Cash vs Accrual Accounting: Which Method Should Startups Use?

The first goal of early startups is usually simple: track money coming in, track money going out, and make sure there is enough cash in the bank to keep building. That is why many founders begin with cash-basis accounting. It is easy to follow because revenue is recorded when cash is received, and expenses are recorded when cash is paid.

But as the business grows, that simplicity can start hiding important details. A startup may have invoices sent but not yet collected, vendor bills received but not yet paid, annual subscriptions collected upfront, or costs that belong to one month but are paid in another.

At that point, cash-basis books may not show what the company has earned, what it owes, or how the business is really performing. Accrual accounting solves this by recording revenue when it is earned and expenses when they are incurred, even if cash moves later.

Here is a simple example. A SaaS startup sends a customer invoice in March, receives payment in April, and pays March hosting costs in the same month. Under cash accounting, March may show the hosting expense but no revenue. Under accrual accounting, March shows both the revenue earned and the cost connected to delivering that service. That difference can change how founders read profitability, runway, month-end reports, and investor updates.

For early-stage startups, cash accounting may work well at the start. But once revenue, expenses, funding, compliance, or cross-border operations become more serious, accrual accounting often becomes the cleaner choice.

What Is Cash-Basis Accounting?

Cash-basis accounting records income when money is received and expenses when money is paid. In this method, your books follow your bank account. If cash enters the account, it becomes revenue. If cash leaves the account, it becomes an expense.

This method is often easier for early-stage startups because there are fewer timing rules to manage. Founders can look at bank activity and get a quick sense of available cash. That makes it useful when the business has limited transactions, simple customer payments, and no complex reporting needs.

Cash-basis accounting usually works well for the following:

- Very early-stage startups with few transactions.

- Founder-led businesses without complex contracts.

- Startups that mainly need bank-level cash visibility.

- Teams that do not yet need GAAP-style investor reporting.

Under cash-basis accounting, timing depends on cash movement, not when work happens. If a startup sends a $10,000 invoice in March and receives payment in April, the revenue is recorded in April. If the startup receives a vendor bill in March but pays it in May, the expense appears in May. This makes the method simple, but it can also make monthly reports look uneven.

Benefits of Cash-Basis Accounting for Startups

Cash-basis accounting gives founders a simple way to track money without building a finance process too early. It works best when the business is still small and does not have many unpaid invoices, vendor bills, subscriptions, or investor reporting needs.

Key benefits of cash-basis accounting include:

- It is easier to maintain with limited finance support.

- It stays closely tied to the startup’s bank account.

- It helps founders check daily cash availability.

- It reduces bookkeeping effort in the early stage.

- It is easier for non-finance founders to read and explain.

Limits of Cash-Basis Accounting for Startups

The main weakness of cash-basis accounting is that it shows cash movement, not business performance. A month may look profitable because a customer paid late. Another month may look weak because several large bills were paid together. This can make it harder to compare performance across months.

Common limits of cash-basis accounting include:

- It can overstate or understate profitability.

- It may not show unpaid customer invoices clearly.

- It may not show vendor bills that are due but unpaid.

- It can make monthly performance harder to compare.

- It may not meet investor, lender, audit, or GAAP reporting needs.

What Is Accrual Accounting?

Accrual accounting records revenue when it is earned and expenses when they are incurred. This happens even if the money has not moved yet. So, your books do not only show what entered or left the bank. They show what the business earned, what it owes, and what it still needs to collect.

This method gives startups a clearer view of financial performance by period. It is especially useful when the company has customer invoices, vendor bills, annual subscriptions, deferred revenue, prepaid expenses, or cross-border transactions. These are common once a startup starts selling SaaS, raising institutional capital, or building a team across countries.

The matching principle means revenue and related costs should be recorded in the same period where possible. For example, if a startup delivers a service in March and also incurs hosting costs in March, both should appear in March reports. This helps founders see whether the business was profitable when the work happened, not only when the cash was received or paid.

How Accounts Receivable and Accounts Payable Work in Accrual Accounting

Accrual accounting uses accounts receivable and accounts payable to track money that has been earned or owed but not yet paid. This gives founders a better picture of upcoming collections and upcoming obligations.

Accounts receivable: Money customers owe the startup for products or services already delivered.

Accounts payable: Money the startup owes vendors, contractors, or service providers for costs already incurred.

For example, if a startup sends a $20,000 invoice in March but receives payment in April, accrual accounting records the revenue in March and shows $20,000 as accounts receivable until the customer pays.

Benefits of Accrual Accounting for Startups

Accrual accounting gives founders, investors, and finance teams a more accurate way to read startup performance. It separates business activity from payment timing, which makes reports easier to compare month by month.

Key benefits include:

- It gives a better view of revenue and expenses by period.

- It creates cleaner financial statements for investors.

