How to Self-File Startup Tax Successfully?

Every year, founders hit the same decision point: Should I just file taxes myself, or do I need help?

For individuals with straightforward income, self-filing usually works. A few forms, some deductions, and a clear process. But for startups, it’s rarely this simple. When you have co-founders, operate in multiple states, or have cross-border elements, tax filing changes. It stops being a single task. Instead, it becomes a system of interconnected filings.

Founders often don’t realize this early. They assume tax filing means submitting one return. But a startup may need to handle federal filings, multiple state returns, and international reporting at the same time. Missing even one requirement can trigger penalties that are far larger than the cost you were trying to save by filing on your own.

So the real question is not whether you can self-file? We’ll find this out in this article!

Questions this article answers:-

- What does it mean to self-file taxes and who should consider it?

- How can you file taxes for free or at low cost?

- Can startup founders self-file business taxes legally?

- What documents do you need before filing?

- What are the biggest risks and penalties in DIY tax filing?

- When should you stop self-filing and hire help?

- How can tools like Inkle simplify compliance and bookkeeping?

What Does Self Filing Startup Taxes Involve?

Tax filing complexity depends on how you file. Using guided software is very different from preparing returns manually. Software can assist with calculations and basic validations. However, it may not always identify structural issues, such as missing international forms or state-level obligations. That gap is where most self-filers run into problems.

Self-filing means preparing and submitting your own tax return without hiring a CPA or tax preparer. This can be done in two ways:

- Using tax software that guides you through inputs and generates the required forms

- Preparing and filing forms manually, either electronically or by mail

- Handling both federal and state filings yourself, including deadlines and extensions

- Taking responsibility for accuracy, completeness, and compliance

For startup founders, it can extend to business returns such as Form 1120 or 1065, along with additional schedules and disclosures.

Here’s how self-filing taxes compare against hiring a professional:

Self-filing works well when the situation is simple and predictable. As soon as filings depend on interpretation, multiple entities, or cross-border rules, the margin for error increases quickly.

How to Choose the Right Way to File Taxes Based on Your Situation?

The decision to self-file taxes should not start with how you will file. It should start with whether your situation is simple enough to handle on your own.

For startup founders, the complexity increases much faster. Even in the early stages, factors like entity structure, multiple founders, or operating in more than one state can change what needs to be filed.

i) Can You Legally Self-File Taxes for Your Startup?

The answer is yes, you can.

There is no legal requirement to hire a CPA or tax preparer. An authorized officer of a corporation or a member of an LLC can prepare and file the return themselves. This applies to most common startup structures, including Delaware C-Corps and LLCs formed through platforms like Stripe Atlas or Clerky.

But legality is not the same as practicality.

The real challenge is not filing the return. It is identifying everything that needs to be filed. A startup may have to handle federal returns, state filings, and additional reporting depending on its structure. Missing one of these can create issues even if the main return is filed correctly.

ii) Check If You Qualify for Simple Filing

Before deciding to self-file, it helps to clearly define whether your situation is actually simple.

A startup that has no revenue, operates in one state, and has only US-based founders may still qualify as simple. But this changes quickly once you introduce additional variables.

If your setup includes any of the following, your filing is no longer straightforward:

- More than one state of operation (e.g., employees in multiple states)

- Any foreign founder or ownership structure (e.g., non-U.S. investors)

- A subsidiary or team outside the US (e.g., international operations)

- Multiple income streams or complex expense categories (e.g., R&D credits, crypto transactions)

At that point, the filing process is no longer just about accuracy. It becomes about identifying what needs to be filed in the first place.

