How to Know When Your Startup Needs Monthly Bookkeeping

Most startups begin with spreadsheets, manual entries, and irregular bookkeeping updates. It works fine in the early days when there are only a few transactions each week. But as financial activity grows, those simple methods start to crack. Missed payments, delayed reports, and inaccurate cash flow tracking can quickly turn into real business risks.

Monthly bookkeeping can solve this problem. It creates structure, visibility, and control over your finances as your startup scales. In this article, we’ll walk through the key signs that it’s time to move beyond spreadsheets and adopt monthly bookkeeping. If any of these situations sound familiar, your business has likely outgrown its current setup.

Ask yourself these questions to figure out if your startup needs monthly bookkeeping:-

Q1: Are You Seeing More Transactions Than You Can Track Manually?

As your startup starts processing more sales, expenses, and payments each month, keeping track manually becomes harder and riskier. Spreadsheets can’t scale with your growth. They break easily, lead to inconsistent records, and make it difficult to get an accurate financial snapshot when you need it. Monthly bookkeeping introduces structure and automation, ensuring every transaction is recorded correctly and on time.

Here are common signs your transaction tracking is breaking down:

- Sales and expense entries are increasing faster than you can update them.

- Manual tracking is becoming inconsistent or delayed week after week.

- Transactions are being missed, duplicated, or misclassified in your records.

When financial volume grows, trying to manage everything by hand invites costly mistakes. Monthly bookkeeping helps you stay accurate, efficient, and audit-ready, no matter how fast your business scales.

