Form 7004 vs Form 4868: Business Extension vs Personal Extension Explained

Every year, founders and business owners scramble toward the same deadlines with the same question: which extension form do I actually need?

The IRS offers two separate automatic extension forms for income tax returns. Form 7004 is for business returns. Form 4868 is for individual returns. They cover completely different return types, have different deadlines, and filing the wrong one does not protect you. If you file Form 7004 when you need Form 4868, the IRS treats your personal return as late from the original due date.

This guide explains exactly which form applies to your situation, what each one covers, the 2026 deadlines for every major entity type, and the most common mistakes founders make when using either form.

The core difference in one sentence

Form 7004 extends the deadline to file a business tax return. Form 4868 extends the deadline to file an individual income tax return. Neither form extends your deadline to pay any tax that is owed.

That last point is the most important and most misunderstood part of any tax extension. An extension only gives you more time to file the paperwork. The tax itself is still due on the original deadline, and interest starts accruing the day after that deadline passes on any unpaid balance.

What is Form 7004?

Form 7004, officially titled "Application for Automatic Extension of Time to File Certain Business Income Tax, Information, and Other Returns," is the IRS form businesses use to request more time to file their federal business tax returns.

Filing Form 7004 correctly and on time gives your business an automatic extension. No IRS approval is required. No explanation is required. The IRS will only contact you if your extension request is denied. In practice, a correctly filed Form 7004 is almost always accepted without any response from the IRS.

Form 7004 covers 33 different business and information returns. The most common ones for startups and small businesses are:

Form 1120 (C-Corporation income tax return), Form 1120-S (S-Corporation income tax return), Form 1065 (Partnership return, including multi-member LLCs taxed as partnerships), Form 1041 (Estates and trusts), and Form 1042 (Annual withholding tax return for US source income of foreign persons).

What is Form 4868?

Form 4868, officially titled "Application for Automatic Extension of Time to File U.S. Individual Income Tax Return," is the IRS form individual taxpayers use to request more time to file their personal federal income tax return.

Like Form 7004, it is automatic. No explanation is required and no IRS approval is needed. Filing it correctly by the original due date secures the extension.

Form 4868 covers individual income tax returns including Form 1040, Form 1040-SR (for seniors), Form 1040-NR (for non-resident aliens), and Form 1040-SS.