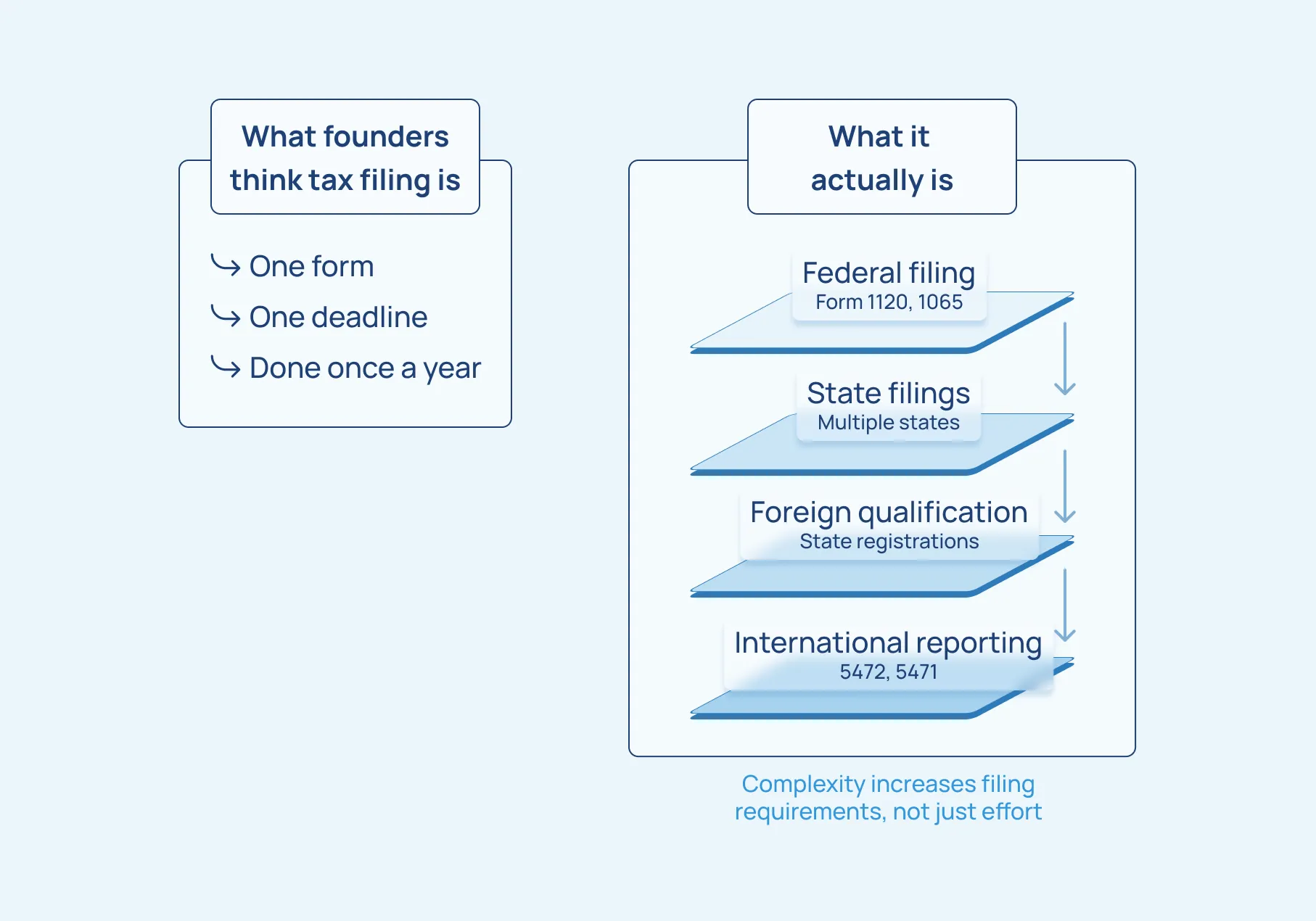

iii) How Tax Filing Complexity Increases

Tax complexity does not increase gradually. It usually jumps in layers.

At the base level, you have your primary return. This is what most people think of when they think about filing taxes. But for startups, that is only the starting point.

The next layer comes from state-level obligations. If your business operates in more than one state, you may need to file separate returns in each of those states. For example, if a startup hires a single remote employee in California, that action alone could establish 'nexus,' requiring the business to file startup tax returns in California.

Beyond that, international elements add another layer. For instance, a U.S. corporation that is 25% or more foreign-owned must file Form 5472, Information Return of a 25% Foreign-Owned U.S. Corporation or a Foreign Corporation Engaged in a U.S. Trade or Business, which introduces specific reporting requirements often overlooked by founders.

iv) Decide Based on Risk, Not Just Cost

Most people approach self-filing as a cost-saving decision. But for startups, the more relevant factor is risk.

If your situation is simple, the risk is low. You are unlikely to miss major requirements, and the cost savings make sense.

But as complexity increases, the downside becomes more significant. Missing a filing requirement or reporting something incorrectly can lead to penalties that are far higher than the cost you were trying to avoid.