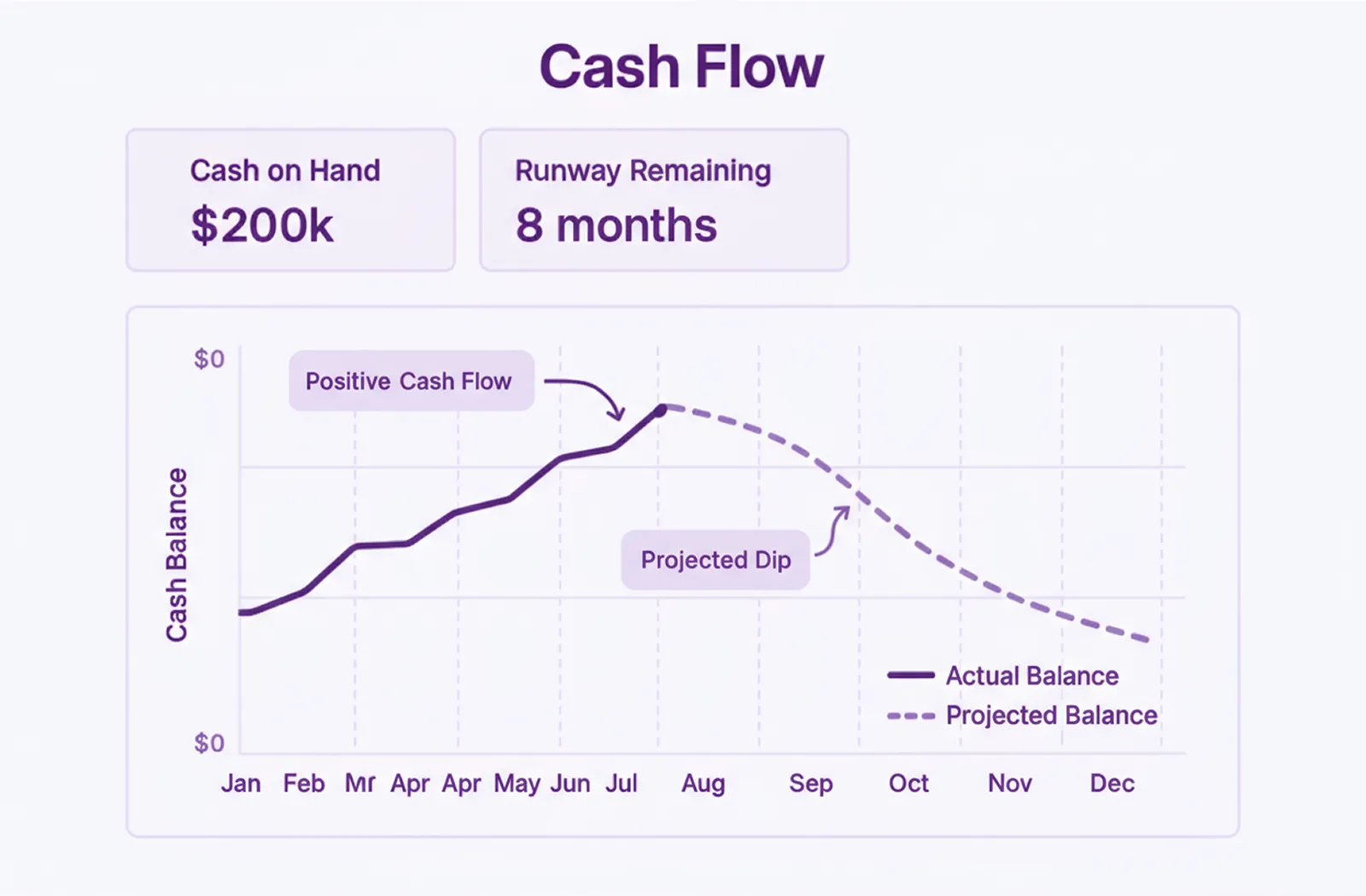

Q2 : Are You Unclear About Your Cash Flow or Runway?

If you’re unsure how much cash is in your account or how long it will last, it’s time for monthly bookkeeping. Without updated financials, startups risk overspending, missing vendor payments, or making strategic decisions based on outdated numbers. Regular bookkeeping gives founders real-time visibility into income, expenses, and upcoming obligations, helping them plan ahead with confidence.

Here are common warning signs of unclear cash flow:

- You’re uncertain about upcoming payroll, vendor payments, or tax dues.

- You don’t have a reliable forecast comparing revenue against expenses.

- You struggle to answer investor questions about runway or burn rate.

- You miss opportunities because your financial data isn’t current or clear.

Knowing your cash position is about control. Monthly bookkeeping gives startups the clarity to make smart spending decisions, plan fundraising timelines, and avoid financial surprises that can derail growth.

Q3 : Do You Struggle to Generate Timely, Accurate Financial Reports?

When investors, lenders, or advisors ask for financial statements, you should be able to share them instantly, not after a weekend of reconciling spreadsheets. If producing basic reports like profit and loss, balance sheets, or cash flow statements feels like a scramble, your startup is ready for monthly bookkeeping. Regular reporting turns financial data into an ongoing narrative of your company’s growth instead of an occasional administrative task.

Here are clear signs your reporting process needs structure:

- Your financial reports are delayed, incomplete, or missing key details.

- Numbers vary across different documents, causing confusion and errors.

- Investor meetings or board reviews create stress because reports aren’t ready.

Consistent monthly bookkeeping ensures your reports are accurate, up to date, and audit-ready at any time. It helps founders move from reactive cleanup to proactive financial storytelling giving investors and teams confidence in every number shared.

Q4: Is Bookkeeping Taking Too Much Time Away from Growth?

As your startup scales, your time becomes your most valuable resource. If you’re spending weekends updating spreadsheets, reconciling bank accounts, or fixing missing entries, it’s a clear sign that bookkeeping has outgrown your bandwidth. Startups need founders focused on growth, not bookkeeping backlogs. Monthly bookkeeping solves this by creating a consistent, automated rhythm for financial updates freeing you to focus on strategy, customers, and innovation.

Founders often underestimate how much context-switching costs. Jumping between product work and expense categorization drains focus and creates more room for mistakes. A structured monthly bookkeeping process (or partner) ensures your finances stay on track, even when your attention is elsewhere.

Here are signs bookkeeping is costing you valuable time:

- You’re personally spending hours reconciling accounts or categorizing expenses.

- Product development, hiring, or sales are delayed because of bookkeeping tasks.

- You feel burnt out or keep falling behind on monthly financial updates.

Your time is best spent building your startup, not buried in accounting tasks. Monthly bookkeeping keeps your finances current with minimal effort, helping you stay focused on what matters most: scaling your business.

Q5: Are You Rushing Through Tax or Compliance Filings?

If every tax deadline feels like a last-minute sprint, your bookkeeping isn’t keeping pace with your business. Many startups only review their books once or twice a year, which leads to disorganized records, missing receipts, and inaccurate numbers when it’s time to file. Monthly bookkeeping removes this stress by keeping everything categorized, reconciled, and audit-ready throughout the year.

When your books are maintained monthly, you’ll always have the financial data needed for tax filings, compliance checks, and investor reporting without the panic. Consistent tracking ensures you never miss deductions, deadlines, or government requirements.

Here are common signs you’re rushing through filings:

- Records are incomplete or outdated during tax season.

- Filing errors or mismatched data cause unnecessary penalties.

- Reporting deadlines for investors or agencies are missed.

By staying organized month by month, startups transform tax season from a stressful scramble into a predictable process. The result: smoother filings, fewer errors, and complete peace of mind when compliance checks come around.

