EIN vs ITIN vs SSN: Which Tax Identifier Does Your US Startup Actually Need?

If you are an Indian founder who just incorporated a Delaware C-Corp, you have probably already encountered the three-letter acronym pile-up: EIN, SSN, ITIN. Banks ask for one. IRS forms ask for another. Payment processors like Stripe ask for something that might be any of the three.

Getting confused about which one you need is not a sign that you missed something obvious. These three tax identifiers serve genuinely different purposes, apply to different people and entities, and are obtained through completely different processes. Using the wrong one on a form creates delays, rejected applications, and sometimes IRS mismatches that take months to sort out.

This guide explains exactly what each identifier is, which one your startup needs, when you might need more than one, and what Indian founders specifically need to know about obtaining them without a US Social Security Number.

Before going into detail, here is the one-line version of each:

EIN (Employer Identification Number): Your business's tax ID. Identify your company to the IRS. Every corporation, partnership, and multi-member LLC needs one.

SSN (Social Security Number): An individual's tax ID for US citizens and authorized residents. Issued by the Social Security Administration. Identifies you as a person, not a business.

ITIN (Individual Taxpayer Identification Number): An individual's tax ID for people who have US tax obligations but are not eligible for an SSN. Issued by the IRS. Used only for tax purposes.

The key distinction is this, EIN is for your business entity. SSN and ITIN are for individual people. You cannot use your EIN in place of your SSN or ITIN on a personal tax return, and you cannot use your SSN or ITIN in place of your business's EIN on a business filing.

What is a TIN and how do EIN, SSN, and ITIN relate to it?

TIN stands for Taxpayer Identification Number. It is the umbrella term the IRS uses for any tax ID number. An EIN is a TIN. An SSN is a TIN. An ITIN is a TIN. When a form asks for a TIN without specifying which type, you use whatever is appropriate for the context: your EIN if the form is about your business, your SSN or ITIN if the form is about you personally.

All three are nine-digit numbers. EINs are formatted as XX-XXXXXXX. SSNs and ITINs are formatted as XXX-XX-XXXX. ITINs always start with the digit 9, which distinguishes them visually from SSNs, which do not start with 9.

EIN: Your business's tax identifier

The EIN, also called the Federal Tax Identification Number or FEIN, is a unique nine-digit number assigned by the IRS to identify a business entity. Every Delaware C-Corp, S-Corp, multi-member LLC, and partnership must have an EIN. It is the number your business uses to file tax returns, open bank accounts, hire employees, and establish business credit.

Who must get an EIN:

A Delaware C-Corp must have an EIN as soon as it is formed. This is true regardless of whether the founders are US citizens, permanent residents, or non-residents living outside the United States. The entity's nationality or tax status does not affect this requirement.

A single-member LLC that is a disregarded entity is not legally required to have an EIN unless it has employees, certain excise tax obligations, or is required to file certain information returns. However, most single-member LLC owners still get an EIN to avoid sharing their personal SSN with banks, clients, and vendors on W-9 forms and vendor agreements.

A multi-member LLC always needs an EIN because it files its own tax return (Form 1065).

Who is the responsible party on an EIN application:

When you apply for an EIN using Form SS-4, the IRS requires you to identify a "responsible party." This is the individual who ultimately owns or controls the entity, or who exercises ultimate effective control over the entity. The responsible party must provide their own personal tax ID number on Form SS-4, which must be either their SSN or their ITIN. This is a required field for the online application. It is the reason foreign founders without either number cannot use the IRS online portal and must apply by fax or mail instead.

This is where Indian founders run into the first confusion. You need your personal tax ID to apply for your business's EIN. If you do not have an SSN (because you are not a US citizen or permanent resident), you would normally need an ITIN. However, there is an important exception.

Indian founders can get an EIN without an SSN or ITIN:

The IRS online EIN application requires a US SSN or ITIN. However, foreign founders who have neither can still get an EIN by filing Form SS-4 by fax or mail. On line 7b of Form SS-4, you enter "Foreign" in place of an SSN or ITIN. The IRS does issue EINs to non-resident foreign founders without SSNs or ITINs regularly.

The fax method typically takes four to fourteen business days. The mail method takes four to six weeks. There is no fee for applying for an EIN regardless of your method or residency status.

Once the EIN is issued, it never expires. An EIN assigned to a business entity stays with that entity permanently unless the business is dissolved or undergoes a structural change that requires a new EIN.

SSN: The individual tax ID for US citizens and authorized residents

The Social Security Number is a nine-digit number issued by the Social Security Administration (not the IRS) to US citizens, permanent residents (green card holders), and certain authorized non-citizen workers with eligible visa types.

