How to prepare GAAP-Compliant financial statements for the first time

GAAP, which stands for Generally Accepted Accounting Principles, is the standard framework of accounting rules that US companies use to prepare financial statements. It is maintained by the Financial Accounting Standards Board (FASB) and enforced for public companies by the Securities and Exchange Commission. For private startups, GAAP compliance is not legally required until you go public, but it becomes practically required the moment you raise institutional capital. Every Series A investor, every lender, and every acquirer will ask for GAAP-compliant financials. If yours are not ready, the due diligence process becomes significantly harder and more expensive to fix.

This guide explains exactly what GAAP compliance requires for a startup preparing its financial statements for the first time, including how to set up your chart of accounts, what accrual accounting means in practice, how to apply ASC 606 revenue recognition, what the four core financial statements must contain, and what footnote disclosures are required. If you want to understand the differences between GAAP and IFRS before going further, our guide on GAAP vs IFRS for startups covers that foundation.

What GAAP compliance actually means for a startup?

GAAP is not a single document or a checklist. It is a collection of principles, standards, and interpretations issued by FASB through the Accounting Standards Codification (ASC), which is the authoritative source of US GAAP for non-governmental entities.

For a startup, GAAP compliance primarily means three things:

You use accrual accounting, not cash accounting. Under accrual accounting, you record revenue when it is earned and expenses when they are incurred, regardless of when cash actually moves. Cash accounting, which many early-stage startups use for simplicity, records transactions only when money is received or paid. GAAP requires accrual accounting for financial reporting. This is not optional.

Your financial statements are prepared on a consistent basis across reporting periods. GAAP requires that you apply the same accounting methods from one period to the next. If you change a method, you must disclose the change and explain its impact.

Your statements include the required components and disclosures. A GAAP-compliant set of financial statements includes four core statements plus footnote disclosures. Producing only a profit and loss report does not constitute GAAP-compliant financial statements.

Most startups do not need full public-company-style GAAP compliance from day one, but they do need financials that are consistent, accurate, credible, and appropriate for their stage. Accrual accounting is part of GAAP, but it is not the same thing as full GAAP compliance. A company must use accrual accounting to be GAAP-compliant, but using accrual accounting alone does not make the company fully GAAP-compliant.

The practical goal for an early-stage startup is to build toward GAAP compliance in stages. The areas that matter most in the early years are accrual accounting, correct revenue recognition, accurate balance sheet categorization, and basic footnote disclosures. As you approach Series A and beyond, the expectation becomes fuller compliance including audit-ready documentation.

Step 1: Switch to accrual accounting

The first step in preparing GAAP-compliant financial statements is switching your books from cash basis to accrual basis if you have not done so already. If you are still recording revenue when you receive payment and expenses when you write the check, your books are not GAAP-compliant.

Under accrual accounting, the timing of recognition is governed by when transactions are earned or incurred, not when cash moves. Here is what this means in concrete terms for the most common startup scenarios:

Annual subscription contract paid upfront. Under cash accounting, a $120,000 annual contract paid in January would show $120,000 of revenue in January. Under accrual accounting, you recognize $10,000 per month across the 12-month service period. The remaining unrecognized amount sits on your balance sheet as deferred revenue, which is a liability.

Vendor invoice received but not yet paid. Under cash accounting, you record the expense when you pay the invoice. Under accrual accounting, you record the expense when you receive the services, and the unpaid amount appears as accounts payable on your balance sheet.

Employee payroll that spans a month boundary. If a pay period ends on December 31 but payroll is not processed until January 5, the December 31 balance sheet must include an accrued payroll liability for the unpaid wages.

If you have been on cash basis and need to make the switch official for IRS purposes, you will need to file Form 3115 (Application for Change in Accounting Method) with your federal tax return. Our guide on Form 3115 covers the mechanics of this process including the Section 481(a) adjustment that reconciles the gap between your old and new methods.

Step 2: Set up a GAAP-Compliant chart of accounts

The chart of accounts (COA) is the structured index of every account in your general ledger. Before you can prepare GAAP-compliant financial statements, your chart of accounts must be organized in a way that maps directly to the structure of those statements.

