How Do You Handle Filing Form 1120 for a C Corporation

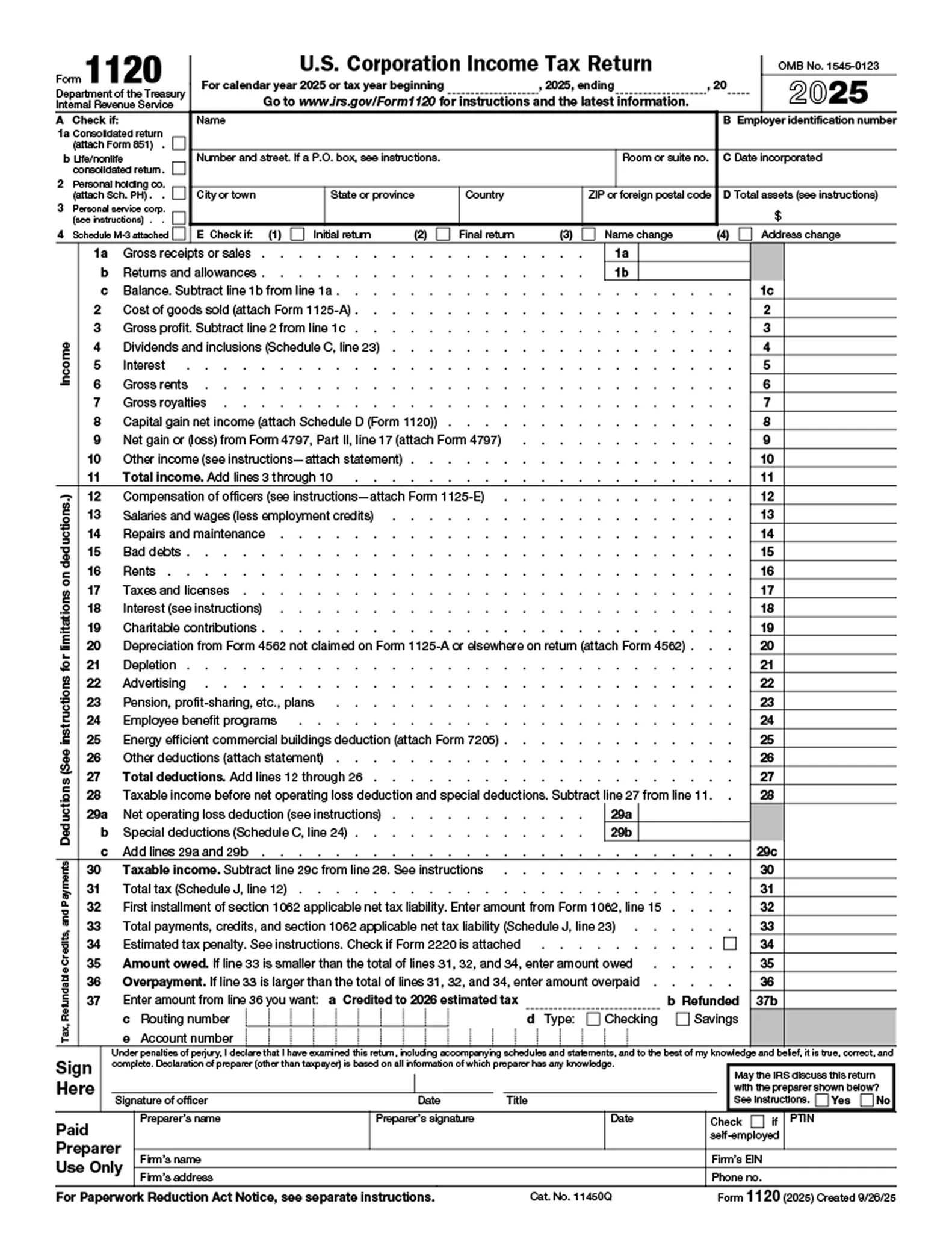

Every C corporation in the United States must file Form 1120 to report its annual income, deductions, and tax liability to the IRS. This form functions as the primary federal corporate income tax return and applies to both large enterprises and newly incorporated startups. Even if a corporation generates no taxable income during the year, the IRS still expects the return to be filed to document the company’s financial activity and tax position.