The SSN serves two purposes simultaneously. It is a tax identification number used for filing individual income tax returns. It is also a work authorization identifier, confirming that the holder has the legal right to work in the United States. This dual purpose is what distinguishes the SSN from the ITIN, which is strictly for tax purposes and carries no work authorization.

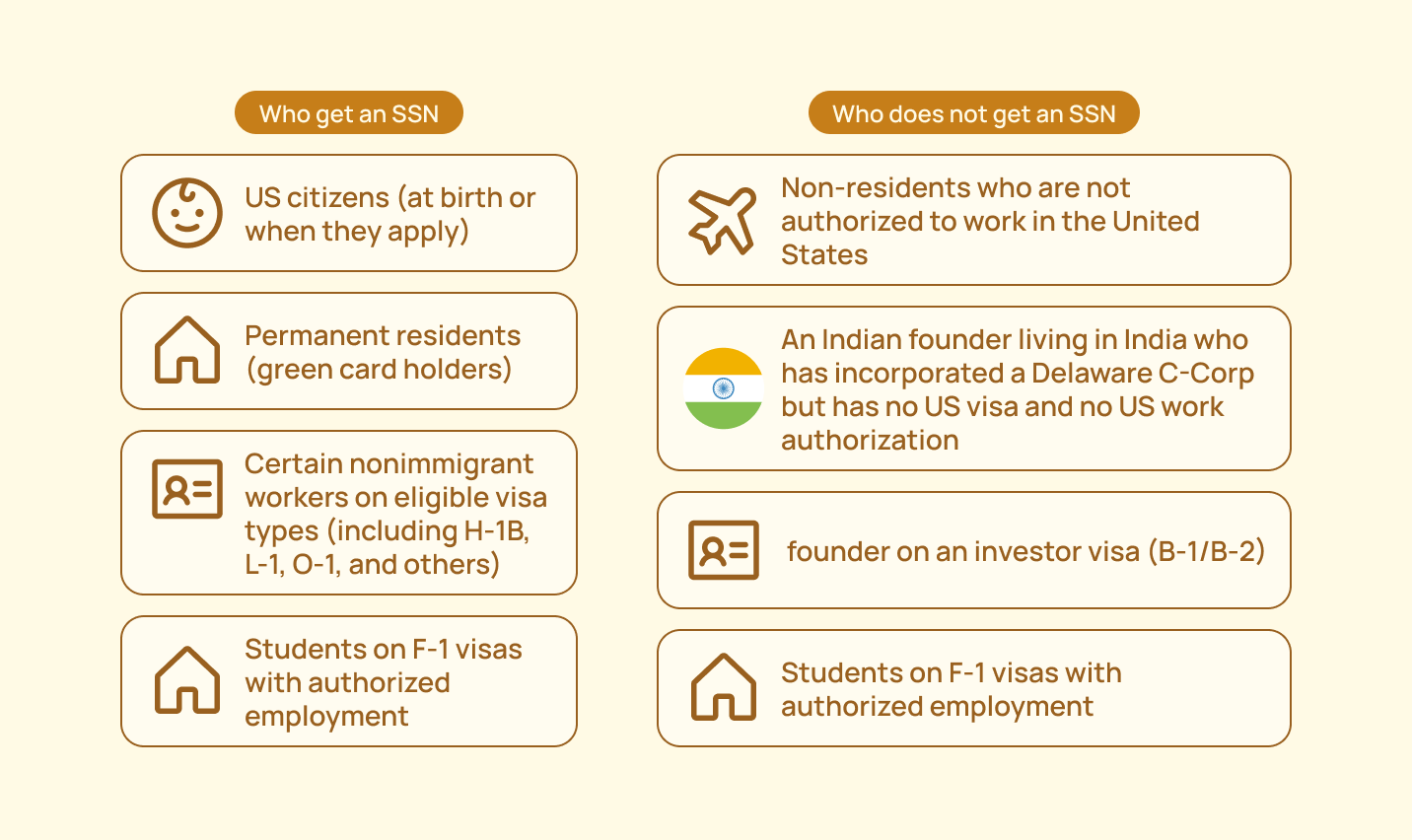

Who gets an SSN:

US citizens receive an SSN at birth or when they apply. Permanent residents (green card holders) receive an SSN. Certain nonimmigrant workers on eligible visa types (including H-1B, L-1, O-1, and others) can apply for an SSN. Students on F-1 visas with authorized employment can also apply.