A typical GAAP-aligned chart of accounts uses a logical numbering system to organize five primary account categories: Assets, numbered in the 1000 to 1999 range; Liabilities, numbered in the 2000 to 2999 range; Equity, numbered in the 3000 to 3999 range; Revenues, numbered in the 4000 to 4999 range; and Expenses, numbered in the 5000 to 9999 range. This structure keeps your entries organized and ensures your financial data rolls up correctly into your statements.

For a startup, here is what each section should contain at minimum:

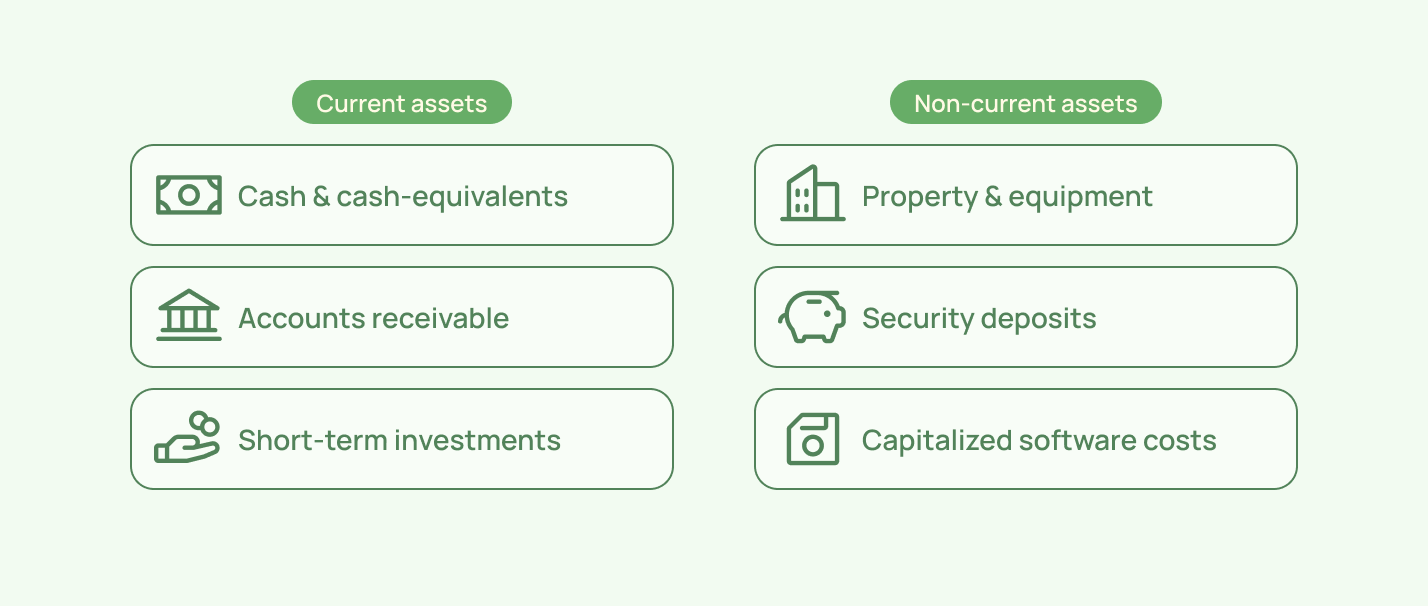

Assets (1000-1999) Current assets: cash and cash equivalents, accounts receivable, prepaid expenses, and short-term investments. Non-current assets: property and equipment (net of accumulated depreciation), security deposits, and capitalized software costs where applicable.

Liabilities (2000-2999) Current liabilities: accounts payable, accrued expenses, deferred revenue (current portion), and the current portion of any long-term debt. Non-current liabilities: long-term debt, deferred revenue (non-current portion), and any other obligations due beyond 12 months.

Equity (3000-3999) Common stock, additional paid-in capital, accumulated deficit, and any other comprehensive income items. C-Corporations use retained earnings (or accumulated deficit for startups that have not yet been profitable).

