Form 1120 Late Filing Penalty and How Can Corporations Avoid It

Form 1120 is the annual federal income tax return that C corporations must file with the IRS to report income, deductions, and tax liability. Missing the filing deadline can lead to immediate consequences. The IRS may impose late filing penalties, interest charges, and additional compliance requirements that increase the administrative burden on finance teams.

For startups and growing companies, these penalties can also create unexpected cash flow pressure and trigger time-consuming follow-ups with tax authorities.

This guide answers those practical questions. It explains how the Form 1120 late filing penalty is calculated, when penalty relief may apply, and what corporations can do to avoid repeat compliance issues in future tax years.

Form 1120 Late Filing Penalty

Form 1120 late filing penalty applies when the return is submitted after the due date and no valid extension has been filed. Corporations often file late due to operational issues rather than intentional noncompliance. Delayed bookkeeping, confusion about whether an extension was filed, incomplete financial records, or internal approval delays can all push tax preparation past the deadline.

When the IRS identifies a late filing, it usually issues a notice explaining the penalty amount and requesting payment or clarification.

Key points corporations should keep in mind:

- Who needs to file Form 1120?: Most domestic C corporations operating in the United States must submit Form 1120 annually.

- When a late filing penalty may apply?: The penalty may apply when the corporation files its return after the due date without a valid extension.

- Why should corporations respond to IRS notices quickly?: Responding promptly helps prevent additional penalties, interest charges, or escalation of the issue.

How Does the IRS Calculate the Form 1120 Late Filing Penalty

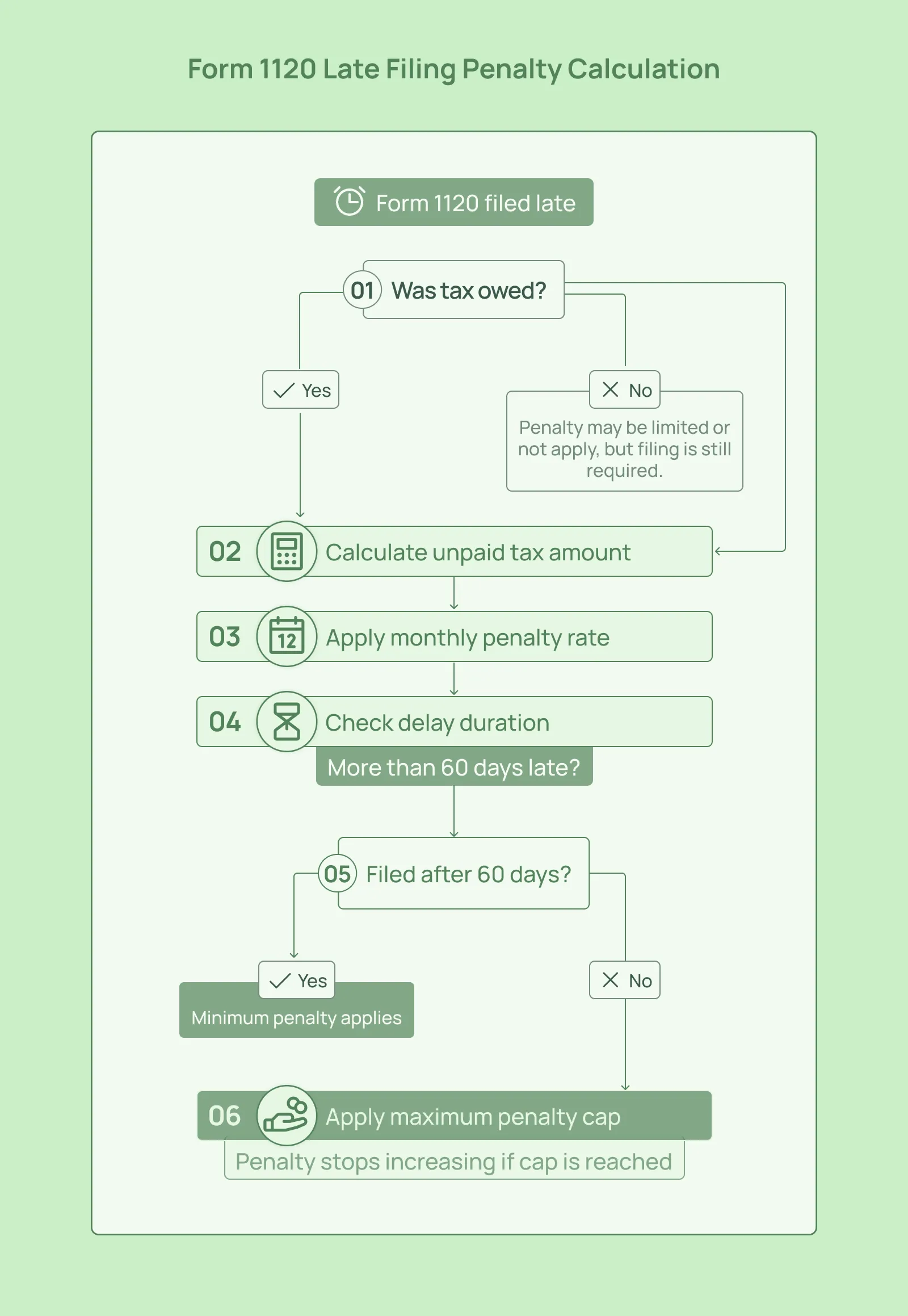

The IRS calculates the Form 1120 late filing penalty based on how long the return is delayed and whether the corporation owes unpaid tax. In most cases, the failure-to-file penalty increases the longer the return remains unfiled. This is why corporations should file the return as soon as possible, even if they cannot immediately pay the full tax amount.