- It helps track unpaid customer invoices.

- It helps track vendor bills and company liabilities.

- It works better for SaaS, inventory, marketplace, and cross-border startups.

Limits of Accrual Accounting for Startups

Accrual accounting gives better reporting, but it also requires more discipline. The startup needs a proper chart of accounts, month-end review, and regular tracking of receivables, payables, deferred revenue, and prepaid expenses.

Common limits include:

- It requires more bookkeeping discipline.

- It needs month-end adjustments.

- It can show profit before cash has arrived.

- It requires founders to review both accrual reports and cash flow reports.

What Is the Difference Between Cash and Accrual Accounting?

Cash and accrual accounting mainly differ in timing. Cash accounting follows money movement. Accrual accounting follows business activity. That one difference changes how revenue, expenses, profit, receivables, payables, and investor reports appear in your books.

Which Accounting Method Should Early-Stage Startups Use?

Early-stage startups with simple revenue, few expenses, no inventory, and no near-term investor reporting needs can often start with cash-basis accounting. It keeps bookkeeping easy, gives founders a direct view of money in the bank, and reduces finance work when the business is still testing its market.

But cash-basis accounting becomes less useful once the startup starts invoicing customers, delaying vendor payments, selling annual subscriptions, or preparing investor updates. If your startup is raising capital, operating across the US and India, or preparing for diligence, accrual accounting gives a cleaner view of revenue, costs, payables, receivables, and deferred revenue.

Use cash-basis accounting when:

- The business has simple transactions.

- Most customers pay immediately.

- There are few unpaid bills.

- Investor reporting is not yet required.

- The main goal is basic tax-time bookkeeping.

Use accrual accounting when:

- The startup invoices customers before receiving payment.

- Revenue is earned before cash reaches the bank.

- Vendor bills are paid after services are used.

- The company has deferred revenue or subscriptions.

- Investors, lenders, or auditors need cleaner financial statements.

- The startup has US-India operations or cross-border compliance needs.