Missing schedules, incorrect classifications, or late 1120 filings can trigger penalties and IRS notices. According to IRS enforcement data, filing errors and incomplete returns remain one of the most common reasons businesses receive compliance notices each year.

When financial data such as income, expenses, and balance sheet records are organized throughout the year, preparing Form 1120 becomes significantly easier. Modern accounting platforms and automated bookkeeping systems help businesses maintain clean records, reduce reporting errors, and stay ready for corporate tax-filing obligations across US and international operations.

This structure follows the educational and solution-oriented approach recommended for Inkle content, where guides combine practical explanations with actionable steps for founders managing compliance.

Who Must File Form 1120 for a Corporation

All domestic C corporations registered in the United States must file Form 1120 each year. The IRS requires this filing regardless of whether the company generated profit during the tax year. The purpose of the return is to report corporate income, claim deductions, calculate tax liability, and disclose key financial information that supports the corporation’s tax position.

Many founders assume filing is only required when a company becomes profitable. That is incorrect. Even early-stage startups or companies with minimal activity must submit Form 1120 if they are legally structured as C corporations. Filing ensures the IRS has a record of the corporation’s financial activity and confirms that the entity remains compliant with federal tax rules.

Corporations that must file Form 1120 include:

- Domestic C corporations registered in the United States

- Corporations that report taxable income or deductible expenses

- Companies with business operations but no profit during the year

- Newly formed corporations during their first tax year

- Inactive corporations that remain legally registered with the state

When Is the Corporate Tax Return Due

The IRS requires corporations to file Form 1120 by the 15th day of the fourth month after the end of the corporation’s tax year. For most companies that follow a calendar year accounting period, this places the filing deadline on April 15 each year. By this date, the corporation must submit its completed tax return and pay any taxes owed.

Some corporations use a fiscal year that ends in a month other than December. In these cases, the filing deadline shifts accordingly. For example, if a company’s fiscal year ends on June 30, its corporate tax return would be due on October 15. Understanding which tax year structure your corporation follows is important to avoid missed deadlines and late filing penalties.

Here’s a quick overview of corporate filing deadlines:-

How Can Corporations Request More Time Using Form 7004

Corporations that need more time to prepare their tax return can request an automatic six-month extension by filing Form 7004 with the IRS. This form allows companies to extend the deadline for submitting Form 1120 without providing a detailed explanation. Many businesses use this extension when financial statements are still being finalized or when additional time is needed to review deductions and supporting schedules.

.webp)

It is important to note that Form 7004 only extends the filing deadline, not the tax payment deadline. Corporations must still estimate their tax liability and pay any expected taxes by the original due date. If the estimated payment is too low or not made on time, the IRS may apply interest and penalties even if the return itself is filed within the extension period.

Key rules when requesting an extension include:

- File Form 7004 before the original corporate tax filing deadline

- Estimate the corporation’s total tax liability for the year

- Pay any expected tax due when submitting the extension request

- Maintain documentation that supports the estimated tax calculation

Difference Between Form 1120 and Form 1120S

Form 1120 and Form 1120S are both corporate tax returns, but they apply to different types of business structures. Form 1120 is used by C corporations, which pay federal income tax at the corporate level. Form 1120 S is used by S corporations, where income and losses pass through directly to shareholders and are reported on their individual tax returns. Because of this difference, the tax treatment and reporting obligations vary between the two entity types.