Revenue (4000-4999) Break this down by product line or revenue stream. A SaaS startup might have subscription revenue, professional services revenue, and usage-based revenue as separate accounts. Keeping these separate is critical for investor reporting and revenue recognition accuracy.

Expenses (5000-9999) Organize expenses into cost of revenue (COGS) and operating expenses. Within operating expenses, common categories include research and development, sales and marketing, and general and administrative. Keeping R&D separate from G&A is important because GAAP has specific rules about how R&D costs are treated.

One structural note: your chart of accounts should mirror the layout of your financial statements. Every balance sheet account should trace directly to a line on your balance sheet. Every income statement account should trace to a line on your income statement. If you cannot draw a direct line from an account in your COA to a line in your financial statements, the account may be misclassified.

Step 3: Apply ASC 606 revenue recognition correctly

Revenue recognition is the area where most startups are non-compliant without knowing it. Under GAAP, revenue is governed by ASC 606 (Revenue from Contracts with Customers), which FASB issued to standardize how all US companies recognize revenue from customer contracts.

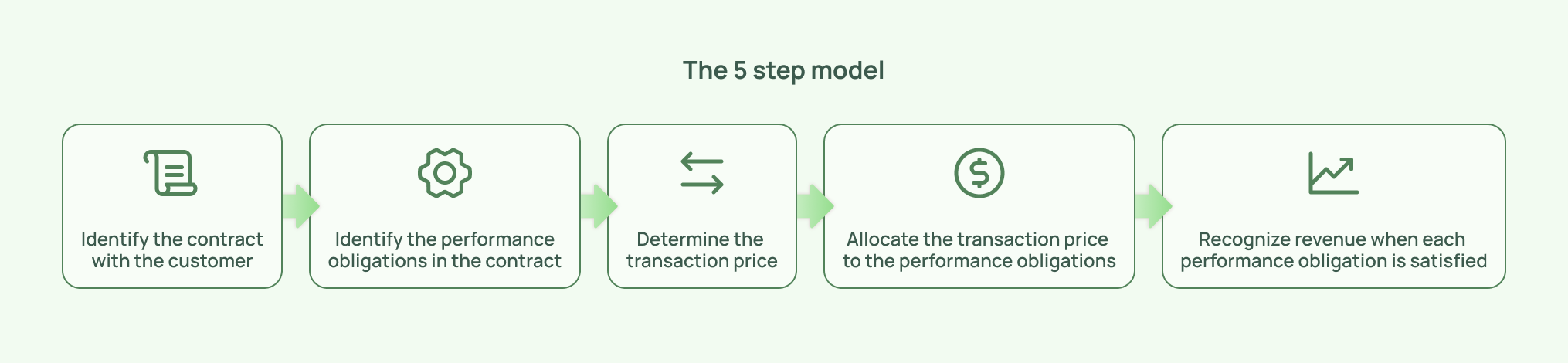

ASC 606 uses a five-step model:

Step 1: Identify the contract with the customer. A contract exists when both parties have approved it, each party's rights and payment terms are identifiable, the contract has commercial substance, and it is probable that you will collect the consideration.

Step 2: Identify the performance obligations in the contract. A performance obligation is a promise to transfer a distinct good or service to the customer. If a single contract includes multiple services that are distinct from each other, they are treated as separate performance obligations with their own recognition timing.

Step 3: Determine the transaction price. This is the total consideration you expect to receive in exchange for fulfilling your obligations. Variable consideration, such as usage-based fees, volume discounts, or success-based bonuses, must be estimated and included if it is probable that a significant revenue reversal will not occur.

Step 4: Allocate the transaction price to the performance obligations. If a contract has multiple performance obligations, you allocate the transaction price based on the relative standalone selling price of each obligation.

Step 5: Recognize revenue when each performance obligation is satisfied. A performance obligation is satisfied when control of the promised good or service transfers to the customer. For services delivered over time, revenue is recognized over the service period. For products delivered at a point in time, revenue is recognized at the delivery date.