Who does not get an SSN:

Non-residents who are not authorized to work in the United States cannot get an SSN. An Indian founder living in India who has incorporated a Delaware C-Corp but has no US visa and no US work authorization is not eligible for an SSN. A founder on an investor visa (B-1/B-2) typically is not eligible either.

If your SSN application is pending, you cannot simultaneously apply for an ITIN. A person can only have one individual tax identifier. If you have an SSN, you use that. If you subsequently obtain an SSN after having an ITIN, the ITIN is invalidated and you must notify the IRS to combine your tax records under the SSN.

ITIN: The individual tax ID for foreign nationals with US tax obligations

The Individual Taxpayer Identification Number is issued by the IRS to individuals who are required to file US taxes or appear on a US tax filing but are not eligible for an SSN.

Every ITIN starts with the digit 9, formatted as 9XX-XX-XXXX. This distinguishes it from an SSN visually. An ITIN is strictly for federal tax purposes. It does not authorize work, it does not make you eligible for Social Security benefits, and it does not constitute any form of immigration status.

Who needs an ITIN:

An ITIN is needed by a non-resident alien who has a US federal tax filing requirement. This includes:

An Indian founder who owns shares personally in a US entity (rather than through a holding company) and who has US-source income that creates a personal filing obligation. If your Delaware C-Corp is profitable and you receive a salary or dividends, you may have a personal US tax obligation that requires you to file Form 1040-NR as a non-resident alien. Filing that return requires an ITIN.

A foreign co-founder who is a non-resident alien and needs to make a Section 962 election to manage GILTI tax obligations as an individual shareholder. The election requires an ITIN on the personal return.

An S-Corp election for an LLC requires a Form 2553 with the EIN of the entity and the SSN or ITIN of the responsible party. If you want to make an S-Corp election and you have no SSN, you need an ITIN.

Spouses and dependents of US visa holders who are claimed on a US tax return as dependents also need ITINs.

When an ITIN is not required:

If you are a foreign founder whose only US footprint is owning shares in a Delaware C-Corp as a foreign person, and you do not personally receive US-source income that creates a tax filing obligation, you may not need an ITIN at all. The C-Corp itself uses its EIN. You use your EIN as the business's identifier. Many non-resident LLC and C-Corp owners operate for years with only an EIN for the business entity and no personal ITIN, because no personal US tax return is required.

How to get an ITIN:

You apply using Form W-7 (Application for IRS Individual Taxpayer Identification Number). You must attach a federal income tax return (Form 1040-NR for non-residents) that demonstrates the tax filing need. You must also provide original identity documents or certified copies proving your identity and foreign status, with a valid passport being the most accepted single document.

Processing takes approximately seven weeks under normal conditions and nine to eleven weeks during peak filing season (January 15 to April 30) or for applications submitted from outside the United States. You can submit through the mail directly to the IRS ITIN Operations in Austin, Texas, through a Certifying Acceptance Agent who can verify your documents locally without sending originals, or in person at an IRS Taxpayer Assistance Center.

These are IRS estimates and actual times can vary based on application volume and completeness of documentation.

ITIN expiration and renewal:

Unlike an EIN, an ITIN can expire. Under the Protecting Americans from Tax Hikes (PATH) Act of 2015, an ITIN that has not been used on at least one federal tax return in three consecutive years automatically expires on December 31 of the third year. ITINs not used on any federal return in tax years 2022, 2023, or 2024 expired on December 31, 2025.

If you file a return with an expired ITIN, the IRS will process the return but delay any refund and disallow certain tax credits, including the Child Tax Credit and the American Opportunity Tax Credit, until the ITIN is renewed. To renew, you complete Form W-7 again and check the "Renew an existing ITIN" box. Your ITIN number does not change during renewal. You are reactivating the same number.

If your ITIN is only used on information returns such as Form 1099 where you are the recipient, you do not need to renew it for that purpose. Expired ITINs can continue to appear on information returns.

Which one does your startup actually need?

The answer depends entirely on your structure and situation.

You are an Indian founder who has incorporated a Delaware C-Corp and you live in India with no US visa:

Your C-Corp needs an EIN immediately. You apply using Form SS-4 by fax or mail, entering "Foreign" on line 7b in place of an SSN. You personally do not need an ITIN unless and until you have a personal US tax filing obligation, such as receiving a salary from the C-Corp or dividends, or making a Section 962 election for GILTI.

You are an Indian founder on an H-1B or O-1 visa living in the United States:

You are eligible for an SSN. Apply for it through the Social Security Administration. Once you have an SSN, use that as your personal tax identifier on all personal filings. You do not need an ITIN. Your C-Corp still needs its own separate EIN.