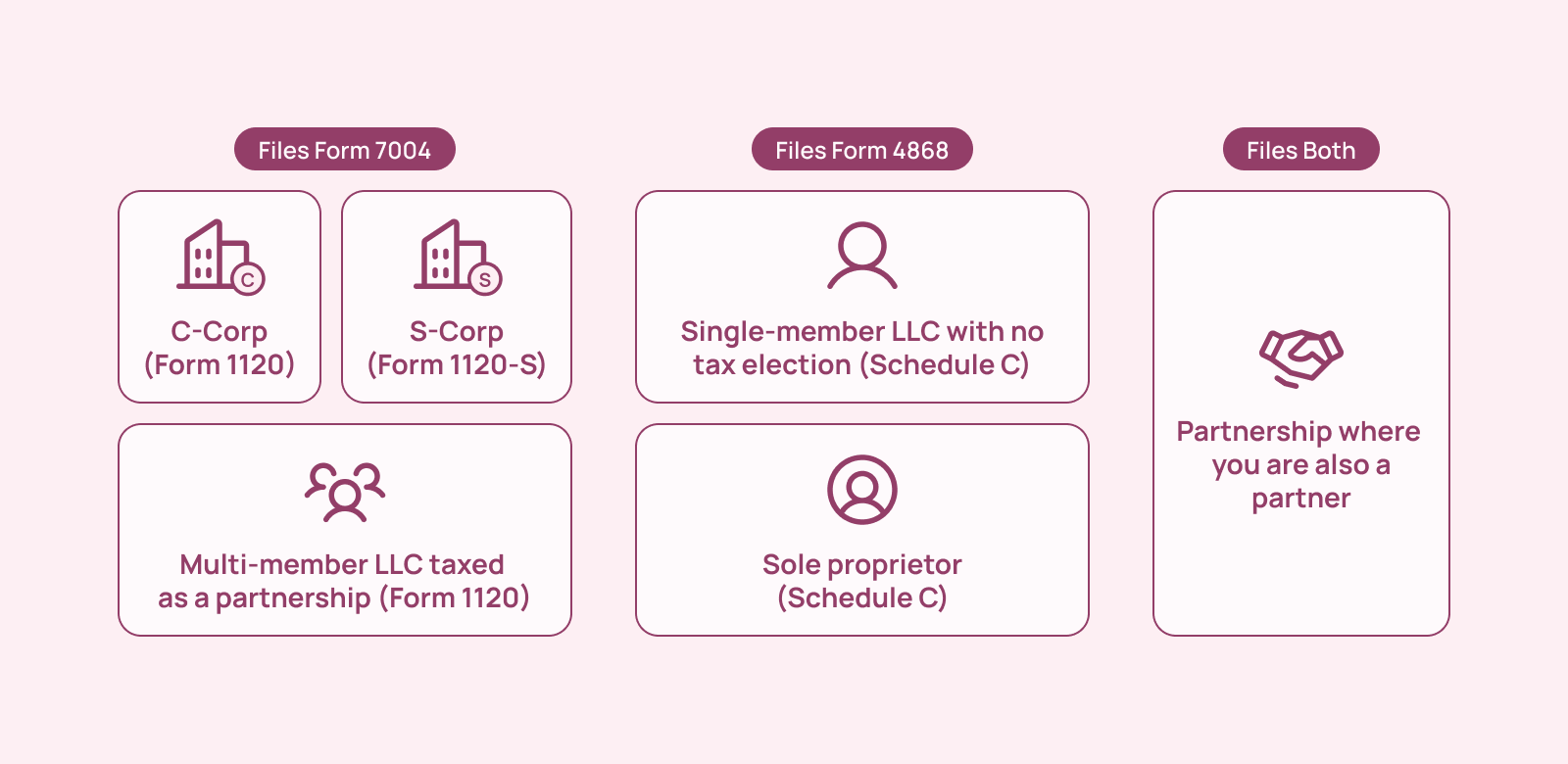

Who files which form?

The single most important factor in choosing between Form 7004 and Form 4868 is how your business is structured for tax purposes, not what your business does or what state you are registered in.

C-Corporation (Form 1120): File Form 7004. Your Delaware C-Corp is a separate tax entity and files its own return. The return is Form 1120. The extension is Form 7004.

S-Corporation (Form 1120-S): File Form 7004. An LLC that elected S-Corp status, or a corporation with an S-Corp election, files Form 1120-S. The extension is Form 7004.

Multi-member LLC taxed as a partnership (Form 1065): File Form 7004. A multi-member LLC files Form 1065. The extension is Form 7004.

Single-member LLC with no tax election (Schedule C): File Form 4868. A single-member LLC treated as a disregarded entity does not file a separate business return. The owner reports business income on Schedule C of their personal Form 1040. The extension is Form 4868 for the personal return.

Sole proprietor (Schedule C): File Form 4868. A sole proprietor reports business income on Form 1040 Schedule C. The extension is Form 4868. Filing Form 7004 for a sole proprietor does nothing and provides no protection from the failure-to-file penalty.

Partnership where you are also a partner: You may need both. A partnership files Form 1065 and uses Form 7004 for an extension. Each individual partner reports their share of partnership income on their personal Form 1040 and may need Form 4868 to extend their personal return, particularly when they are waiting for Schedule K-1s from the partnership.

2026 Deadlines

For the 2025 tax year (returns filed in 2026), here are the confirmed deadlines.

*March 15, 2026 falls on a Sunday, which moves the deadline to the next business day, Monday March 16, 2026.

**Trusts and estates filing Form 1041 receive a 5.5-month extension, not the standard 6 months, which places the extended deadline at September 30, 2026.

One additional note for C-Corporations: C corporations with tax years ending June 30 and beginning before January 1, 2026 are eligible for an automatic 7-month extension. For tax years beginning in 2026, the automatic extension period is 6 months. For most calendar-year C-Corps filing their 2025 return, the 5-month statutory rule under IRC Section 6081(b) applies, which is why the extension moves from April 15 to October 15 (exactly 6 months), not to a different date.