What this means for a SaaS startup in practice:

A 12-month subscription contract for $12,000 paid upfront has one performance obligation: providing access to the software over the subscription period. Revenue is recognized ratably at $1,000 per month as the service is delivered. The $12,000 received upfront is recorded as deferred revenue on the balance sheet and recognized into the income statement monthly.

If the same contract also includes a one-time onboarding service worth $2,000 as a standalone price, that is a separate performance obligation. The $2,000 is recognized when the onboarding is completed, while the remaining $10,000 is recognized monthly over the subscription term.

Getting revenue recognition wrong is one of the most expensive mistakes a startup can make. A SaaS startup that had been booking annual subscription payments as immediate revenue rather than spreading them over the service period faced six months of financial restatements and $150,000 in accounting fees when investors flagged the error during Series A diligence. Implementing ASC 606 correctly from the beginning eliminates this risk.

Step 4: Prepare the 4 core GAAP financial statements

A complete set of GAAP-compliant financial statements for a startup includes four statements. Producing only a profit and loss report, which many startups do in their early years, is not GAAP-compliant.

The balance sheet

The balance sheet presents your company's financial position at a specific point in time, typically the last day of the reporting period. It shows what the company owns (assets), what it owes (liabilities), and the residual interest of the owners (equity). The fundamental equation is: Assets equal Liabilities plus Equity.

Under GAAP, the balance sheet separates assets and liabilities into current and non-current categories. Current assets are expected to be converted to cash or used within 12 months. Non-current assets are held for longer periods. Current liabilities are obligations due within 12 months. Non-current liabilities are due beyond 12 months.

For a startup, the balance sheet commonly includes:

Current assets: cash and cash equivalents, accounts receivable net of any allowance for doubtful accounts, prepaid expenses, and any other current assets. Non-current assets: property and equipment net of accumulated depreciation, capitalized software costs net of amortization, security deposits, and intangible assets.

Current liabilities: accounts payable, accrued compensation (salaries and benefits earned but not yet paid), other accrued liabilities, deferred revenue (current portion), and current debt. Non-current liabilities: deferred revenue (non-current), long-term debt, and other long-term obligations.

Equity: common stock at par value, additional paid-in capital (which captures the premium over par value for all stock issuances), and accumulated deficit (since most startups are loss-making in early years, equity is presented as a deficit rather than retained earnings).

The income statement

The income statement reports revenue, expenses, and net income or loss for a specific period, such as a quarter or a year. It begins with revenue, deducts cost of revenue to arrive at gross profit, then deducts operating expenses to arrive at operating income or loss, and finally accounts for interest and other non-operating items to arrive at net income or loss.

For GAAP compliance, expenses must be classified correctly. Cost of revenue includes direct costs of delivering the product or service, such as hosting costs, customer support salaries, and third-party software fees that are directly tied to delivering the product. Research and development expenses include costs of developing new features or products. Sales and marketing includes customer acquisition costs. General and administrative includes finance, legal, and executive costs.

Depreciation and amortization appear within the relevant expense categories rather than as a separate line item on the income statement for most startups, though they are disclosed separately in the footnotes.

The cash flow statement

The cash flow statement reconciles the change in your cash balance during the period across three categories of activity: operating, investing, and financing.

Operating activities capture the cash generated or consumed by your core business operations. The indirect method, which most startups use, starts with net income and adjusts for non-cash items (depreciation, amortization, stock-based compensation) and changes in working capital (accounts receivable, accounts payable, deferred revenue).

Investing activities capture cash used for capital expenditures, purchases of investments, or proceeds from asset sales.

Financing activities capture cash flows from issuing equity, borrowing, repaying debt, and paying dividends.

The cash flow statement is one of the most important documents investors review because it shows whether your business is actually generating or consuming cash independent of accounting choices. A company can show GAAP revenue and still be burning cash rapidly, and the cash flow statement makes that visible.

The statement of stockholders' equity

This statement reconciles the changes in your equity accounts from the beginning to the end of the period. It shows the opening balance for each equity component, adds contributions (stock issuances, exercise of options), adds or subtracts net income or loss, and arrives at the ending balance.

