate rate from 10.5% to 12.6%. Partially offsetting this, the foreign tax credit cap increased from 80% to 90%, and the crossover rate moved from 13.125% to approximately 14%. India's corporate rates exceed the new crossover rate, so the practical impact for most Indian subsidiaries is limited, but all calculations must reflect the 2026 rules.

Does GILTI apply to me personally if I own shares in an Indian company without a US corporate structure?

Yes. If you are a US person who owns 10% or more of an Indian company that qualifies as a CFC, GILTI applies to you personally at your ordinary income tax rate (up to 37%), with no Section 250 deduction and no access to indirect foreign tax credits. The Section 962 election addresses this by allowing you to elect corporate-rate treatment, giving you access to the 40% Section 250 deduction and 90% foreign tax credit under the 2026 rules. Whether to make the Section 962 election depends on your specific facts, particularly the Indian entity's tax rate and whether you plan to take distributions in the same year. This election should be evaluated annually with your tax advisor.

In this article

.jpg)