Growth Milestones Signal that It’s Time for Monthly Bookkeeping

Every startup reaches a point where ad-hoc recordkeeping stops working. At first, tracking finances in spreadsheets might feel efficient, but as transactions multiply, it becomes harder to stay accurate, compliant, and investor-ready. Growth brings complexity, and with it, the need for a consistent financial process that keeps pace with your company’s evolution.

Monthly bookkeeping gives startups the visibility and control to manage that complexity. It turns messy financial data into organized insights that support faster decision-making, cleaner reporting, and stronger investor confidence. Recognizing the right time to make this shift is key to maintaining stability while scaling.

1. Preparing for a Fundraising Round

Investors expect organized, verifiable financials. When you start building pitch decks or having early conversations with VCs, monthly bookkeeping becomes non-negotiable. It ensures your profit and loss statements, cash flow reports, and expense records are ready for due diligence without the stress of last-minute cleanups.

2. Hiring Employees or Expanding Vendor Relationships

The moment you start paying salaries, managing reimbursements, or working with multiple vendors, your transaction volume grows exponentially. Monthly bookkeeping helps you track every payment, automate reconciliations, and prevent errors that could affect payroll accuracy or vendor trust.

3. Launching New Products or Entering New Markets

Expanding into new markets or launching additional products adds new revenue streams and compliance requirements. Monthly bookkeeping consolidates these changes into clear, unified reports so you can see the financial performance of each line of business and ensure compliance across states or regions.

4. Watching Your Burn Rate Increase

A rising burn rate is a natural part of scaling but only if it’s measured. Monthly bookkeeping helps monitor runway and spending patterns closely, giving you the foresight to make adjustments before cash constraints appear. It also allows founders to model scenarios and plan funding timelines more accurately.

5. Getting Investor or Board Reporting Requests More Frequently

Once you start receiving regular investor updates or board meeting requests, monthly bookkeeping becomes essential. It keeps your data fresh and reliable, ensuring you can deliver accurate reports quickly, backed by organized records.

As your startup grows, your financial processes should grow with it. Monthly bookkeeping ensures your records stay consistent, your insights stay real-time, and your decisions stay strategic, no matter how fast your business evolves.

How Inkle Helps Startups Switch to Monthly Bookkeeping

With AI-powered automation, Inkle syncs your transactions, categorizes them intelligently, and reconciles your accounts automatically. You don’t have to chase receipts or manually label every expense; Inkle does it for you. Each month, you receive clean, reconciled books along with reports that investors, auditors, or tax preparers can use instantly.

Here’s how Inkle simplifies monthly bookkeeping for startups:

- It syncs transactions across bank accounts and payment platforms, ensuring nothing is missed.

- It categorizes and reconciles records automatically, saving hours of manual effort.

- It generates monthly reports for founders, investors, and tax professionals ready for compliance or review.

- It includes built-in checks to flag inconsistencies and avoid compliance errors before they cause issues.

Inkle helps startups move from reactive bookkeeping to proactive financial management. You’ll gain the structure and visibility of a full finance team without the cost or complexity.

Ready to make bookkeeping the easiest part of running your startup? Book a demo with Inkle and see how automation can help you stay organized, compliant, and investor-ready every single month.

Frequently Asked Questions

What are the top signs my startup needs monthly bookkeeping?

If you’re dealing with rising transaction volumes, unclear cash flow, delayed reporting, or last-minute tax filing chaos, it’s time to move to monthly bookkeeping. These are signs your startup has outgrown spreadsheets and needs structure for accuracy and growth.

Is monthly bookkeeping only for funded startups?

No. Even pre-seed or bootstrapped startups benefit from consistent recordkeeping. Monthly bookkeeping helps track burn rate, manage runway, and prepare for future investor conversations long before funding rounds begin.

How does monthly bookkeeping improve financial decision-making?

It gives founders a clear, updated picture of their financial position every month. With real-time reports, you can budget smarter, forecast confidently, and identify risks or opportunities before they affect cash flow.

When should I switch from DIY spreadsheets to a professional bookkeeping process?

When spreadsheets become error-prone, slow, or stressful to maintain, that’s your signal to switch. A structured monthly bookkeeping system like Inkle ensures accuracy, organization, and compliance without draining founder time.

Can I automate monthly bookkeeping without hiring in-house help?

Yes. Inkle automates the entire bookkeeping process from transaction syncing to reconciliation and monthly report generation. You’ll stay organized and audit-ready without needing to hire a dedicated finance team.

In this article

.webp)

.webp)