The U.S. Startup Compliance Checklist (2026)

Most startup compliance problems don’t come from bad decisions—they come from deferred ones.

Founders are trained to move fast: ship product, close customers, raise capital. Compliance rarely feels urgent until it suddenly is—when a missed filing delays a fundraise, a payroll mistake triggers penalties, or due diligence turns into a cleanup project.

This guide is designed to prevent that outcome.

The U.S. Startup Compliance Checklist (2026) is a practical, systems-first framework for founders who want compliance handled quietly and correctly in the background. No legal theory. No edge cases. Just the recurring actions that keep your company in good standing, monthly, quarterly, and annually, so you stay investor-ready without losing focus on building.

If you want compliance to be boring, predictable, and off your mental load, this checklist is for you.

1. Why this checklist exists

Most founders do not think about compliance until something breaks.

It usually starts small: a missed filing, a delayed tax payment, an unclear cap table entry, or payroll set up incorrectly “for now.” The consequences rarely appear immediately. They surface months or years later—during a fundraise, an acquisition discussion, or an audit—when fixing past mistakes is slow, expensive, and distracting.

This checklist exists to give founders a clear, repeatable system to:

- Keep the company in good legal and tax standing

- Avoid penalties, notices, and last-minute fire drills

- Stay ready for investor diligence at any point

- Prevent compliance from becoming a recurring cognitive burden

This is not legal theory or edge-case analysis. It is a working checklist designed to be used monthly, quarterly, and annually.

2. Who this guide is for (and who it is not)

This guide is for startups that:

- Are incorporated as a U.S. LLC or Corporation

- Are operating now or planning to operate in 2026

- Do not have in-house legal or finance teams

It is especially relevant if you are:

- A first-time founder

- A non-U.S. founder entering the U.S. market

- A small team handling compliance alongside product, sales, and growth

This guide is not designed for:

- Public companies or pre-IPO entities

- Startups in heavily regulated industries (e.g., fintech, healthcare, defense)

- Companies with complex international tax structures or in-house counsel

If you fall outside this scope, many of the principles still apply, but the execution details will differ.

3. What “compliance” actually means for a U.S. startup

Compliance is not a single task or filing. It is the result of three systems working together.

1. Legal compliance

Your company exists and operates correctly.

- The entity is properly incorporated

- Ownership and equity are documented

- Core agreements are adopted

- Contracts are executed by the company, not individuals

2. Tax compliance

The right taxes are filed and paid, on time.

- Federal and state income taxes

- Payroll taxes

- Required information returns (e.g., 1099s)

3. Financial compliance

Your financial records match reality.

- Books reflect actual cash movement

- Bank, payroll, and accounting records reconcile

- Reports are accurate and defensible

When these three stay aligned, the startup stays compliant. When one breaks, the others usually follow.

4. Day 0 to Day 30: setting the foundation correctly

The first 30 days matter more than most founders realize. Decisions made here determine how difficult or easy, compliance will be later.