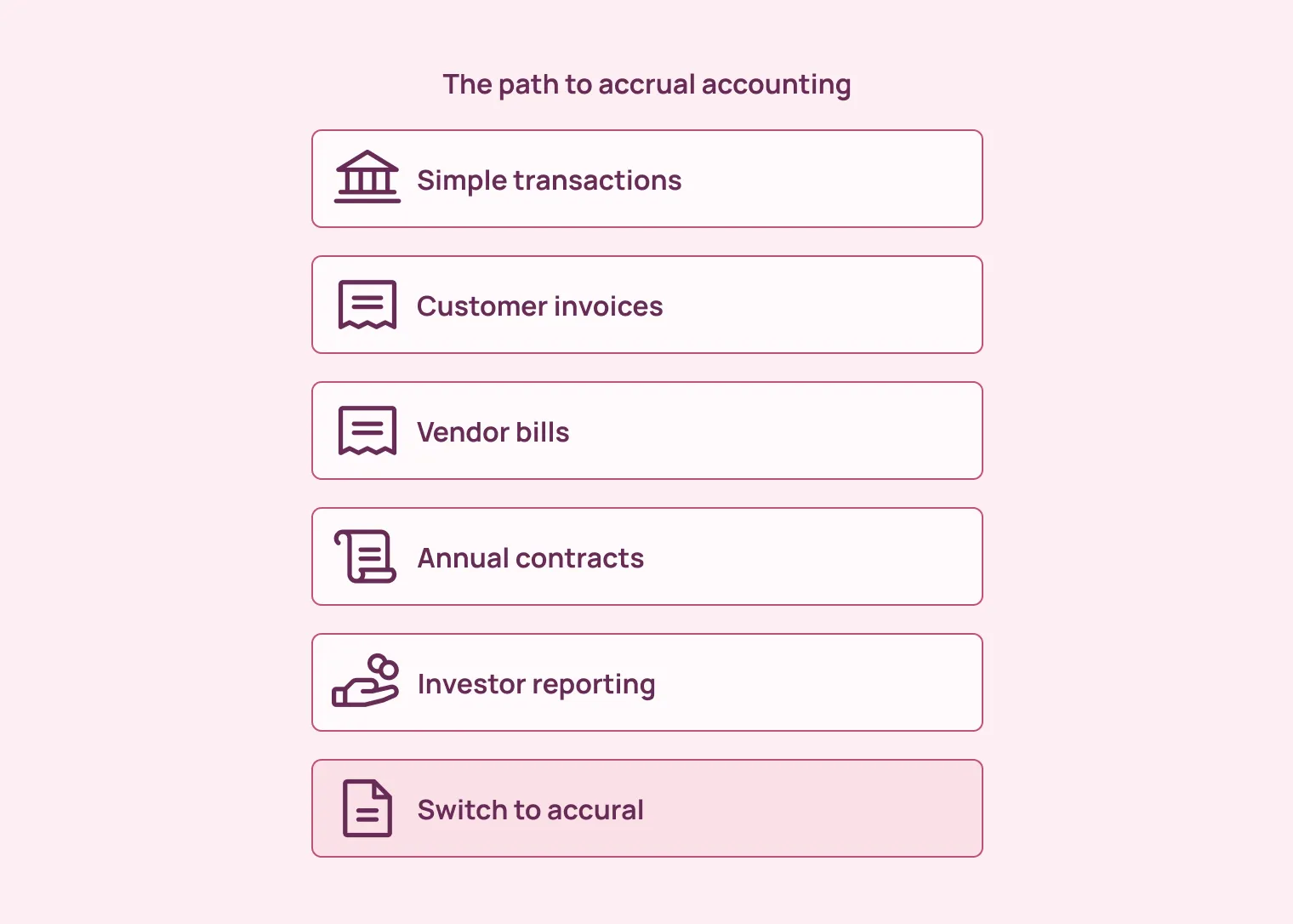

When Should a Startup Switch from Cash to Accrual Accounting?

You should switch from cash to accrual accounting when cash-basis books stop showing a reliable view of performance. This usually happens when the company has more customer invoices, delayed collections, vendor bills, annual contracts, or investor reporting requirements.

The switch should ideally happen before fundraising, audit preparation, or diligence begins. Converting old records under pressure can take more time, cost more, and create avoidable back-and-forth with investors or tax advisors. For startups planning a priced round, the transition should begin a few months before financial statements are shared.

Common triggers include:

- The startup is preparing for seed, Series A, or later funding.

- The team needs to manage accounts receivable and collections.

- The company has vendor bills, payables, or contractor obligations.

- The startup sells annual contracts, subscriptions, or prepaid plans.

- The business manages inventory or cost of goods sold.

- Founders need financial statements for board, lender, or investor review.

Why Accrual Accounting Matters for Fundraising

Investors want to see how the business performs across periods, not just when cash moves. Accrual accounting gives them a cleaner view of earned revenue, actual expenses, unpaid invoices, deferred revenue, and liabilities. It also reduces the need to rebuild financials during diligence.

Accrual accounting helps fundraising because:

- Investors can compare revenue and expenses across months.

- Accrual books show the quality and timing of revenue.

- Deferred revenue and receivables are easier to review.

- Clean books reduce back-and-forth during funding rounds.

What IRS Rules Should Startups Check Before Choosing a Method?

You cannot always choose an accounting method only based on convenience. Tax rules may limit which method a business can use, especially as revenue grows or the company holds inventory. For many small startups, cash-basis accounting is allowed because it is simpler and easier to maintain. But once a business crosses certain revenue thresholds or has more complex operations, accrual accounting may become required for tax reporting.

For 2025, the IRS small business taxpayer threshold was generally $31 million or less in average annual gross receipts for the prior three years. For 2026, the gross receipts test threshold is $32 million. Startups should confirm the current threshold, inventory rules, and any entity-specific requirements with a CPA before choosing or changing accounting methods. Inkle’s guide also notes that C-corps crossing the gross receipts threshold are required to use accrual accounting.

How Do Cash and Accrual Accounting Affect Startup Financial Statements?

Cash-basis accounting can make a startup’s financial statements look uneven from month to month. One month may look highly profitable because a large customer finally paid. Another month may look weak because several vendor bills were paid together. The business activity may be stable, but the reports can look volatile because cash timing drives the numbers.

Accrual accounting reduces this timing distortion. It records revenue in the period it is earned and expenses in the period they relate to. This gives founders a clearer view of revenue trends, gross margin, operating expenses, and true burn. It also makes financial statements easier for investors, lenders, and tax advisors to review.

How the Income Statement Changes

Under cash-basis accounting, the income statement often follows payment timing. This can make revenue, gross margin, and operating expenses look inconsistent. Under accrual accounting, the income statement shows activity by period. That makes it easier to compare monthly performance, track margins, and explain financial results during investor updates.

How the Balance Sheet Changes

Accrual accounting adds more structure to the balance sheet. It can include accounts receivable, accounts payable, deferred revenue, prepaid expenses, and accrued expenses. These items help founders see what the company has earned but not collected, what it owes but has not paid, and what cash received still needs to be earned through future service delivery.

How Cash Flow Reporting Fits In

Accrual accounting does not replace cash flow tracking. A startup can show revenue under accrual accounting even before the customer pays. That is why founders still need cash flow reports to track runway, burn, collections, payment timing, and available bank balance. The best finance view usually combines accrual-based performance reports with cash flow reporting.

How Can Startups Switch from Cash to Accrual Accounting?