For startups, the primary movements in this statement are: new share issuances (both common and preferred), stock-based compensation expense recognized during the period, and net loss for the period. Each funding round will show up as an increase in common or preferred stock and additional paid-in capital.

Step 5: Write the footnote disclosures

Footnote disclosures are a required component of GAAP-compliant financial statements. They provide context, detail, and transparency that the four core statements alone cannot convey. Many founders view footnotes as a formality, but investors and auditors rely on them heavily.

The minimum footnotes a startup should include are:

Note 1: Summary of significant accounting policies. This is the most important footnote. It describes your basis of presentation (GAAP, accrual basis), your revenue recognition policy under ASC 606, your policy for research and development costs, your depreciation methods and useful lives for each asset class, and your policy for stock-based compensation.

Note 2: Going concern. If there is substantial doubt about your ability to continue as a going concern, typically because your cash runway is less than 12 months, GAAP requires you to disclose this. Investors know this is common for early-stage startups, but the absence of the disclosure when doubt exists is a red flag in audit.

Note 3: Revenue breakdown. A disaggregation of revenue by product type, geography, or customer segment as required by ASC 606. This shows investors where your revenue is coming from and how it is growing.

Note 4: Property and equipment. A table showing the gross cost and accumulated depreciation for each category of fixed asset, and the net book value.

Note 5: Debt and equity. A summary of any outstanding loans, convertible notes, or SAFE agreements, including the key terms. If SAFEs or convertible notes are outstanding, investors and auditors will want to understand how they are classified (as debt or equity) on the balance sheet and what the conversion terms are.

Note 6: Stock-based compensation. A summary of your stock option plan, including the total options authorized, granted, exercised, and forfeited, the weighted average exercise price, and the expense recognized during the period. Stock-based compensation under ASC 718 must be estimated using an option pricing model such as Black-Scholes.

Note 7: Subsequent events. Any material events that occurred after the balance sheet date but before the financial statements were issued. This commonly includes funding rounds that closed after the period ends.

The most common GAAP mistakes startups make in their first set of statements

Booking all upfront payments as immediate revenue: This is the most common and most expensive error. Any contract where services are delivered over time requires deferred revenue treatment under ASC 606. The entire upfront payment does not belong in revenue on day one.

Not recording stock-based compensation expenses: Founders often treat option grants as free, but under ASC 718, you must estimate the fair value of each option grant and expense it over the vesting period. Ignoring this understates expenses and overstates operating profit.

Misclassifying expenses between COGS and operating expenses: Hosting costs, customer success salaries, and third-party tools that directly support product delivery belong in cost of revenue. Finance, legal, and HR costs belong in G&A. Mixing these distorts gross margin, which is one of the most scrutinized metrics in a fundraise.

Not recording accounts receivable and accounts payable: Startups that switch to accrual accounting sometimes still only record transactions when cash moves. Every invoice sent to a customer that has not been paid creates accounts receivable. Every vendor bill received but not yet paid creates accounts payable.

Missing the deferred revenue calculation: If you have annual or multi-year contracts, you need a deferred revenue schedule that tracks the recognized and unrecognized portions for every active contract. This is not something you can reconstruct at year-end without tracking it monthly.

When does a startup need GAAP-Compliant financial statements?

GAAP compliance is not legally required for most private startups, but investors often expect GAAP-compliant financials once you are raising institutional funding or preparing for due diligence.

The practical triggers are:

Before a Series A or any priced institutional round. Most institutional investors will request GAAP-compliant financials as part of due diligence. If your books are on cash basis or your revenue recognition is wrong, you will need to restate before closing. Restating is expensive and creates friction.

Before a bank loan or venture debt. Lenders require accrual-based financials to assess your creditworthiness. A cash basis income statement does not give them the information they need.

Before an acquisition or M&A process. Any acquirer will conduct financial due diligence. GAAP compliance is table stakes.

If your gross receipts exceed $32 million. Per IRS Revenue Procedure 2025-32, for tax years beginning in 2026, businesses with average annual gross receipts exceeding $32 million over the prior three tax years are required to use the accrual method for tax purposes. At this stage, GAAP compliance and tax compliance converge significantly.