What typically happens in the first 30 days

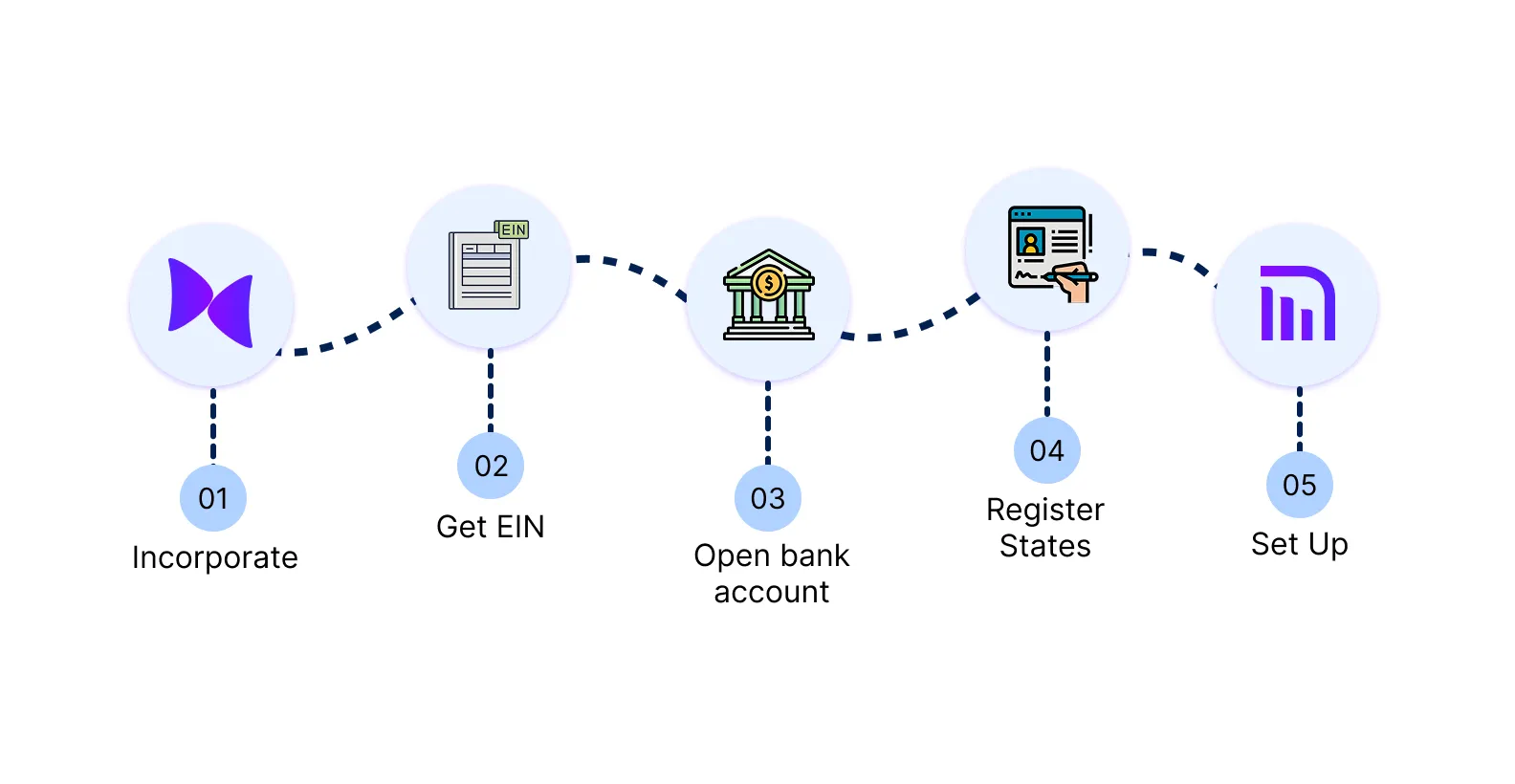

- Choose an entity type and incorporate

- Adopt core governance documents (bylaws or operating agreement)

- Apply for an EIN

- Open a business bank account

- Separate personal and business finances

- Register in the required states

- Set up basic bookkeeping Inkle has a free plan. Add Inkle books Nudge.

Depending on timing and structure, some startups may also need to:

- File initial state reports

- Register for payroll or sales tax accounts

Day 0–30 checklist

- Incorporate the company and adopt core documents

- Obtain an EIN

- Open a business bank account in the company’s name

- Register required state tax and business accounts

- Select an accounting system and record all expenses and invoices from day one

Mistakes made here rarely surface immediately. They usually appear during tax season, a fundraise, or a cleanup project—when fixes are more expensive and disruptive.

5. The monthly compliance checklist

Monthly routines prevent small issues from compounding.