The IRS generally applies a monthly penalty rate to the unpaid tax amount when a corporation files its return late. Each month that the return remains unfiled can increase the total penalty.

Key rules to remember include:

- The penalty is calculated based on the unpaid tax amount reported on the return.

- Each month or part of a month after the deadline counts toward the penalty calculation.

- The total failure-to-file penalty is capped, so it does not continue increasing indefinitely.

If a corporation files its tax return more than 60 days after the due date, the IRS may apply a minimum penalty amount. This minimum penalty ensures that significantly late returns still face a penalty even if the unpaid tax amount is relatively small.

How Is the Late Filing Penalty Different from the Late Payment Penalty

The IRS treats late filing and late payment as two separate compliance issues, and each has its own penalty structure. The late filing penalty applies when a corporation submits Form 1120 after the deadline. The late payment penalty applies when the corporation does not pay the tax owed by the due date. In some situations, both penalties can apply at the same time.

This distinction is important because corporations should still file their return on time even if they cannot pay the full tax amount immediately. Filing the return avoids the higher failure-to-file penalty. The corporation can then work with the IRS to address the remaining balance through payment plans or other arrangements.

Late Filing Penalty vs Late Payment Penalty:-

Can a Corporation Face a Penalty If It Owes No Tax?

Many founders assume that if their corporation owes no tax, missing the Form 1120 deadline will not lead to penalties. In reality, the IRS still expects corporations to file their tax return on time even when there is little or no tax liability. Filing requirements are tied to the corporation’s legal status, not just the amount of tax owed.

For example, early-stage startups or inactive corporations may report minimal revenue or losses during the year. Even in these situations, the IRS still requires the return to be filed so that the company’s financial activity and tax position are formally recorded. Ignoring the filing obligation can still trigger notices or compliance issues.

Key reminders for corporations include:

- Filing obligations still apply even with minimal activity. The IRS expects corporations to submit Form 1120 each year unless the entity has been formally dissolved.

- Deadlines should not be ignored simply because no tax is owed. Filing late can still lead to IRS correspondence and additional administrative work.

- IRS notices should always be reviewed carefully. Responding quickly helps prevent escalation and ensures the issue is resolved before additional penalties or compliance actions occur.

What Are the Form 1120 Deadlines and How Do Extensions Work

One of the simplest ways to avoid the Form 1120 late filing penalty is to clearly understand when the corporate tax return is due. Many late filings occur because corporations lose track of deadlines or misunderstand how fiscal year timelines work. Knowing the correct due date and using extensions when needed can prevent unnecessary penalties.

The filing deadline depends on whether the corporation follows a calendar tax year or a fiscal year. Most startups use a calendar year, which means their corporate tax return is due in April of the following year. Corporations that operate on a fiscal year must calculate their deadline based on the end of their accounting period.

Key deadlines include:

- Calendar-year corporations: Form 1120 is generally due on April 15.

- Fiscal-year corporations: The return is due on the 15th day of the fourth month after the end of the tax year.

Corporations that need additional time to prepare their return can file Form 7004, which provides an automatic extension to submit Form 1120. This extension gives companies extra time to finalize financial records, review deductions, and complete supporting schedules.

However, it is important to understand that Form 7004 only extends the filing deadline, not the tax payment deadline. Corporations must still estimate their tax liability and pay any taxes owed by the original due date. If taxes remain unpaid, the IRS may apply interest or late payment penalties even if the return itself is filed within the extension period.

Here’s how Form 1120 filing timeline looks like:-

This timeline helps clarify a few common misunderstandings:

- Filing and payment deadlines are not the same.

- Form 7004 extends the filing deadline but not the tax payment deadline.

- Filing late without an extension is what usually triggers the failure-to-file penalty.

When Can a Corporation Request Form 1120 Penalty Relief

Receiving an IRS penalty notice does not always mean the penalty must be paid immediately. In certain situations, corporations may request relief from the Form 1120 late filing penalty. The IRS evaluates these requests based on the reason for the delay, the company’s compliance history, and the documentation provided to support the request.

Corporations that act quickly after receiving an IRS notice often have better chances of resolving the issue. Understanding the types of relief available and preparing a clear explanation of what caused the delay can help finance teams respond more effectively.

The IRS may waive penalties when a corporation can demonstrate that the late filing occurred due to reasonable cause rather than willful neglect. Reasonable cause generally refers to situations where the corporation exercised ordinary care but still could not meet the filing deadline.