Key Differences Between Form 1120 and Form 1120S

What Financial Documents Are Required Before Filing Form 1120

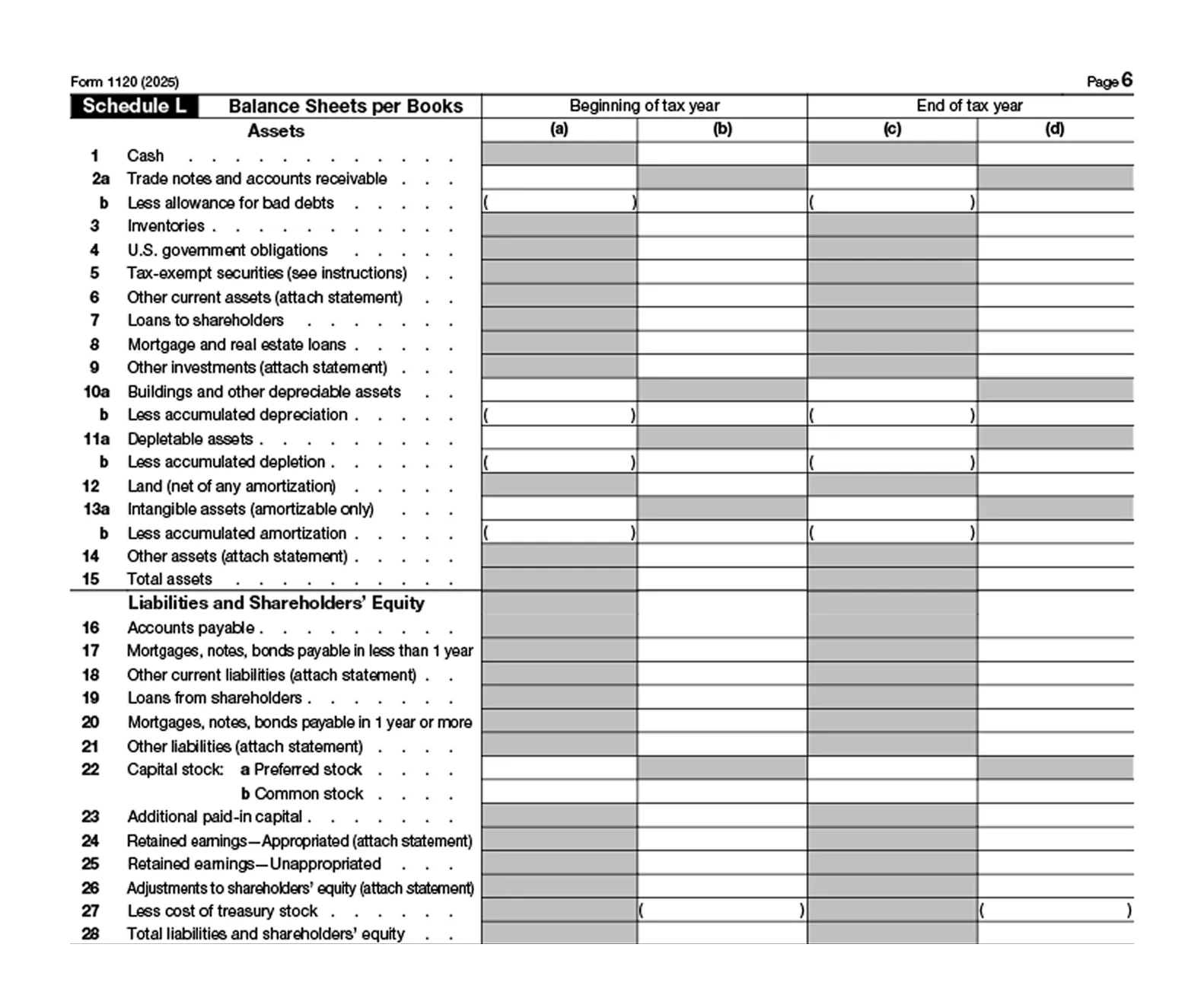

The IRS requires corporations to report income, deductions, and balance sheet positions using verifiable accounting data. If records are incomplete or inconsistent, the corporate return may not reconcile properly with supporting schedules such as Schedule L or Schedule M-1.

This is why most corporations finalize their financial statements before starting the tax return. These documents provide the numbers that populate different sections of Form 1120 and help accountants verify that book income aligns with taxable income. Clean financial records also make it easier to defend deductions if the IRS requests clarification later.