Monthly checklist

- Close the books and reconcile all bank and card accounts

- Review cash balance, burn rate, and upcoming obligations

- Confirm payroll ran correctly and taxes were withheld

- Log any changes in ownership, addresses, employees, or business activity

Many founders fail here not because the work is complex, but because it is inconsistent. The goal is not sophistication—it is reliability.

6. The quarterly compliance checklist

Quarterly obligations are where most tax-related risk accumulates.

Quarterly checklist

- Review whether federal or state estimated tax payments are required and submit on time

- Reconcile payroll tax filings with amounts paid

- Review multi-state payroll and nexus exposure, if applicable

- Assess whether hiring, expansion, or revenue changes triggered new registrations

Quarter ends are also a natural checkpoint to reassess runway, hiring plans, and upcoming fundraising needs.

7. The annual compliance checklist

Annual tasks keep the entity clean and defensible under scrutiny.

Annual checklist

- File state annual reports and pay franchise or similar fees

- File federal and state income tax returns

- Issue required 1099 forms and reconcile W-2 filings

- Renew business licenses and confirm registered agent details

- Update corporate records, consents, and meeting minutes

If you have employees, this is also the point to:

- Review HR policies

- Confirm required postings and notices

- Complete any mandatory training

8. Founder-specific compliance mistakes to avoid

Most compliance failures come from a small set of repeat behaviors.

Common mistakes

- Mixing personal and business finances

- Taking money before formalizing the entity or cap table

- Ignoring payroll or state registrations until notices arrive

- Misclassifying contractors as employees

- Treating compliance as a once-a-year task

These mistakes are rarely intentional. They happen when founders move fast and push compliance aside. The cost is delayed—but real.

9. What’s changing in U.S. startup compliance in 2026

As of 2026, several trends continue to shape compliance expectations:

- Ongoing updates and clarifications around Corporate Transparency Act reporting

- Increased enforcement focus on payroll compliance and worker classification

- More states tightening privacy and data-handling rules, including for smaller SaaS and ecommerce companies

Founders do not need to master the law. They do need to know what applies to their startup, and when.

10. Doing it yourself vs. getting professional help

Most startups begin with a DIY approach and transition to professional support as complexity increases.

DIY makes sense when:

- The company is early-stage with a simple structure

- Operations are limited to one state

- Transaction volume is low

- Founders follow a disciplined checklist

Professional help becomes worth it when:

- The company operates in multiple states

- Employees are added

- A fundraise, acquisition, or audit is approaching

- Notices, penalties, or cleanup work have already occurred

Compliance work is unevenly distributed across the year. Deadlines cluster. Missing one often creates downstream issues.

To help founders plan, Inkle maintains a consolidated U.S. tax and compliance calendar covering common federal and state deadlines for 2026. Founders who align routines to a calendar are significantly less likely to miss filings or face penalties.

11. How Inkle helps U.S. startups stay compliant

Compliance breaks down when information is fragmented.

A bank account in one place. Books in another. Deadlines buried in inboxes. Filings remembered too late.

Inkle brings bookkeeping, tax readiness, and compliance tracking into a single system so founders can:

- Maintain accurate, current books

- Track federal and state deadlines across the year

- Keep records that investors and advisors expect during diligence

- Reduce reliance on manual reminders and ad-hoc processes

The objective is not to turn founders into tax experts. It is to ensure nothing critical is missed while they focus on building the company.

12. Final notes for founders

Compliance rarely kills a startup on its own. Ignoring it quietly builds risk.

Most problems come from:

- Waiting too long

- Assuming something does not apply yet

- Treating compliance as an annual event

Staying compliant does not require perfection or expensive advisors from day one. It requires consistency, basic awareness, and simple systems.

Founders who treat compliance as an operating discipline—not an afterthought, build companies that are easier to fund, scale, and exit.

Compliance, done well, does not slow you down. It removes friction so you can move forward with confidence.

In this article

.webp)