Examples that may support a reasonable cause request include:

- Unexpected events outside the corporation’s control

- Situations where documentation shows the company attempted to comply on time

- Evidence explaining the timeline that led to the delay

- Clear records demonstrating that the issue has been corrected

Can a Corporation Qualify for First-Time Penalty Abatement

Corporations with a clean compliance history may qualify for First Time Penalty Abatement (FTA). This IRS program allows certain taxpayers to request penalty relief if they have filed and paid their taxes on time in prior years. If the corporation meets the eligibility criteria, the IRS may remove the late filing penalty for the affected tax year.

How Should a Corporation Request Penalty Relief

Corporations typically request penalty relief by responding directly to the IRS notice that explains the penalty. The response should clearly describe the reason for the delay and include documentation that supports the explanation. In some cases, corporations may submit a written request or work with a tax advisor to prepare a formal penalty abatement request.

Preparing a clear explanation and organizing supporting documents can help the IRS review the request more efficiently and improve the chances of a favorable outcome.

Here’s what to gather before requesting penalty relief:

- IRS notice describing the penalty

- Corporate filing history for prior tax years

- A timeline explaining why the filing delay occurred

- Supporting documentation such as internal records or correspondence

- Payment records related to the tax return

What Steps Help Corporations Avoid Form 1120 Penalties in the Future

Avoiding Form 1120 late filing penalties usually comes down to strong internal processes and consistent bookkeeping. Many corporations miss deadlines not because the tax rules are unclear, but because financial records are incomplete or the tax preparation process starts too late. When companies close their books earlier and track compliance deadlines carefully, the risk of late filing drops significantly.

Another key factor is having organized financial documentation before tax season begins. When income records, expense data, and financial statements are already prepared, accountants and finance teams can complete the corporate tax return without rushing near the deadline. This reduces errors, avoids last-minute confusion about extensions, and ensures that both filing and payment obligations are handled properly.

Practical steps corporations can take include:

- Maintain a clear tax compliance calendar with all filing deadlines

- Close financial books well before the corporate tax filing date

- Plan extension filings and tax payment estimates separately

- Track confirmation of submitted filings and IRS acknowledgments

- Work with experienced tax advisors who monitor corporate compliance

How Can Inkle Help You Avoid 1120 Late Filing Penalties

Staying compliant with IRS filing deadlines starts with accurate and organized financial records. When bookkeeping is inconsistent or financial data is scattered across systems, preparing corporate tax returns becomes slower and more error-prone. Platforms like Inkle help startups maintain structured financial records so that tax preparation begins with reliable data rather than last-minute reconciliation.

Inkle supports founders and finance teams by keeping bookkeeping current and improving visibility into compliance timelines. When financial statements, transaction records, and supporting documentation are maintained throughout the year, corporations are better prepared for tax filings and far less likely to miss important deadlines.

Inkle helps corporations:

- Keep bookkeeping updated so tax preparation starts with accurate financial records

- Track compliance requirements across different geolocations

- Reduce manual follow-ups during tax season

- Provide clearer visibility into filing readiness and documentation status

See how Inkle simplifies compliance and bookkeeping for global startups. Book a demo to learn how your team can stay ahead of IRS deadlines and reduce corporate tax filing risks.

Frequently Asked Questions

What is the Form 1120 late filing penalty for corporations

The Form 1120 late filing penalty is an IRS failure-to-file penalty applied when a corporation submits its tax return after the filing deadline without a valid extension. The penalty generally increases the longer the return remains unfiled, especially if the corporation also owes unpaid taxes.

How does the IRS calculate the failure to file penalty for a corporation

The IRS usually calculates the penalty as a monthly percentage of the unpaid tax. Each month or part of a month after the deadline counts toward the penalty calculation. The penalty is capped once it reaches a defined maximum percentage of the unpaid tax.

Is there a Form 1120 late filing penalty if no tax is due

In many cases, the failure-to-file penalty is based on unpaid tax. If no tax is owed, the penalty may not apply in the same way. However, corporations are still required to file Form 1120 annually, and ignoring the filing requirement can lead to IRS notices or additional compliance issues.

Does Form 7004 remove the Form 1120 late filing penalty

Form 7004 does not remove a penalty that has already occurred. However, filing Form 7004 before the original deadline provides an automatic extension to file Form 1120. This extension helps corporations avoid the late filing penalty as long as the return is submitted by the extended deadline.

Can a corporation get penalty relief for filing Form 1120 late

Yes. Corporations may request penalty relief if they can show reasonable cause for the delay or if they qualify for the IRS First-Time Penalty Abatement program. The IRS reviews these requests based on compliance history and supporting documentation.

What documents help support a reasonable cause request

Corporations requesting penalty relief should gather documentation that explains why the filing delay occurred. This may include IRS notices, internal timelines showing the cause of the delay, prior filing history, correspondence related to the issue, and payment records.

How can corporations avoid Form 1120 late filing penalties in future years

Corporations can reduce the risk of penalties by maintaining organized bookkeeping throughout the year, using a compliance calendar to track deadlines, and starting tax preparation early. Filing extensions when needed and confirming that returns have been successfully submitted can also help prevent repeat issues.

In this article