How Startups Can Automate Bookkeeping With AI and Save Time

Manual bookkeeping quietly consumes hours that founders could spend on product, sales, or hiring. As startups scale, transaction volumes increase across payment processors, bank accounts, payroll tools, and SaaS subscriptions. Without automation, finance teams often spend large amounts of time categorizing transactions, reconciling accounts, and organizing receipts instead of reviewing financial performance.

AI accounting software changes this workflow. These tools automate most routine bookkeeping tasks such as categorization, reconciliation, and document extraction. Instead of entering data every day, startups can shift to a review-based process where automation handles the bulk of the work and humans focus on exceptions.

In this guide, we explain what AI can automate in bookkeeping, the typical tools used in startup finance stacks, and how founders can set up a simple system that keeps their books accurate and ready for taxes or investor reporting.

What AI Can Handle in Startup Bookkeeping

AI bookkeeping tools focus on repetitive financial tasks that traditionally require manual entry or review. By learning from transaction patterns, vendor history, and accounting rules, these systems can categorize transactions, process documents, and reconcile accounts automatically. The result is a bookkeeping workflow where automation handles routine entries and humans focus on exceptions and financial review.

i) Code Bank and Card Transactions Automatically

AI bookkeeping systems analyze transaction data from connected bank accounts and corporate cards to assign categories automatically. The software studies vendor names, past transaction history, and the company’s chart of accounts to predict the correct classification. For example, payments to cloud providers may consistently map to infrastructure expenses, while SaaS subscriptions map to software costs. Over time, the system improves accuracy as it learns from corrections made by accountants or founders.

ii) Extract and Book Receipts, Bills, and Invoices

AI systems can process financial documents and convert them into accounting entries automatically. Instead of manually entering expense data, the system reads documents and prepares draft records in the ledger.

- OCR reads PDFs and emails

- Vendor, tax, and line items pulled into entries

- Draft bills or expenses auto-created

iii) Reconcile and Flag Errors in Real Time

Modern bookkeeping automation tools match transactions across bank feeds, invoices, and payment processors to reconcile accounts continuously. When a payment is recorded in the bank but not linked to an invoice, the system flags it for review. AI can also detect duplicate transactions, unusual spending patterns, or uncategorized expenses that require attention. These alerts help finance teams catch errors early instead of discovering them during the month-end close.

Step-by-Step Plan to Implement AI Bookkeeping in Your Startup

Adopting bookkeeping automation does not require a complex finance transformation. Most startups can implement AI bookkeeping by connecting existing tools, cleaning up their accounting structure, and setting review rules.

The goal is to move from daily manual entry to a controlled monthly review process supported by automation.