Here’s how different tax filing methods compare:

The cost difference often drives the initial decision. But for startups, the more important comparison is between cost and exposure.

The better way to approach this decision is to ask the following:

- Do you fully understand what needs to be filed?

- Can you identify all required filings across federal, state, and international levels?

- Are you confident that nothing important is being missed?

If the answer to any of these is uncertain, the decision is no longer just about saving money. It becomes about avoiding mistakes that are difficult to fix later.

v) Tax Filing Methods for Business Returns

Once you decide to self-file, you also need to decide how to submit your return. There are two primary methods, and each comes with its own trade-offs.

- Paper filing gives you full control over the process. You prepare the forms manually and mail them to the IRS. This method is straightforward but slow, and there are no built-in checks to catch errors.

- E-filing is faster and reduces basic mistakes like calculation errors. It also gives quicker confirmation that your return has been received.

- Processing timelines differ significantly. Electronic filings are processed in days, while paper filings can take weeks or even months.

The method you choose does not change your obligations. It only affects how efficiently your return is processed.

Prepare All Required Documents Before You File Taxes

For startups, your tax return is built on your financial records, ownership structure, and transaction history. If these are not clean, even a correctly filled form can be wrong.

Think of this step as preparation, not paperwork. The more structured your inputs are, the smoother the filing process becomes.

i) Gather Personal Tax Documents

If you are filing as an individual or reporting personal income alongside your startup, you need to start with basic income and deduction records.

This typically includes:

- W-2 forms for salary income

- 1099 forms for freelance or contract income

- Investment income statements such as dividends or capital gains

- Proof of deductions, including rent, insurance, or eligible expenses

- Prior year tax returns for reference and consistency

Having these documents ready ensures that your income is reported correctly and that you do not miss any deductions you are eligible for.

ii) Organize Startup Financial Records

For founders, this is where most of the work lies. Your business return depends entirely on how well your financial records are maintained.

At a minimum, you should have:

- Income statements showing revenue and expenses for the year

- Balance sheets reflecting assets, liabilities, and equity

- Detailed expense records categorized correctly

- Payroll reports if you have employees or founders on payroll

- Bank and payment processor statements that reconcile with your books

Inaccurate financial records directly lead to an inaccurate tax return.F For example, your balance sheet should tie to your books, and your expenses should match your actual transactions. These are not optional checks. They are foundational to correct filing.