Switching from cash to accrual accounting means your books need to start tracking business activity, not only bank movement. This includes unpaid customer invoices, unpaid vendor bills, deferred revenue, prepaid expenses, and accrued expenses. For tax reporting, the switch may also require Form 3115 and a Section 481(a) adjustment, so founders should review the change with a CPA before applying it to tax filings.

Follow this checklist to switch from cash to accrual accounting:

Step 1 - Review the current chart of accounts

Make sure revenue, expenses, assets, liabilities, and equity are structured correctly.

Step 2 - Identify unpaid customer invoices

These may need to be recorded as accounts receivable.

Step 3 - Identify unpaid vendor bills

These may need to be recorded as accounts payable.

Step 4 - Record deferred revenue for prepaid customer contracts

Cash collected upfront may need to be recognized over the service period.

Step 5 - Record prepaid expenses for upfront costs

Annual software, insurance, or similar costs may need to be spread over time.

Step 6 - Add accrued expenses for costs incurred but not yet billed

This helps match costs to the correct period.

Step 7 - Reconcile bank accounts, credit cards, payroll, and payment processors

Clean reconciliations reduce errors during the transition.

Step 8 - Review opening balances with a CPA or startup accounting team

This helps avoid double-counting or missing revenue and expenses.

Step 9 - Set a monthly close process

Accrual accounting works best when books are reviewed every month.

Step 10 - Create accrual-based reports for founders, investors, and tax advisors

These reports give a clearer view of performance, obligations, and cash needs.

The IRS treats a cash-to-accrual switch as a change in accounting method, and eligible businesses may use the automatic change process with Form 3115. You need to calculate the transition adjustment so income and expenses are not counted twice or skipped.

Can Startups Use a Hybrid Accounting Method?

Some startups use a hybrid accounting method for specific reporting or tax needs. In this approach, certain items may be tracked on a cash basis, while others are tracked on an accrual basis. For example, a company may use cash-basis accounting for some operating expenses but track inventory, receivables, or payables differently because of tax or reporting requirements.

A hybrid approach can work in limited cases, but it can also create confusion if founders rely on it for management reporting. The risk is that reports may not show a clean view of cash, revenue, expenses, or liabilities. Before using a hybrid method, founders should ask a CPA whether it fits their tax position, business model, and investor reporting needs.

A hybrid accounting method:

- May work for simple tax reporting in limited cases.

- Can create reporting gaps if used for management accounts.

- May not work well for investor or lender reporting.

- Should be reviewed by a CPA before use.

How Inkle Helps Startups Manage Accounting

Inkle helps startups keep their books cleaner by bringing bookkeeping, tax, and compliance workflows into one place.

This is especially useful for cross-border startups with US-India operations. These companies often need to track income, vendor bills, intercompany costs, payroll, reimbursements, and compliance deadlines across entities. Inkle helps founders move from scattered finance records to books that are easier to review, report, and trust.

With Inkle, startups can:-

- Automate bookkeeping workflows for startup finance teams.

- Track income, expenses, payables, and receivables.

- Support a cleaner month-end close process.

- Prepare financial reports for tax filings and investor updates.

- Manage US-India compliance tasks in one place.

Book a demo with Inkle to make your startup books investor-ready and tax-ready.

Frequently Asked Questions

What is the main difference between cash and accrual accounting?

Cash accounting records revenue and expenses when money moves in or out of the bank. Accrual accounting records revenue when it is earned and expenses when they are incurred, even if payment happens later. This makes accrual accounting more useful for tracking actual business performance.

Is cash-basis accounting enough for an early-stage startup?

Cash-basis accounting may be enough for a very early-stage startup with simple transactions, immediate payments, and limited reporting needs. It works well when founders mainly need to track bank balances and basic expenses. It becomes less useful when the startup has invoices, unpaid bills, subscriptions, investors, or cross-border operations.

Why do investors prefer accrual accounting?

Investors usually prefer accrual accounting because it shows revenue, expenses, receivables, payables, and deferred revenue more clearly. This helps them review business performance without relying only on cash movement. It also makes monthly reports easier to compare during diligence.

When should a startup move from cash to accrual accounting?

A startup should consider moving to accrual accounting before fundraising, audits, complex customer contracts, inventory management, or investor reporting. It is better to switch before diligence creates pressure. Waiting too long can make the transition more expensive and harder to clean up.

Does accrual accounting show how much cash a startup has?

No. Accrual accounting shows revenue and expenses by period, but it does not replace cash flow tracking. Founders still need cash flow reports to track bank balance, runway, burn, collections, and upcoming payments.

Can a startup use cash accounting for taxes and accrual accounting for management reports?

In some cases, yes. But the rules depend on the company’s structure, revenue, inventory, and tax position. A CPA should review the approach before the startup uses different methods for tax reporting and internal reporting.

In this article