You are an Indian founder who relocated to the US on an investor or tourist visa temporarily without work authorization:

You are not eligible for an SSN. If you have a personal US tax obligation (because you were in the US long enough to meet the substantial presence test, or because you have US-source income), you need an ITIN. Apply using Form W-7. Your C-Corp still needs its own separate EIN regardless.

You are an Indian founder who owns shares personally (not through a US holding entity) in an Indian company that qualifies as a CFC:

If you are a US tax resident (green card holder, citizen, or substantial presence test met), you use your SSN on personal returns including any GILTI inclusions. If you are a non-resident with a US tax filing obligation due to US-source income, you need an ITIN.

You are a sole proprietor operating under your personal name with no separate business entity:

You use your SSN (or ITIN if you are not eligible for an SSN) for all business and personal tax purposes. You are not required to get an EIN unless you hire employees. However, getting an EIN even as a sole proprietor is worth considering if you want to avoid sharing your personal SSN on W-9 forms with clients and vendors.

The 3 numbers side by side

Common mistakes Indian founders make

Using their EIN in place of an SSN or ITIN on a personal return. An EIN identifies the business, not the individual. Putting an EIN in the SSN field on a Form 1040-NR is an error that will cause processing problems and IRS notices.

Assuming they need an ITIN before getting an EIN. You do not need an ITIN to get an EIN as a foreign founder. These are two separate applications with separate processes. Get your EIN first (it is faster), and get your ITIN only when you actually have a personal US tax filing obligation.

Applying for an EIN online when they are a foreign founder. The IRS online EIN tool requires a US SSN or ITIN. Foreign founders without either must use Form SS-4 by fax or mail. Attempting the online application without an SSN or ITIN will result in a failed session.

Not renewing an ITIN after years of non-use. ITINs expire automatically after three consecutive years without being used on a federal tax return. Many founders obtain an ITIN for an initial filing, do not file a return for several years (perhaps because they had no filing obligation), and then discover the ITIN has expired when they need it again. Check your ITIN status before each filing season if you have not filed for two or more consecutive years.

Thinking an ITIN authorizes employment. An ITIN is a tax processing number only. It does not authorize work in the United States, does not provide immigration status, and does not entitle the holder to Social Security benefits.

Navigating EIN applications, ITIN requirements, and the personal tax filing obligations of a cross-border India-US founder structure is exactly the kind of complexity Inkle handles. Book a demo with Inkle to make sure your startup's tax IDs are set up correctly from day one.

Frequently Asked Questions

Can I get an EIN for my Delaware C-Corp without an SSN or ITIN?

Yes. Foreign founders who do not have a US SSN or ITIN can still obtain an EIN for their US business entity by filing Form SS-4 by fax or mail. On line 7b of Form SS-4, you write "Foreign" in place of an SSN or ITIN. The fax option typically takes four to fourteen business days. There is no fee. You cannot use the IRS online EIN application because it requires an SSN or ITIN. Once issued, your EIN never expires.

Do I need both an EIN and an ITIN as an Indian founder with a Delaware C-Corp?

Not necessarily, and not immediately. Your C-Corp needs an EIN right away. You personally only need an ITIN if you have a US federal tax filing obligation as an individual, such as receiving US-source income, filing Form 1040-NR, or making certain elections like a Section 962 election for GILTI. Many foreign founders operate their US entity for years with only the business EIN and no personal ITIN, because their personal situation creates no US individual filing obligation. Get the ITIN when you actually need it for a personal filing.

What is the difference between an ITIN and an SSN?

Both are individual tax identification numbers formatted as nine digits. The SSN is issued by the Social Security Administration to US citizens, permanent residents, and certain authorized non-citizen workers. It authorizes employment and tracks Social Security earnings. The ITIN is issued by the IRS to individuals who need to file US taxes but are not eligible for an SSN. It starts with the digit 9, is strictly for tax filing purposes, and does not authorize employment, provide immigration benefits, or track Social Security earnings. A person can only have one of these: if you have an SSN you use that, and if you later get an SSN after having an ITIN, the ITIN is invalidated. Unlike an SSN, an ITIN can expire if not used on a federal return for three consecutive years.

Can two people at the same startup share an EIN?

No. An EIN is assigned to a specific legal entity, not to individuals. Each separate business entity has its own unique EIN. If two founders co-own a C-Corp, the C-Corp has one EIN. Each founder individually uses their own SSN or ITIN on their personal returns. If the same founders also own a separate LLC, that LLC would need its own separate EIN. A single EIN cannot be shared between two different legal entities.

In this article

.jpg)