Before an audit. If any stakeholder requests audited financial statements, those statements must be GAAP-compliant. Auditors cannot express an unqualified opinion on statements that are not prepared in accordance with GAAP.

What does this mean for India-US founders?

If you are an Indian founder with a Delaware C-Corp and an Indian subsidiary, GAAP applies to your US entity's financial statements. Your Indian subsidiary's statutory financial statements are prepared under Indian Accounting Standards (Ind AS) or Companies Act requirements, not US GAAP.

The key issue for multi-entity India-US structures is consolidation. If you prepare consolidated financial statements that include both the US parent and the Indian subsidiary, the Indian subsidiary's financials must be converted to US GAAP before consolidation. This requires identifying and adjusting for any differences between Ind AS and US GAAP in areas like revenue recognition, lease accounting, and R&D capitalization.

Transfer pricing documentation between your US entity and Indian subsidiary affects how intercompany transactions appear on each entity's standalone statements and on the consolidated statements. Revenue earned by the Indian entity from services provided to the US parent, for example, needs to reflect arm's length pricing, and that pricing directly affects how much revenue and profit appear on each entity's standalone GAAP statements.

Getting your books GAAP-compliant before a fundraise is significantly cheaper and faster than restating them during one. Book a demo with Inkle to see how Inkle's bookkeeping and tax team builds investor-ready, GAAP-compliant financial statements for India-US startups from seed stage through Series A and beyond.

Frequently Asked Questions

Do early-stage startups need to be GAAP-compliant from day one?

Not fully, but sooner is much better than later. Most pre-seed and seed-stage startups cannot justify the cost of full GAAP compliance, and institutional investors at that stage generally understand this. What they do expect, even at seed stage, is accrual-based bookkeeping, consistent financial reporting, and correct revenue recognition if you have recurring revenue contracts. The full package of four financial statements with footnote disclosures typically becomes expected at Series A. The problem with waiting is that restating two or three years of financial history to GAAP standards during a fundraise can cost six figures in accounting fees and delay a closing by months. Building toward GAAP from the beginning, even if you are not fully compliant yet, is a far lower-cost path.

What is the difference between accrual accounting and GAAP-compliant financial statements?

Accrual accounting is a prerequisite for GAAP compliance, but it is not the same thing. A company using accrual accounting records transactions when they are earned or incurred rather than when cash moves. GAAP-compliant financial statements go further: they require correct revenue recognition under ASC 606, correct expense classification, proper balance sheet categorization of assets and liabilities as current and non-current, a complete set of four financial statements, and footnote disclosures explaining your accounting policies. A company can use accrual accounting and still have financial statements that are not GAAP-compliant if the revenue recognition, expense classification, or disclosure requirements are not met.

What is ASC 606 and why does it matter for my startup?

ASC 606 is the FASB standard that governs revenue recognition for all US companies. It requires you to recognize revenue based on when performance obligations in a customer contract are satisfied, not when cash is received. For most SaaS and software startups, this means annual or multi-year subscription payments received upfront cannot be recognized as revenue immediately. The payment must be spread across the service period and recorded as deferred revenue on the balance sheet until it is earned. Getting ASC 606 wrong is one of the most common reasons startups have to restate their financials during due diligence. If you have recurring revenue contracts, verifying your revenue recognition against ASC 606 before you begin fundraising is essential.

How do I know if my startup's books are GAAP-compliant?

The best way is to have a CPA review your financials against the GAAP requirements for your specific business model. A GAAP readiness review typically covers whether your books are on accrual basis, whether your revenue recognition is ASC 606-compliant, whether your balance sheet accounts are correctly classified and all required accounts are present, whether your four core financial statements have been prepared, and whether you have adequate footnote disclosures. Common signals that books are not GAAP-compliant include: all revenue is recognized at the time of payment regardless of contract terms, no deferred revenue account appears on the balance sheet despite subscription contracts, stock option grants have no associated compensation expense, and the financial package consists only of a profit and loss report without a balance sheet, cash flow statement, or footnotes.

In this article

.jpg)