Key documents typically required before filing include:

i) Profit and Loss Statement (Income Statement)

This report summarizes revenue, operating expenses, and net profit for the year. It forms the basis for calculating the corporation’s gross income and deductible expenses reported on Form 1120.

ii) Balance Sheet

The balance sheet lists the company’s assets, liabilities, and shareholder equity at the end of the tax year. These numbers are required for Schedule L, which reports the corporation’s financial position to the IRS.

iii) Cost of Goods Sold Records

Businesses that sell products must track inventory purchases, production costs, and ending inventory. These records determine the cost of goods sold deduction, which directly affects taxable income.

iv) Payroll and Operating Expense Records

Salary payments, contractor fees, rent, utilities, and other operating costs are often deductible. Accurate records ensure the corporation claims the correct deductions without overstating expenses.

v) Depreciation Schedules

When companies purchase equipment, software, or other assets, the cost is usually deducted over time through depreciation. A depreciation schedule tracks asset value and allowable deductions each year.

vi) Prior Year Tax Returns

Previous returns help verify carryforward items such as net operating losses, retained earnings adjustments, or tax credits. They also help ensure consistency in reporting between tax years.

Process to Complete the Major Sections of Form 1120

Form 1120 is structured to help the IRS review a corporation’s identity, income, deductions, and final tax liability. Each section pulls information from the company’s financial statements and supporting schedules.

Although the form may appear long, most corporations complete it by working through a few core sections in sequence. These sections establish the company’s identity, calculate gross income, apply allowable deductions, and determine the final tax due after credits and estimated payments.

1. Report Corporate Information

The first section of Form 1120 captures basic identifying information about the corporation. This includes the legal name of the business, its Employer Identification Number (EIN), and the date the company was incorporated. Corporations must also report their principal business activity using a specific IRS activity code. These details allow the IRS to match the return with the correct legal entity and understand the nature of the company’s operations.

2. Calculate Corporate Gross Income

The income section reports the total revenue earned during the tax year. Corporations must include income from all sources, not just their primary line of business. This often includes operating revenue from products or services, interest earned on financial accounts, and gains from selling company assets. These amounts are combined to determine the corporation’s total gross income before deductions are applied.

3. Claim Corporate Tax Deductions

After income is reported, corporations subtract ordinary and necessary business expenses to determine taxable income. These deductions typically include employee salaries and benefits, rent and office expenses, depreciation on business assets, and professional service costs such as legal or accounting fees. Accurate expense tracking is important here because deductions directly reduce the corporation’s taxable profit.

4. Calculate Tax Liability and Credits

The final section calculates the corporation’s tax liability. The IRS applies the corporate tax rate to taxable income after deductions. Corporations can then reduce this liability by applying eligible tax credits and subtracting estimated tax payments already made during the year. The result determines whether the company must pay additional tax or is entitled to a refund.