The most important rule: Extensions do not extend time to pay

This is the point that creates the most expensive surprises for founders who file extensions.

Filing Form 7004 or Form 4868 by the original due date gives you more time to file the paperwork. It does not give you more time to pay the tax you owe. The IRS expects full payment of any tax owed by the original filing deadline, regardless of whether an extension has been filed.

Here is what happens if you extend but do not pay by the original deadline:

The failure-to-pay penalty is 0.5% of the unpaid balance per month or part of a month, up to a maximum of 25% of the unpaid amount. Interest also accrues on the unpaid balance. In early 2026, the IRS interest rate is 7% for the first quarter and 6% for the second quarter, compounded daily. These charges run from the original due date, not from the extended filing deadline.

There is a safe harbor that protects you from the failure-to-pay penalty even if you cannot pay the full amount. For corporations filing Form 7004, the IRS will not assess the failure-to-pay penalty if the tax paid by the original due date equals at least 90% of the tax shown on the return. For individuals filing Form 4868, the same 90% standard applies.

Paying at least 90% of the estimated tax owed by the original deadline and paying the remainder with the filed return avoids the penalty, though interest continues to accrue on any unpaid balance.

The failure-to-file penalty is much more expensive than the failure-to-pay penalty. Filing an extension protects you from the failure-to-file penalty, which is 5% of unpaid tax per month up to 25%. If you owe tax and cannot file on time, filing the extension form even without paying anything eliminates the much larger failure-to-file penalty. You will still owe interest and the smaller failure-to-pay penalty, but the 5% per month failure-to-file penalty is cut entirely.

How to file form 7004?

Form 7004 must be filed by the original due date of the return you are extending.

The form requires your business name, EIN, tax year, and the specific form code for the return you are extending. Each return type on Form 7004 has a designated code number. Using the wrong code is one of the most common errors and can result in the extension being applied to the wrong return or rejected entirely.

You also need to include an estimate of the tax owed on line 6 of the form. This does not need to be exact, but it must be a reasonable good-faith estimate.

Form 7004 can be filed electronically for most business returns through IRS-authorized e-file providers. Form 7004 cannot be filed electronically for Forms 8612, 8613, 8725, 8831, 8876, or 706-GS(D). For all other covered returns, electronic filing is available and recommended by the IRS.

No signature is required on Form 7004. File a separate Form 7004 for each return you are extending. A single Form 7004 does not cover multiple return types.

How to file form 4868?

Form 4868 must be filed by April 15, 2026 for the 2025 tax year.

The form is straightforward. It requires your name, address, Social Security Number, an estimate of your total 2025 tax liability, the amount you have already paid through withholding and estimated payments, and the balance you are paying with the extension.

If you are paying additional tax with the extension, you can make that payment online through IRS Direct Pay or through your bank and have the payment count as an automatic Form 4868 filing. This means if you make a payment online and select "extension" as the reason, you do not need to separately file Form 4868. Save the payment confirmation number in case of any question.

If you are out of the country on the due date of your return and are a US citizen or resident, you are allowed 2 extra months to file your return and pay any amount due without requesting an extension. Interest will still be charged, however, on payments made after the due date. If you are out of the country and file a calendar year income tax return, you can pay the tax and file your return or Form 4868 by June 15, 2026. You can then file Form 4868 to receive an additional 4-month extension to October 15, 2026.

Common mistakes and how to avoid them

Filing Form 7004 for a sole proprietorship or single-member LLC. Sole proprietors and single-member LLCs without a tax election report on Schedule C of Form 1040. Form 7004 has no effect on a Form 1040 return. Filing Form 7004 in this situation gives you no protection from the failure-to-file penalty. You need Form 4868.

Filing Form 4868 for a C-Corp, S-Corp, or partnership. Form 4868 is for individual returns only. A Delaware C-Corp, S-Corp, or partnership must use Form 7004. Filing Form 4868 for a business entity return does not extend the business filing deadline.

Assuming the extension covers the state return. A federal extension does not automatically extend your state tax return deadline. Some states honor the federal extension; others require a separate state extension filing or a payment by a specific date. You need to check the requirements for every state where you are registered to do business.