Step-by-Step Process to E-File Your Startup Taxes

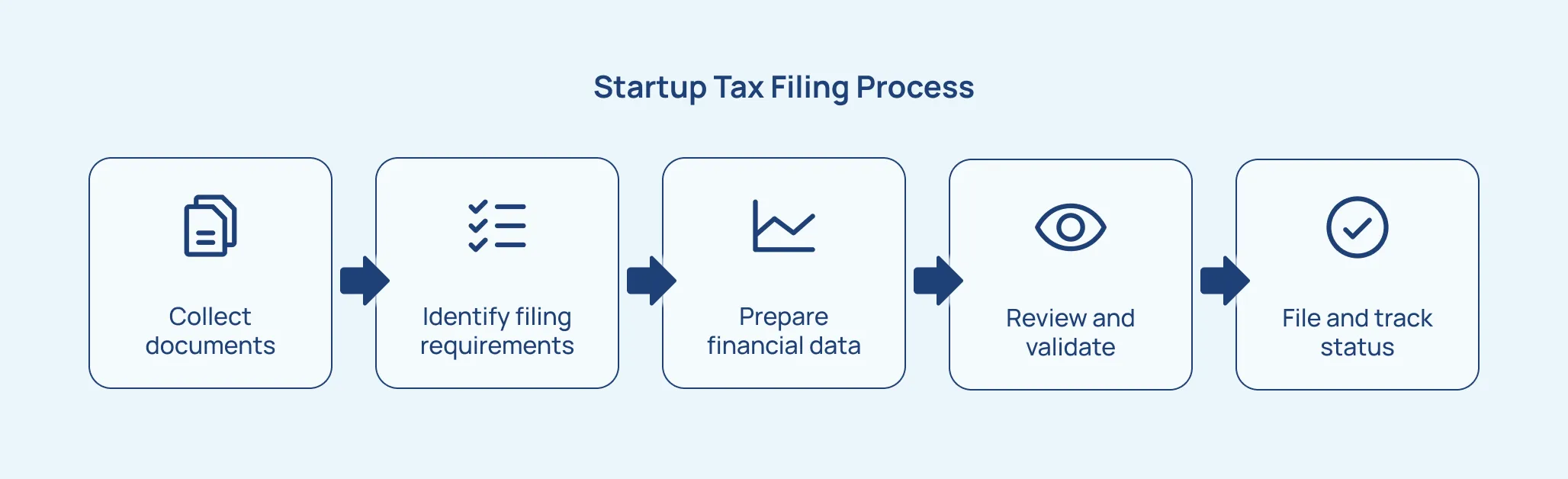

Once your documents are in place and you understand what needs to be filed, the next step is execution. This is where most self-filers either move smoothly or get stuck. A structured process helps you avoid going back and forth between forms, missing details, or making last-minute errors.

Follow this step-by-step process to self-file your startup taxes:-

Step 1: Collect all documents and financial records

Start with everything you prepared earlier. Make sure your income, expenses, and financial statements are complete and consistent. Any gaps at this stage will carry forward into your filing.

Step 2: Select your filing method and confirm requirements

Decide whether you will file electronically or through paper. At the same time, confirm what forms you actually need to submit based on your situation, including any state or additional filings.

Step 3: Enter financial details carefully

Begin with your primary return and input all financial data. For startups, ensure that your numbers tie back to your books. This includes revenue, expenses, and balance sheet figures where required.

Step 4: Review for errors and missing information

Go through the entire return before submission. Check for inconsistencies, missing schedules, or incomplete sections. This is especially important for areas where additional disclosures may be required.

Step 5: Submit and track your filing status

Once submitted, confirm that your return has been accepted. Keep a copy of everything you filed and track any follow-ups, including payments, refunds, or additional filings.

Use Inkle to Simplify Startup Tax Filing and Compliance

Self-filing works best when your situation is simple and clearly defined. But as soon as your startup starts growing, the number of moving parts increases. You are no longer dealing with just one return. You are managing bookkeeping, multiple filings, and compliance deadlines at the same time.

This is where most founders start feeling the gap. The challenge is not just filing taxes. It is keeping everything aligned so that your filings are accurate and complete.

Inkle is designed to handle exactly this problem for startups.

Instead of treating bookkeeping, tax filing, and compliance as separate tasks, Inkle connects them into a single workflow. This reduces the chances of mismatched data, missed filings, or last-minute corrections.

- Automates bookkeeping so your financial records stay clean and ready for filing

- Prepares accurate reports that feed directly into your tax returns

- Tracks compliance deadlines across federal, state, and international filings

- Reduces the risk of penalties by identifying requirements early

Schedule a demo with Inkle to simplify your startup tax filing.

Frequently Asked Questions

What is the deadline to self-file taxes each year?

For most individuals and C-corporations, the deadline is April 15 for calendar-year filings. Partnerships and S-corporations typically have a March 15 deadline.

Important: Extensions for startup taxes are available, but they extend the filing timeline, not the payment deadline.

Can startup founders file taxes without hiring a CPA

Yes, founders can legally self-file their business taxes. However, this is practical only when the startup is simple, with no foreign ownership, no subsidiary, and operations in a single state.

How do you know if you qualify for free tax filing

Free filing usually applies to individuals within certain income limits and simple filing scenarios. It rarely applies to startups or business entities with additional compliance requirements.

What are the biggest mistakes people make when self-filing taxes

Common issues include missing required forms, incorrect reporting of income or expenses, and overlooking state or international filing requirements. These mistakes often come from incomplete understanding rather than calculation errors.

Should freelancers and contractors self-file or use software

Freelancers with straightforward income can often self-file. As income sources grow or deductions become more complex, structured filing support becomes more useful to avoid errors.

How does bookkeeping impact accurate tax filing

Your tax return is based on your financial records. If your books are incomplete or incorrect, your filing will also be inaccurate. Clean and reconciled records are essential before filing.

When should you switch from DIY tax filing to professional help

You should reconsider self-filing when your startup introduces complexity, such as foreign ownership, multi-state operations, fundraising activity, or rapid growth. These factors increase both filing requirements and risk exposure.

In this article