Form 1120 Schedules

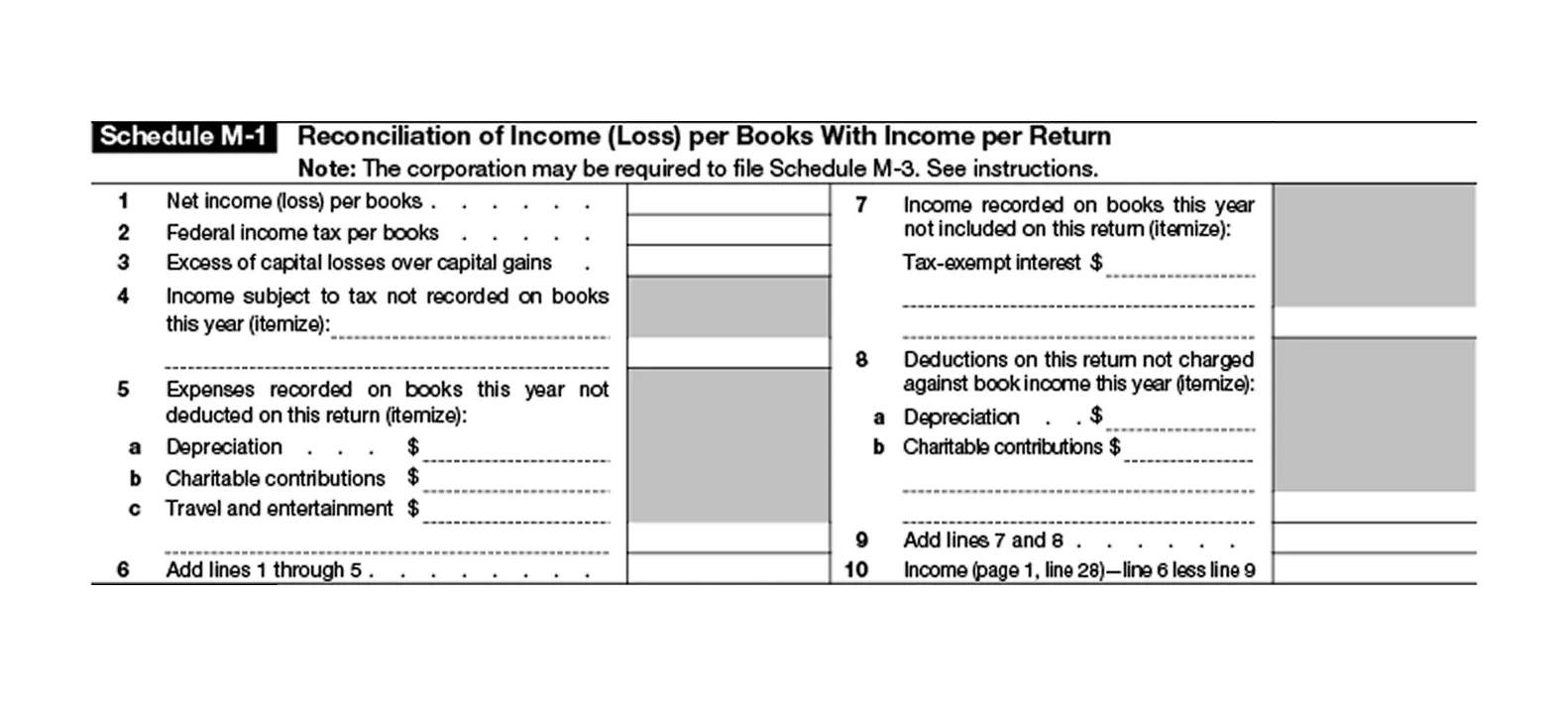

Form 1120 often requires additional schedules that provide deeper financial detail beyond the main tax return. These schedules help the IRS verify that the numbers reported in the corporate tax return aligns with the company’s financial statements and accounting records. They also provide transparency around how profits, retained earnings, and balance sheet changes occur during the year.

For many corporations, these schedules act as a bridge between bookkeeping data and tax reporting. Accounting systems track financial activity throughout the year, while the schedules reconcile that data to the tax rules used by the IRS. Preparing these schedules correctly helps reduce inconsistencies between book income and taxable income.

Here’s a quick overview of key Form 1120 schedules

Now, let’s cover these schedules in detail:-

i) Schedule L

Schedule L presents the corporation’s balance sheet, including assets, liabilities, and shareholder equity at the beginning and end of the tax year. This helps the IRS assess whether the company’s reported income aligns with its financial position.

ii) Schedule M-1

Schedule M-1 reconciles the difference between accounting profit and taxable income. Some expenses allowed in accounting may not be deductible for tax purposes, while some tax deductions may not appear in financial statements. This schedule explains those adjustments.