Missing the extension deadline itself. Both Form 7004 and Form 4868 must be filed by the original due date of the return. Filing either form one day late means the extension is invalid and penalties run from the original deadline. File a few days early to avoid last-minute rejection issues from electronic filing systems.

Waiting for the K-1 before filing the personal extension. Partners and S-Corp shareholders often need Schedule K-1 forms from the entity before they can complete their personal return. If the partnership or S-Corp has filed Form 7004, the K-1s may not be ready before the personal return deadline. File Form 4868 for the personal return to extend it while the entity return is still being prepared.

What this means for India-US founders

If you are an Indian founder with a Delaware C-Corp that has an Indian subsidiary, you likely have both a business filing obligation and a personal filing obligation.

Your Delaware C-Corp files Form 1120 and uses Form 7004 for a business extension if needed. The C-Corp's original deadline is April 15, 2026, extending to October 15, 2026 if Form 7004 is filed.

Separately, if you are personally a US tax resident (green card holder, US citizen, or someone who meets the substantial presence test), you file a personal Form 1040 and use Form 4868 for a personal extension if needed. Your personal return deadline is April 15, 2026, extending to October 15, 2026 if Form 4868 is filed.

If you are an Indian founder who is not a US tax resident, you may still have a Form 1040-NR filing obligation if you have US-source income. Form 4868 also covers Form 1040-NR extensions.

One practical coordination issue: founders who own shares in the C-Corp and receive compensation as W-2 employees or dividends as shareholders need their personal return to reflect what the corporate return reports. If the C-Corp is on extension, it makes sense to also file Form 4868 for the personal return to ensure you have the time to coordinate the two returns accurately before filing either one.

A quick reference: Form 7004 vs Form 4868

Managing business and personal tax deadlines, extension filings, and payment estimates across a growing startup can create compliance gaps that add up quickly. Book a demo with Inkle to handle your C-Corp, partnership, and personal extension filings and make sure the right form reaches the IRS by the right deadline every year.

Frequently Asked Questions

Does filing a tax extension mean I have more time to pay my taxes?

No. This is the most common and most expensive misconception about tax extensions. Both Form 7004 and Form 4868 extend only the deadline to file your return, not the deadline to pay the tax you owe. The IRS expects payment of your full estimated tax liability by the original due date, April 15 for most individuals and C-Corps, and March 17 for partnerships and S-Corps in 2026. If you do not pay at least 90% of your estimated liability by the original deadline, the IRS will charge a failure-to-pay penalty of 0.5% per month on the unpaid balance plus daily compounding interest. Filing the extension does protect you from the much larger failure-to-file penalty of 5% per month, so it is always worth filing even if you cannot pay the full amount.

Which extension form does a single-member LLC use?

It depends on how the LLC is taxed. A single-member LLC that has not elected corporate taxation is treated as a disregarded entity. The owner reports business income on Schedule C of their personal Form 1040. The correct extension form is Form 4868 for the personal return. Form 7004 does not apply to this situation and provides no protection if filed instead. If the single-member LLC has elected to be taxed as a C-Corp using Form 8832, it files Form 1120 and uses Form 7004. If it has elected S-Corp status, it files Form 1120-S and uses Form 7004.

What is the 2026 extended deadline for an S-Corp or partnership?

For a calendar-year S-Corp or partnership filing for the 2025 tax year, the original due date is March 16, 2026 (March 15 falls on a Sunday). Filing Form 7004 by March 17, 2026 extends the deadline to September 15, 2026. Note that this is an extension to file the return, not to pay any tax owed. The S-Corp itself generally has no tax to pay since income passes through to shareholders, but partnerships with withholding obligations should confirm their specific payment deadlines.

Can I file both Form 7004 and Form 4868 for the same tax year?

Yes, and for many founders this is the right approach. If you own a C-Corp or are a partner in a partnership, you may need Form 7004 to extend the business return and Form 4868 to extend your personal return. The two forms apply to completely separate returns and are filed independently. Filing Form 7004 for your business does not automatically extend your personal return, and filing Form 4868 for yourself does not automatically extend your business return. Coordination between the two is especially important when Schedule K-1 forms from the business return feed into the personal return.

In this article

.jpg)