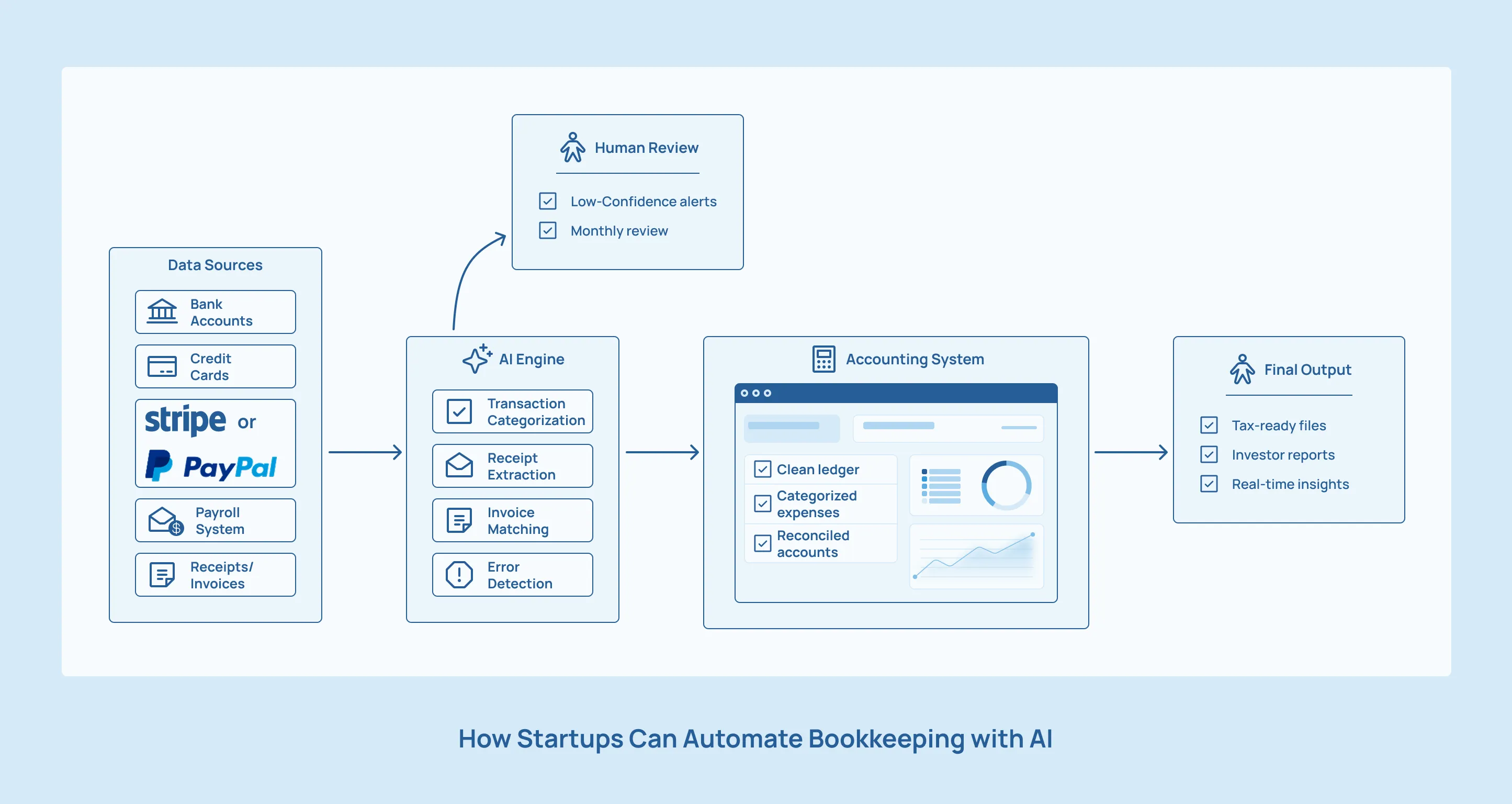

Step 1: Connect Your Data Sources

Start by linking your financial data sources to the accounting platform and AI bookkeeping tool. Most tools allow direct integrations with banks, credit cards, payment processors, and payroll systems. Typical connections include bank accounts, Stripe, PayPal, payroll software, and the accounting ledger. Once connected, transactions flow automatically into the system without manual imports.

Step 2: Define Chart of Accounts and Key Rules

Automation works best when the chart of accounts is clean and consistent. Startups should remove duplicate categories, standardize expense groups, and define clear vendor rules. For example, payments to AWS may always map to infrastructure expenses, while advertising platforms map to marketing spend. Once these rules are defined, AI tools learn from them and classify future transactions more accurately.

Step 3: Set Up Review Thresholds

AI bookkeeping tools allow startups to define when transactions should be posted automatically and when they require review.

- Auto-post high-confidence transactions

- Route low-confidence or high-value items to a human

- Weekly spot checks to confirm categorization accuracy

This setup keeps automation running while maintaining control over unusual or sensitive transactions.

Step 4: Close Monthly With AI Support

At the end of each month, founders or finance teams review flagged transactions and reconcile remaining balances. AI dashboards highlight anomalies such as uncategorized expenses, unmatched payments, or unusual spending patterns. Once corrections are made, the books can be closed quickly with supporting documentation already attached.

Step 5: Sync to Tax and FP&A Tools

Clean accounting data feeds directly into tax preparation platforms and financial planning tools. When the ledger is updated automatically and reconciled monthly, startups can generate financial statements, tax reports, and cash forecasts without rebuilding data manually. This also makes investor reporting and fundraising preparation much easier.

How Automated Bookkeeping Saves Startups Time and Money

When transactions, receipts, and reconciliations are automated, founders spend less time managing financial records and more time reviewing performance. A structured automation setup also keeps books consistently updated, which improves decision-making and reduces stress during tax filing or fundraising.

i) Fewer Hours on Manual Bookkeeping

Manual bookkeeping requires founders or finance teams to categorize transactions, upload receipts, reconcile accounts, and investigate discrepancies. AI bookkeeping tools automate most of these steps by learning transaction patterns and vendor mappings. As a result, startups often reduce bookkeeping workload by 50–80%, shifting from daily accounting tasks to periodic reviews of flagged items.

ii) Better Visibility Into Financial Metrics

Automation keeps financial records continuously updated, allowing founders to monitor important metrics without waiting for manual reconciliation.

- Live view of burn and runway

- CAC and LTV calculations based on updated expense categories

- Investor-ready financials before fundraising conversations

iii) Reduced Risk in Tax and Diligence

Accurate categorization and continuous reconciliation reduce the risk of errors during tax preparation or financial audits. When expenses are classified correctly and documents are attached to entries, accountants can prepare filings faster and investors can review financial statements with greater confidence. This lowers compliance friction and avoids last-minute corrections before reporting deadlines.

How Inkle Helps Startups Automate Bookkeeping

Inkle helps you automate transaction categorization and financial data organization. As transactions flow into the ledger, automation rules classify common expenses, identify recurring vendors, and prepare draft accounting entries that are ready for review.

The platform also prepares structured financial reports that founders can use for tax filings, investor reporting, and compliance requirements. This allows startups to move from scattered financial data to a clean ledger that stays updated as transactions occur.

Automation works best when paired with clear review processes. Inkle includes controls that help founders maintain accurate records while keeping automation active.

- Categorization rules with confidence scores

- Flagged items routed to a CPA or founder for review

- CPA-reviewed filings and tax reports

Automated bookkeeping can save significant time, but the setup matters. Clean ledgers, accurate categorization, and consistent reconciliation ensure that automation actually improves financial reporting.

Book a free demo with Inkle to simplify your startup’s bookkeeping and get investor-ready faster.

Frequently Asked Questions

What is AI bookkeeping?

AI bookkeeping uses automation and machine learning to handle routine accounting tasks such as categorizing transactions, reconciling accounts, and processing receipts. Instead of entering data manually, AI systems analyze transaction patterns and vendor history to generate accounting entries automatically.

How accurate are AI accounting tools?

High-confidence transactions in AI accounting systems often exceed 90% categorization accuracy. These tools learn from historical data and predefined rules to classify expenses correctly. When the system detects uncertainty, it flags those transactions for human review to maintain clean financial records.

Do I still need a human to review my books?

Yes. AI reduces repetitive bookkeeping work, but human oversight remains important. Founders or accountants review flagged transactions, verify unusual expenses, and confirm that records align with tax rules and reporting standards.

How does Inkle support automated bookkeeping?

Inkle connects with your accounting ledger and applies automation to categorize transactions and organize financial data. The platform prepares tax-ready financial reports and includes CPA oversight to ensure that your books remain accurate and compliant as your startup grows.

In this article