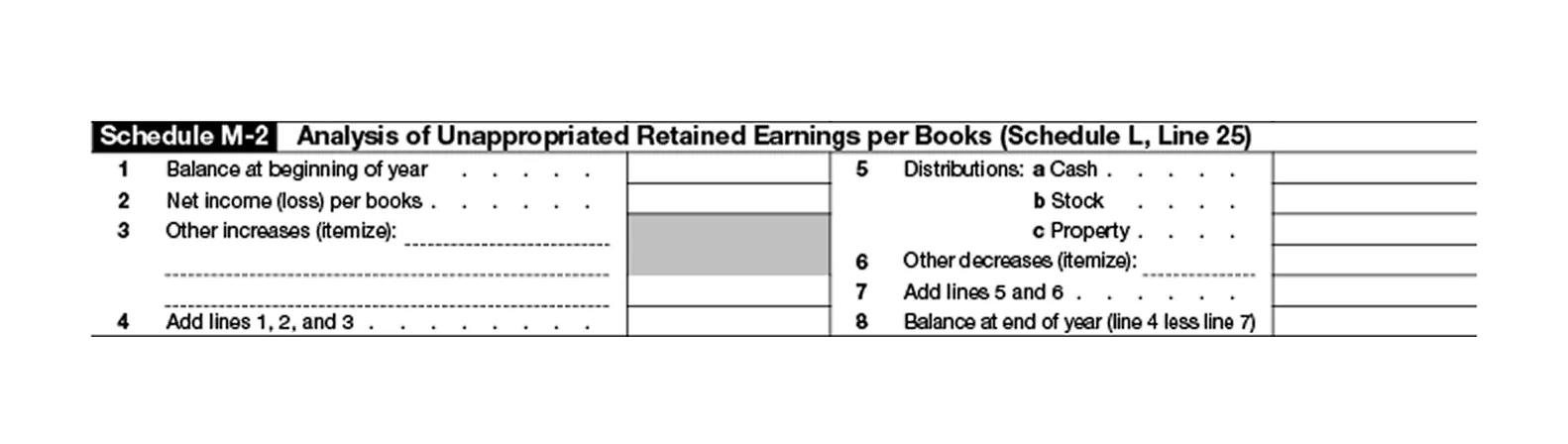

iii) Schedule M-2

Schedule M-2 tracks changes in retained earnings across the year. It shows how profits, losses, dividends, and other adjustments affect the corporation’s accumulated earnings. This information helps the IRS understand how income is retained or distributed within the company.

Penalties for Late Filing or Payment

The IRS imposes penalties when corporations fail to file Form 1120 on time or do not pay their taxes by the deadline. These penalties are designed to encourage timely reporting and accurate tax payments. Even if a corporation eventually files the return, delays can increase the total amount owed through penalties and interest.

Filing an extension with Form 7004 can prevent late filing penalties, but taxes owed must still be paid by the original deadline.

Common penalties corporations may face include:

- Late filing penalty per month if the tax return is submitted after the deadline

- Interest charges on unpaid taxes until the balance is fully paid

- Accuracy related penalties when the IRS finds incorrect reporting or underpayment

- Additional enforcement actions if a company repeatedly fails to comply with filing requirements

How Inkle Helps Founders Stay Compliant with Corporate Tax Filing

Inkle supports founders by maintaining accurate financial records and preparing the financial data needed for corporate tax filings. Instead of assembling documents manually at year end, businesses can rely on automated bookkeeping and structured reporting to keep their financial data tax-ready. This approach reduces reporting errors and helps ensure corporate tax returns align with underlying accounting records.

Inkle helps founders:

- Maintain organized financial records required for corporate tax filing

- Track income and expenses automatically through structured bookkeeping

- Generate financial statements needed to prepare Form 1120

- Manage compliance for US entities and cross-border startup operations

Schedule a demo with Inkle to see how automated bookkeeping, structured reporting, and compliance tracking can simplify corporate tax preparation for your startup.

Frequently Asked Questions

Who must file Form 1120 for a corporation

All domestic C corporations must file Form 1120 each year. This requirement applies even if the corporation has no taxable income. Filing ensures the IRS receives a record of the company’s financial activity and confirms the corporation remains compliant with federal tax rules.

When is Form 1120 due each year

For corporations that follow a calendar year, Form 1120 is due on April 15. Corporations that use a fiscal year must file their return by the 15th day of the fourth month after the end of their tax year.

Can a corporation request an extension for Form 1120

Yes. Corporations can request an automatic six month extension by filing Form 7004 before the original tax deadline. However, the extension only applies to filing the return. Any taxes owed must still be paid by the original due date.

What records should a company prepare before filing Form 1120

Companies should prepare financial statements such as the profit and loss statement, balance sheet, expense records, and depreciation schedules. Prior year tax returns are also useful because they help verify carryforward items and maintain consistency between tax years.

What happens if a corporation files Form 1120 late

If a corporation files late, the IRS may apply monthly penalties and interest on unpaid taxes. The longer the delay continues, the more the penalty amount can increase. Repeated noncompliance may also trigger additional IRS scrutiny.

How can startups simplify corporate tax compliance

Startups can simplify corporate tax compliance by maintaining organized bookkeeping throughout the year. Automated financial tracking and structured reporting help ensure financial statements are ready when it is time to prepare the corporate tax return.

In this article